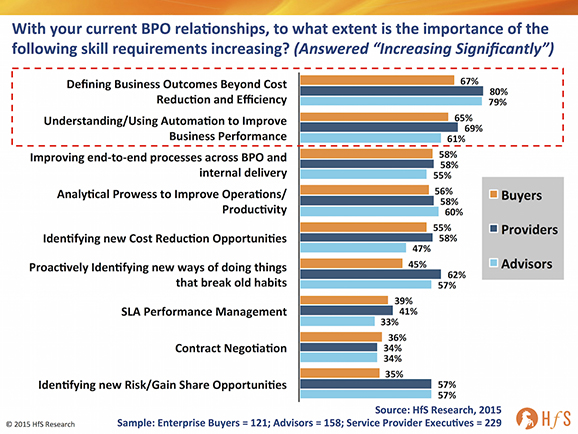

We’re shortly going to release the results of our new study delving into BPO talent, which probes into whether there is a genuine career path to follow for BPO and operations professionals, or whether we’re terminally stuck in the “accidental career” we never intended to venture into. In anycase, I wanted to share one set of data points that show which skills have been increasing in significance.

RPA has arrived as a core part of BPO’s future

Over the past year, the skill where demand and expectations has become the most elevated, more than any other, is automation. 65% of service buyers and 69% of provider professionals cite the need to understand and deploy automation is significantly increasing as a skill requirement – and even 61% of advisors are feeling the pressure to knowledge-up.

Essentially, as the room for additional cost savings diminishes for BPO buyers, the logical next step is to reduce manual tasks (and ultimately unnecessary labor costs). With the heavy marketing coming from service providers and technology firms offering robotic process automation (RPA) solutions, the awareness from the buy side – and pressure on operations managers – to have a more defined, measurable automation strategy, has never been as intense as it is today, and is likely to crescendo for some time to come yet. At HfS, we are getting calls every week from buyers wanting support developing an RPA plan for their business – it’s becoming the new efficiency drive for many experienced BPO buyers. Whatever actions buyers eventually take with RPA, they at least need to have some sort of strategy developing to placate the higher-ups questioning where their next 20% of productivity benefits are going to to come from.

The Bottom-line: RPA provides transformation baby steps for buyers wanting away from overdependence on labor arbitrage

RPA provides that logical first step for buyers and service providers to reduce their reliance on throwing lower cost human labor at problems. It provides the building blocks to develop more streamlined end-to-end processes, to perform more meaningful analytics, to create more of a digital infrastructure across the business. Essentially, RPA is the new arbitrage for many, but is unlikely to yield massive cost-savings in the near to medium terms – it is more about helping enterprises deploy their talent on higher value activities. In short, RPA is about working smarter, not cheaper.

Would you believe it? That quirky little research firm that started as a blog, at which many people snickered as a flash in the pan… reached 5 years old this week.

But we actually had a plan – and it was a five year one to break into the analyst mainstream and influence our services markets as much as any of the establishment analysts who’ve been around for years. Have we succeeded in doing that? I’ll leave that to you to decide…

I would personally like to recognize several characters who have played a part in helping HfS get off the ground and developing our reputation in the market as the destination for unvarnished insight, collaborative debate and plenty of entertainment: Esteban Herrera, Tom Ivory, Tony Filippone and Jamie Snowdon for having pride and faith in our mission and playing their part. Reetika Joshi, Charles Sutherland, Ned May, Mark Reed-Edwards, Tricia Bolger, Ned May, Pareekh Jain and Khalda de Souza for their ongoing support of the business and preaching the gospel – and putting up with me.

Fred McClimans, Bram Weerts, Hema Santosh and Barbra McGann for throwing their lot in with us recently to take us to a whole new level. And several friends (and family) who have been active in their support; Deb Kops, Lee Coulter, John Haworth, Sir Alan Fersht, David Poole, Jay Desai and many others. Also our early clients who have stayed loyal; Sarah Thomas, Shari Wenker, Mike Salvino, Ian Maher, Frank D’Souza, Stan Lepeak, Cliff Justice, Tiger Tyagarajan, Frank Cannata and many, many others. If I forgot to mention you, please forgive me as so many of you have been amazing with your support.

Now for our second 5 year plan…. what fun and games are in store for us next?

Happy Springtime all =)

Phil

Some fresh faced healthy looking chap in March, 2010…

Is your enterprise ready for what the future has in store for us?

This emergence of “As-a-Service” represents the most disruptive series of impacts to the traditional IT and business services industry that we have seen.

The globalization wave is peaking, and many maturing enterprise service buyers are struggling to find incremental value from the traditional outsourcing model, such as accessing more meaningful data, achieving better automation of processes, deploying end-to-end process delivery and accessing talent with creative business thinking skills. At the same time, service buyers need to keep driving down their operating costs to a minimum, with globally accessible technology platforms, based on common standards enabled by the cloud.

Looking at this next evolution of value, it is coming from technology-driven “As-a-Service” advancements that directly enhance employee, partner and customer effectiveness.

In short, the way service buyers receive services, and the way service providers sell and deliver them, is going to be very, very different in a few short years, and already some process areas where the technology is already available are being impacted.

At HfS, we have developed Eight Ideals of As–a–Service, that provide a guide for us all to follow as we look to achieving maximum value from our services in the future:

1. Design Thinking

2. Business Cloud

3. Intelligent Automation

4. Proactive Intelligence

5. Intelligent Data

6. Write off Legacy

7. Brokers of Capability

8. Intelligent Engagement

So how is your organization shaping up against these Ideals – and what is most important to you?

Whether you buy, provide or advise on business and IT services, your opinions and intentions are critical for our research, so please spend some time completing our study and you could win an Apple Watch.

Please note that your contact details will only be used for the purposes of sending you the optional executive report and entering you into the prize draw for the Apple Watch.

So please take our survey to air your views and experiences.

One of the main purposes of NASSCOM is to showcase the strength and direction of the Indian IT and BPO services economy. However, it’s not only about the heritage Indian firms promoting their strengths, it’s also a great venue for leading traditional Western-HQed service providers to brand themselves in India, to help them compete for the top talent.

One such service provider that’s made considerable strides in developing a major brand in India is Capgemini, whose staffing base has rocketed to 55,000 and made sure it had a very strong presence at the Mumbai showpiece this year. We managed to grab a side-bar with their dynamic CEO, Aruna Jayanthi, recently voted India’s third most powerful business woman by Fortune magazine, to talk a bit more about herself, her firm and her views on talent the future for India’s services economy…

Phil Fersht (CEO, HfS): Good afternoon, Aruna. Thanks for spending a bit of time with us today. Would you start by introducing yourself and how you got into this business?

Aruna Jayanthi (CEO, Capgemini India): I started with Capgemini 15 years ago. I now run Capgemini India, and before that I ran global delivery for our outsourcing business. I was part of the core team that setup India, and when I joined there were 80 people in India. Today, we are a little over 55,000 (couldn’t say this then due to impending results announcements – will be good to mention the new headcount number as this is current view).

Phil: 55,000. That’s a large number!

Aruna: It is a large number. But in the end, it’s not only numbers that matter; what matters is the value you deliver to your customers.

Phil: Right… so would you talk a bit about your career progression and how you ended up leading the India business for Capgemini?

Aruna: It’s a strange story, because twice in my life I was tempted to get out of the industry and do something else, but somehow I got back in. I started my career with TCS, fresh out business school. I got trained in programming and project management, did account management, the works. Then I thought, that’s enough, let me go try something else. And even though I did something completely different, I ended up in software for another in six years.

Then I decided to get into consulting. So I joined Ernst & Young in India, and within three months it was acquired by Capgemini. At that time, Capgemini didn’t have a presence in India, and the ex-Ernst & Young management consulting team became the core team that set it up and grew our offshore presence.

Phil: Traditionally, Capgemini has had a very strong reputation in Europe and in parts of Asia. And more recently, it’s been investing more in the U.S. and in India. And 55,000 is a big number, even though it’s not about the numbers. Would you talk about that operation and you know how it’s running? And, what do you think is making it successful?

Aruna: 70-percent of our business here is apps-oriented, and the rest is BPO and infrastructure-related services. And more than 90 percent of it is the traditional offshoring model. We do a little bit of work here for local Indian customers, but the bulk of the business is from customers in Europe, North America, and a little bit in Asia Pac.

What differentiates us in terms of value? We’ve managed to blend the India advantage and the local onshore advantage. That local touch is sensitive, it’s important, and we’re very strong with it in Europe and increasingly in North America.

Phil: Aruna, we spoke with several hundred services buyers for a study we’re producing. And the number one issue right now is talent and how to get more access to creative analytical capabilities, that sort of thing. How are you addressing that in India for Capgemini? What sort of people are you trying to hire? What’s the training strategy? What are you doing to try and stay ahead of the talent game?

Aruna: We’ve shifted our talent strategy in the past year and a half. Originally, we focused on lateral recruitment, meaning recruiting experienced hires from the industry. But in the last 18 months, we’ve started hiring far more fresh graduates.

The reason for it is twofold. First, there really aren’t many people already in industry that have experience in the new technology areas we want to build on. They just don’t exist. But I visit university campuses regularly, and look at the stuff they are doing in their labs. They have access to almost all the new technologies, as they get all the licenses at almost no cost. And the students are playing around with cool stuff, which is what we want. Of course, we continue with lateral recruitment when it’s appropriate.

That’s our shift in terms of where we get our recruits. The second shift is in terms of the skills we’re looking for. The Internet of Things, embedded systems, wearables, big data…now we’re focusing on analytics plus business skills. So while engineers were formerly our typical recruits, I think math graduates who have done a bit of business school are actually better.

Phil: So the theme of this year’s NASSCOM was “digital”, at a very high level. And an early takeaway of ours was that probably half of the service providers here get it. They know what’s happening, and they are figuring out what they need to do to get ahead of the curve. The other half they are like deer in headlights. How do you think India is going to make the shift, and do you think there is going to be some collateral damage on the way here?

Aruna: Phil – there is bound to be. My view is that when you look at digital, it’s not about technology. The role of the provider itself is changing. The question is, who understands the shifting role of the provider and how do they see it? Are we strong enough to understand the emerging digital agency, and the fact that if you are going to work on the customer side of it you better understand that side of the business? Is my role to write a program or code a system for somebody? Or is my role to provide a solution for a problem that they have?

So if I take the latter approach of it’s my job is to provide a solution that gives the customer value, then I start to look at building different sets of skills altogether, right? I would start to look at building more consulting skills, more domain skills. My job then becomes an aggregator or an integrator role, as opposed to a software developer role. And I think for me that’s far more important. Providers that understand that shift will do well.

Phil: So, if you were to look out five years to 2020, what do you think we will be talking about?

Aruna: I think we’ll still have a large digital element, but we won’t be talking software or applications anymore. The content will be far more business-focused than IT-focused. Also, I think the definition of the service provider will change. To me, the start-ups will become far more important, and it could be an aggregation of much smaller companies. We may even see a completely different set of providers.

Phil: One final question, Aruna. If you were crowned the Empress of the Indian services industry for one week, what would you change?

Aruna: I would change our positioning. Let’s use cars designed in Germany as an analogy. We talk about German engineering and how great it is, but we never talk about where the cars are manufactured (which I think is most often Mexico.) We just say it’s German engineering. What I would really aim for is that we say, “It’s Indian designed software” or Indian whatever. That’s the value that we need to rebrand ourselves to. It could be delivered from anywhere in the world. But the branding that we need to get to is that this is Indian IT. It is a solution conceptualized in India.

Phil: Precise and to the point, Aruna! Thanks for sharing your insights with our readers – it’s been great to meet you.

Aruna Jayanthi (pictured) is the CEO, Capgemini India. You can view her bio here.

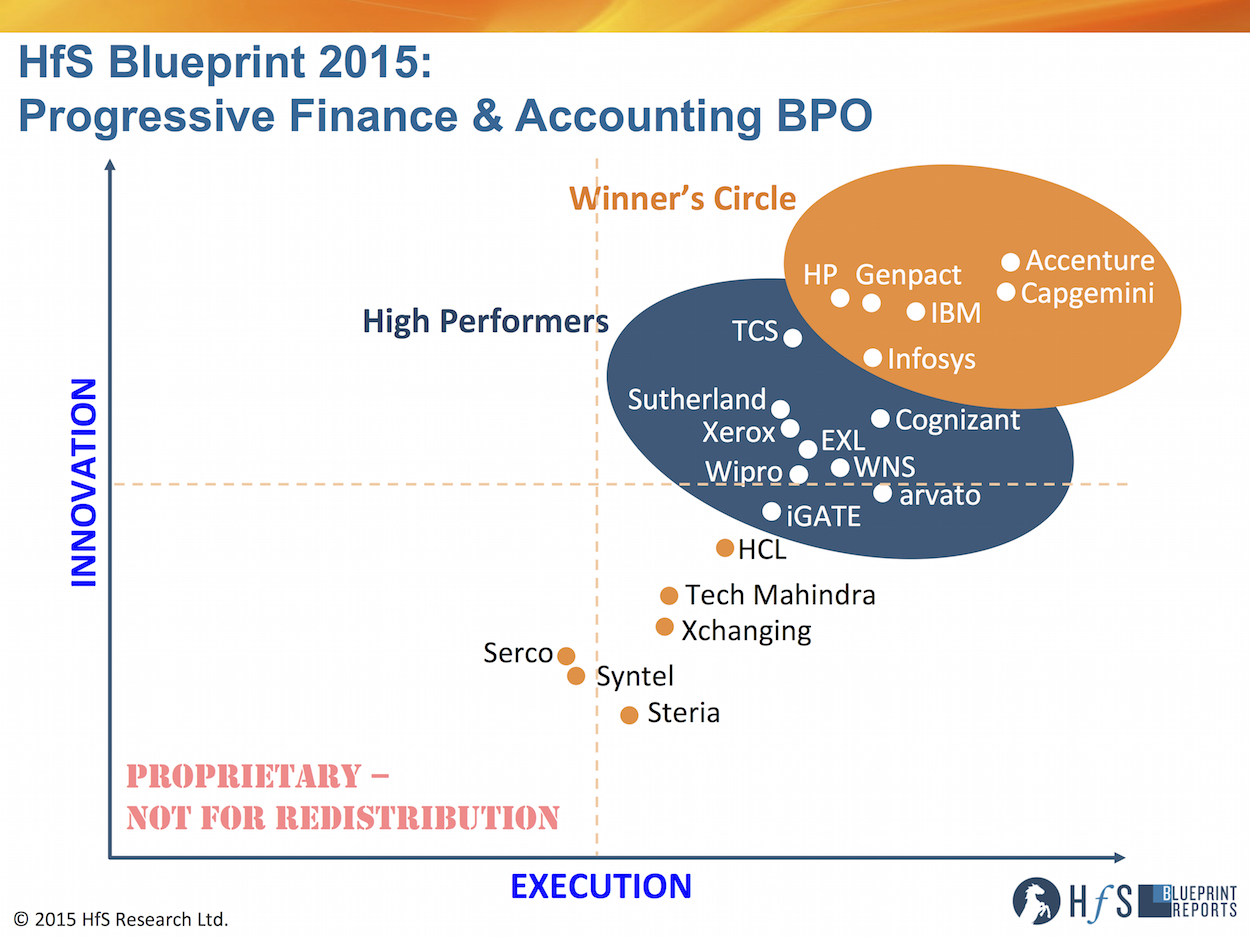

Almost two years to the day since we launched our first Blueprint Report, we finally circle back to the core horizontal services function providing the fulcrum for BPO and shared services: finance and accounting. For our 20th Blueprint, authored by analysts Phil Fersht and Hema Santosh, we deliberately focused on the proven “progressive” skills, investments, domain acumen and as-a-service potential of the leading providers in finance and accounting service delivery.

In order to pull together the most comprehensive view of this market, we created importance weightings for the key categories of services innovation and execution, that were based on the opinions of 1109 services buyers, advisors and provider executions in our 2014 State of Outsourcing Study, conducted in conjunction with KPMG. In addition, we conducted exhaustive interviews with more than 100 F&A service buyers, many of whom are members of the HfS Sourcing Executive Council. We didn’t rely 100% on reference clients ponied up from the service providers themselves – this is the genuine, unvarnished view of how providers are performing today from the people experiencing their services:

Click to Enlarge

So, Phil, what’s happening in the F&A space these days? Is the market slowing down as BPO services commodotize?

Not at all, one of the reasons why people hear about F&A “slowing down” is the diminishing role of sourcing advisors on F&A deals (only 30% of competitive F&A deals in 2013-14 were advisor-led, and 17% of sole-sourced used a advisor). A third of the deals were also sole-sourced, and very, very few were publicly announced. So the lack of “noise” causes people to incorrectly assume that activity in F&A is slowing down. In addition, we saw a lot more mid-sized businesses take the plunge for the first time, with 55% of F&A deals being signed up companies under $5Bn in revenues in 2013-14 – there have been many non-advisor-led sub-$15m engagements that pretty much flew under the radar in the last couple of years.

Net-net, total F&A BPO surpassed $25B in 2014, at a growth rate of 5%, with multi-process F&A BPO reaching $5B for the first time. Multi-process F&A BPO is expected to increase at 9% in expenditure in 2015.

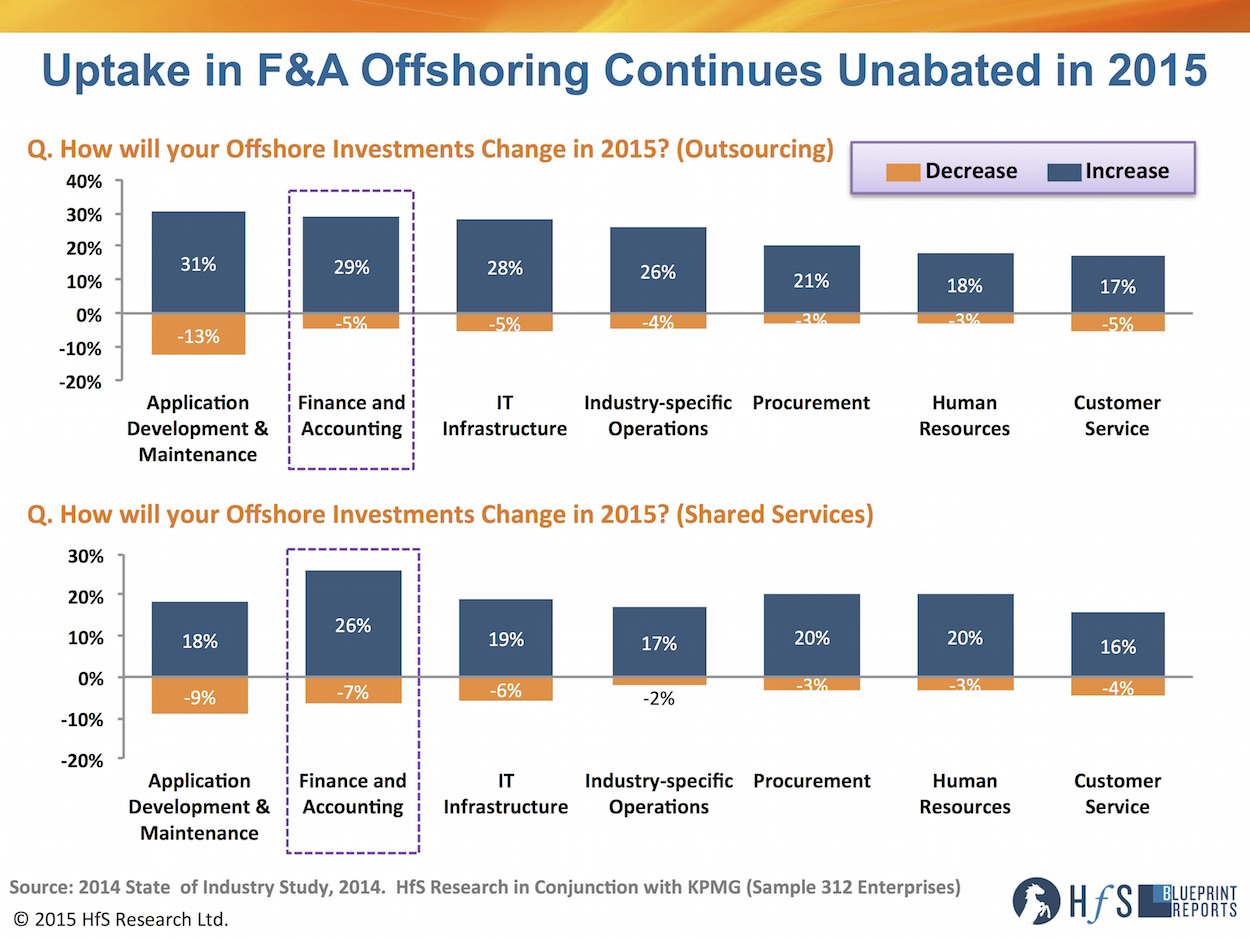

But isn’t offshoring slowing down? Surely buyers are pulling back from moving F&A delivery into offshore locations?

Stories of the demise of offshoring are not only premature, but wildly inaccurate. Our 2014 State of Outsourcing Study asked 312 major buyers of services their 2015 intentions to increase/decreasing offshoring, and close to one in three enterprises will increase their F&A offshore delivery for both outsourcing and (notably) shared services.

Click to Enlarge

This is indicative of buyers using their offshore in-house centers to house more controllership / high risk services they do not feel ready to outsource, but want to reduce overhead. Additionally, the increased scope in services that experienced buyers are outsourcing, such as F&A analytics, is increasingly markedly amongst some enterprise clients.

However which way you look at it, the offshore component of F&A is almost as popular as IT – and there is no slowdown in sight. While use of robotic process automation is being piloted by several F&A buyers, we’re still years away from firms being able to make significant reductions in labor as a results. F&A is a function which has, is and will be – for a very long time to come – dependent on people and talent. While buyers and sellers all want to leverage better tools and tech to streamline delivery and improve digital workflows, the change is more in the nature of work the delivery staff is doing than simply offloading them altogether. The game today is more about working smarter than simply cheaper..

Who’s winning the progressive game with the service buyers?

The most eye-opening shift has been the steady improvement of both HP and InfosysBPO to join the “Big 4” of Accenture, Capgemini, Genpact and IBM in the Winner’s Circle. We also saw real momentum, in terms of innovative delivery, from TCS, Cognizant and Sutherland and steady gains from both EXL and WNS.

I hope you all find the time to read our report that profiles each of the service providers, but there have been a few standout performances worth highlighting:

Accenture leads on partnerships with clients (Winner’s Circle)

Accenture breaks new ground with a formal joint venture with its long-standing client, Marriott, to go to market with BPO services to hospitality industry, where F&A outsourcing is a prominent offering. The firm increased its share of the market even further to 30% with its highly successful strategy of expanding its based of large enterprise (diamond) clients. The blending of F&A operations, infrastructure and close alignment with its shared services consulting has the firm leading the market in a time when clients need real consultative support.

Capgemini’s Global Enterprise Model is a world-class delivery platform for F&A services (Winner’s Circle)

Capgemini’s flexible, platform-based GEM methodology has all the aspects of progressive delivery covered from the right mix of FTEs, location mix, competency, technology, analytics, and governance. All key Capgemini clients attest real value from the GEM methodology. Capgemini has now emerged as one of the global market leaders with its laser focus and dedication to its F&A business.

Infosys wins big on account management attention and responsiveness (Winner’s Circle)

Infosys scores highly when it comes to the “listening” capabilities of their account management and delivery teams for clients. The firm are frequently cited as being easy to work with and highly responsive to the short- and long-term needs of clients of all sizes. Infy has shown a real hunger to grow their F&A business with multiple recent mid-sized deals that can be scaled in the future and a CEO who clearly sees the value of investing in his BPO business. The recent acquisition of automation tech firm Panaya (see link) could have major impact for clients struggling with ERP strangleholds in F&A.

HP leads with F&A Process Automation Tools and strong SAP-enablement capabilities (Winner’s Circle)

HP has been actively been driving the benefits of deploying robotic process automation for high volume, repetitive, rules-based work, and its AutoFlow tool for workflow meets the needs for clients tired of relying on legacy systems. Its recent number one rating in the 2015 Robotic Premier League is testament to HP’s strong automation focus in F&A. The recent restructuring of HP has been a positive for its F&A business, which has been better exposed to upper management as a genuine area of growth for the firm.

Smart Design and CFO focus from Genpact (Winner’s Circle)

Its dynamic ‘Smart’ foundation of Smart Strategy, Delivery, and Design are compelling and transformative, and Genpact’s tools have been backed by several customer F&A success stories. Moreover, Genpact is making investments in areas of F&A value to meet the needs of the CFO through its CFO Suite offering, under the leadership of Shantanu Ghosh, which could prove to become a major differentiator for the firm.

IBM drives innovative partnerships with clients (Winner’s Circle)

IBM continues to win over ambitious clients by hosting innovation discovery jams and workshops with its clients to understand pressing needs and create required solutions. There is strong future potential with its analytics and cloud offerings in F&A BPO. Its recent merging of GBS with GPS (BPO) delivery, could well craft a compelling proposition to the market, under the impressive leadership of Jesus Mantas, who is adopting the term “consult-to-operate services.” Mantas, a transformational consultative leader, understands the value of delivering the entire lifecycle of F&A services to clients – from process design through to managed steady-state.

Cognizant succeeding in moving from FTE-pricing to outcomes (High Performer)

Despite a smaller footprint in F&A BPO, Cognizant’s clients all cite the firm’s desire to move as aggressively as possible to outcome-based delivery of F&A, which is already working very effectively. Well positioned for the As-a-Service Economy and clearly one of the more forward-thinking innovative service providers in business services today.

WNS’ flexibility positions it well in today’s F&A market

WNS has firmly established itself as a strong “pure play” alternative to some of its larger competitors, winning against the top tier on several occasions. The firm is big enough to deliver and small enough to respond. Has received many positive accolades from many market clients for its hard-work and client focus. Also developing a strong reputation for it’s F&A analytics focus.

TCS’s vertical focus a strong potential differentiator for “As-a-Service” F&A in the future (High Performer)

Continues to believe – and invest – in strengthening industry knowledge, and investing in key leaders within industry segments who provide domain intensive guidance. Proprietary TRAPEZE Tools – available both in web-based and mobile versions provide compelling governance support in F&A. Its innovative approach to Robotic Process Automation in F&A has been lauded by some clients and impressed the HfS analyst team (see link).

EXL a strong all-round performer with a consistent transition and process improvement performance (High Performer)

The no-surprise transitions and managing change strategy works well with EXL’s clients. When operations are stabilized over the 12-18 month period, EXL shifts focus with its EXLerator process improvement methodology and collaborates effectively with clients for overall process optimization, target operating model, platform changes, business impact value drivers, and scope shifts. The recent appointment of Henry Schweppe is will help EXL compete for larger, more transformative engagements.

So, Phil, what is your prediction for what this market will look like in three years’ time?

F&A represents the perfect blend of “traditional” labor arbitrage and evolving “As-a-Service” delivery. Nowhere is more ripe for advancements in robotic process automation, analytics and outcomes models than F&A. The winners will be those which can maintain effectively their global delivery scale, but combine it effectively with the As-a-Service ideals, where clients can “plug-in” to the service provider experience, where cloud and automation are at the core of the offerings and designed with these in mind, as opposed to being retrofitted as an after-thought. However, people are still the key ingredient in F&A, and the market leaders are all differentiated not only by the scale – but the skill – of their delivery talent.

This market will continue to grow at an annual clip of 5-10% for several year to come – remember, it took the world of finance a decade just to make the jump from Lotus 1-2-3 to Excel. It’s going to take a while to get ahead of the As-a-Service curve!

HfS readers can click here to view highlights of all our recent 20 HfS Blueprint reports.

HfS subscribers click here to access the new HfS Blueprint Report, “HfS Blueprint Report 2015: Progressive F&A BPO Services“

Each year, most of the service providers like to bring together their multifarious assortment of “influencers” to pitch their capabilities, reinforce their strategies and make sure their key executives have some sort of relationship with the key people in their space who talk to their clients.

Having been in and around the analyst and consultant community for the last 20 years, these gatherings were typically 90% attended by industry analysts, namely Gartner, Forrester, IDC et al and a few small boutiques, independents, bloggers etc who mattered to them. Then, about five years ago, most the service providers had the bright idea of tacking on a handful of sourcing advisors who could also benefit from the same experience of being influenced. All of a sudden, these events have become about 60% advisor, 40% analysts. I think only Accenture and IBM are the only service providers left which actually separate the analysts from the advisors these days.

As a recent example of this, I had the privilege of attending Capgemini’s influencer day in an arctic Chicago last week. And I was impressed at the line up of legends attending from the sourcing advisory world – characters like Peter Allen (Alvarez & Marsal), Harvey Gluckman (ISG), Kevin Parikh (Avasant), Chip Wagner (Alsbridge), Peter Bendor-Samuel (Everest), Tom Torlone (PwC) – all accompanied by teams from their advisory firms. I have to hand it to Capgemini’s advisor relations team – no-one has ever assembled a gaggle of advisors together in one place quite like they managed. I then popped into WNS’ influencer day in New York and a similar line up ensued there… with additional SWAT teams from KPMG and Deloitte adding to the festivities.

This change in dynamics is having the following impact on the way these service providers interact with their influencers:

Pros

Much better questioning from advisors. It’s almost a relief to hear sensible, real-world questions from advisors during these sessions. Long gone are those days when you’d get analysts piping in with their drawn-out abstract thought-patterns, which actually were never really supposed to be questions, more statements of how clever they were.

Advisors are much more social. Most the advisors like to network – even with their competitors. Always good to exchange views with (some) them over a glass of wine. Most analysts just disappear to their hotel rooms at 8.30pm, never to resurface.

Advisors have more energy and passion. Most of the advisors enjoy what they do – they are passionate about services and are hungry to learn more. Most of the analysts have been doing this for decades, are clearly jaded and exhausted by these dog n’ pony shows, and are just going through the motions these days.

Cons

Advisors have become quasi-competitive with most service providers. As the outsourcing service providers look to move further up the value-chain with their client engagements, they are essentially offering the same services as most the advisors. All I hear from the leading advisory firms, today, are how they are running consulting practises in digital transformation, robotic process automation, CFO services, GBS etc. These ambitious advisors want service providers who are only really focused on the efficiency-driven services further down the value stack, so they can profit from the consultative and governance-driven services they can layer on to their clients’ outsourcing engagements. However, the more complex clients’ needs are becoming, the blurrier the line is becoming between what service providers and advisors deliver.

Advisor “influence” is much harder to track. With analysts, the goal for service providers is simple: dazzle them and hope they will write about them to their readerships and social followings. Tracking their influence is easier when there is a tangible outcome, such as a piece of research or a blog post. Most advisors won’t write anything – even with a gun to their heads. The service providers simply hope the advisors are moving them up their evaluation curves and pushing more deals their way.

Most advisors with deep client engagements do not have time for service provider days. Having been on the advisor side myself, I can tell you that I never had the time to take entire days out to hobnob with service providers, unless I had a lucky week of break-time in between client engagements. Most of the advisors who do have the time for these service provider influencer days are clearly the executive-level leaders not so ensconced with the day-to-day execution of advisory services. Hence, the service providers are hoping this bedazzling of the advisor leaders is somehow translating its way to the advisor deal teams doing the site visits, service provider selection sessions etc.

The Bottom-line: The influencer model is clearly broken in the services industry – a new breed clearly needs to emerge that advises, analyzes AND influences

In short, the evolving confusion over advisor and analyst roles is a result of the lack of real influencers in the industry – experts who not only talk to buyers on a daily basis, but also share real insights and leverage data for them. In today’s world, advisors and analysts are very different animals – and the winners will ultimately be the ones which can fuse together the two worlds.

Oh no! We’re back on your laptop screen this 26th March at 11.00am ET.

Yes, that sad little attempt by HfS to assemble a cacophony of industry advisor gurus onto one webinar platform just refuses to go away…

And we can see that you just can’t stay away from the entertainment either, so let’s just launch into our latest attempt to create a little bit o’ clarity to your confusing worklife.

Please join our latest suite of sourcing savants of sourcing soliloquy later this month as we violently argue (or agree) on the the following burning topics:

What are the burning platforms driving enterprises to make real changes to their IT and Operations infrastructures?

First we get hit with “Digital”, then “Robotics”, then “Artificial Intelligence”. Is the dear lord of sourcing smoking something, or is there some real substance into what is happening in our industry?

Does this mean that our traditional outsourcing industry is dying? Are enterprise clients really evolving this quickly to these As-a-Service models?

Is our talent keeping up with this As-a-Service revolution – across buyers, advisors and service providers? And what can we do to retrain ourselves and our staff to get with the program?

So what does our future really look like is this new world into which we’re venturing, when we show up to work in our iCar and are served coffee by a robot?

Yes, we will really answer all those questions for you once and for all, or at least our esteemed panelists claim they will:

These are really exciting times for the services industry, where little upstart “Born in the Cloud” As-a-Service providers can sneak up on the traditional service providers and deliver pure cloud-based services in a model that was designed to be in the cloud.

And when you design services for pure cloud delivery, they have to be seamlessly automated at their very core. The services ethos is about enterprises operating smarter, not cheaper… and as a result will likely save a ton of money because they end up simply running more effectively.

One such irritant to the traditional services model is OneSource Virtual (OSV), which has built up a compelling business delivering business process service offering for clients around Workday’s HR and F&A SaaS platforms. OneSource Virtual is an As-a-Service provider – there is no transition to becoming one, it was born as one with As-a-Service as it’s intended delivery. And when you consider one of OneSource’s clients is Uber, it just makes for one harmonious As-a-Service mash-up…

The exciting value OSV is bringing to the table is its services are focused on real business support areas, such as organizational design and workforce analytics, in addition to the transactional needs of clients in areas such as payroll fulfillment, or accounts payable. And this also creates exciting jobs for onshore staff who can apply more consultative, value-based capabilities to service their clients. This is the As-a-Service Economy, where service jobs are becoming more challenging and interesting, where real business services are delivered on-tap and clients can access services designed to meet the needs of the modern business, not just some legacy back office designed on a mainframe cluster back in the late 1970s…

OneSource Virtual’s service delivery was built with RPA at its core

We’ll admit it. We didn’t see the robots for the trees. We’ve been so focused on how Robotic Process Automation is being implemented across legacy application environments, we missed how it is also being rolled out in “Born in the Cloud” business environments.

Last Friday, we spent time with the As-a-Service provider OSV, which has built business process service offerings around the Workday SaaS platform for HR and F&A. While it is true that Workday itself has automated many processes that require more manual intervention in other applications, OSV has gone taken this one step further.

With the development of its proprietary service delivery environment Atmosphere, built on force.com, OSV has created a platform for the extraction – and then automation of – recurring processes across their base of hundreds of clients. This is a critical development, because together, with consistency in the code base of Workday across clients, the automation in Atmosphere allows OSV to establish very high levels of productivity in tasks where human agents are still required.

Especially compelling is that fact that OSV has not developed its Atmosphere and this model of shared automation after years of running individual silos of client delivery, as several other service providers are now trying to do. Instead, OSV was founded on this principle of shared automation from its inception.

In essence, this means that OSV is already operating at the highest Level of the HfS Maturity Model for Robotic Process Automation that we released in November 2014. This Level, “Institutionalization” describes a common theme of broad strategic commitment by a service provider to the transformational potential of RPA on their clients’ business and operations. Any service provider characterized by this Level is making a sizeable investment in RPA, with a view to creating a fundamental change in the commercial and delivery operations of their clients’ business operations.

Other service providers are striving to move aggressively into the Institutionalization Level, however, they are doing it by retrofitting RPA into their established business, as opposed to develop new client delivery environments with RPA at the core.

Net-net, it’s time to really get down and dirty with RPA as a core component of the service delivery platform – get ahead of this unstoppable trend as opposed always chasing it…

Mike Sutcliff is Group Chief Executive, Accenture Digital (Click for bio)

Two buzzwords have re-ignited the world of global services since “offshoring” became so passé… Digital and Automation.

And the two are inextricably linked – you can’t really digitize your business processes until you have effectively automated them. And if your industry requires you to have that digital interface with your customers and suppliers to survive (and that pretty much includes all industries today), you’re pretty much done for, if you haven’t build that automated process layer as the foundation. And if you need more evidence of this, please take some time to read our recent report on the impact of Digital on business services.

So surely this is the gravy train for ambitious service providers to jump to the needs of their clients to save the day? Or is the business world changing so dramatically that this is simply going to be one insurmountable challenge too far for many enterprises, and they might as well give up now?

So let’s hear from the one service provider that dusted off the “Digital” terminology from the dictionary and reapplied it to the world of services. We managed to get some face-time recently with Accenture’s Mike Sutcliff at his firm’s Global Shared Services Conference (GSSC) in Prague, to hear about how his group is developing its digital capabilities and applying them to the world of business operations and shared services…

Phil Fersht (CEO, HfS): Mike – Good to connect again! Tell us about your background. How did you come to lead the digital practice for Accenture?

Mike Sutcliff (Group Chief Executive, Accenture Digital): I’ve been at Accenture for 27 years. In the early 1990s, I founded the Finance Management Group which developed our shared services business. Then I got the opportunity to establish a new business. I became interested in analytics; I wanted to understand how analytics could bring more value to companies. I studied how enterprises created data as a mass that they then could leverage across the organization. I combined my experience in financial services with my new understanding of these growing fields to form Accenture Digital, which brings together our capabilities around e-Commerce, digital marketing, social collaboration, mobility and analytics.

Phil: “Digital” is the industry’s new hot button; everyone has jumped on this and is coming out with their own digital practices. How is Accenture’s digital practice different from the offerings of other tech-based services firms?

Mike: First, we have history. We’ve been working on various parts of our digital business for a decade, collaborating with our technology partners across the entire ecosystem. Over time we developed our offering that now the marketplace considers digital.

Second, we don’t use digital as a group of technologies. We think about digital as:

Connecting people

Creating mobile capabilities

Embedding real-time analytics into enterprise operating models

We do this across different industries and geographies. When we talk about the digital customer, we think about how citizens engage with their governments, how patients interact with their healthcare providers or how consumers engage with retailers. We try to put together the digital pieces in new and unique ways to change the way the world is working.

Phil: Mike, The consensus at the recent GSSC conference is that shared services operations are ideal to house a digital CoE (center of excellence). In your opinion, can digital services become a genuine innovation engine for business operations?

Mike: Absolutely, Phil. Digital services allow enterprises to house expertise in different types of data; for example, they could create an analytics center of excellence. They could also innovate by doing mash ups, where you combine technology from inside the organization with technology from others in the environment. And these digital technologies can help individuals capture market share–it could be in a call center, agent network or a physical store. The business unit can now think about how digital technologies can enable each business process at every point in the customer interaction. In my opinion, all of these are interesting opportunities for shared services organizations to accelerate the innovation that’s happening within the business.

Phil: Based on your experience, how can operations executives improve their digital capabilities? Is there a big opportunity here or is it too late?

Mike: It’s not too late, Phil! Digital is a fantastic opportunity. Here’s why: There was a cycle of early adoption which required executives to act as general contractors to put together their own solutions as the technology matured. Today solutions have been tested, developed, even packaged as subscription services.

Phil: What is your first piece of advice to people starting out in a digital transformation, Mike?

Mike: Understand you need to design business processes for the mobility environment. Today your employees, customers, business partners and supply chain are all increasingly using their mobile phones as a business tool. Mobility is more than people using their handsets to access information, which was the hallmark of the first generation of mobility. Today organizations have to embed computing capabilities into centers and analytics into devices. Things are mobile as well as people. We can design much more effective business processes if we think about what it really means to untether people from the laptops or desktops. People are no longer just sitting in an office or stuck in a static physical location.

Phil: And what is your advice concerning analytics?

Sutcliffe: Enterprises need to take the next generation of analytics, which includes machine learning, cognition engines and structured text mining, among other things, to take advantage of all the information that exists. That includes the information both within your company and in your business environment. We were not able to collect and amalgamate these in the past. Then use the combined data to do something you couldn’t do in the past. The new digital tools allow companies to discover and act on insights in a more practical way because trends are become more economically visible than in the past.

If companies understand both the mobility and analytics involved, they can start imagining more effective business processes. That can start a revolution internally, a revolution that challenges the existing constraints in current operating processes.

Phil: What do you think is the broader societal impact of digital transformation? Are we going to see real issues arise due to a lesser reliance on humans? Do you see real growth opportunities for professionals or are we heading into a very different future?

Mike: I am an optimist. Yes, technology is destructive. In the disruption there are different short and long-term benefits to different members of the ecosystem. Like other technologies before it, digital will change the way we work. People will have to adjust to the new way or potentially be eliminated in order to make a process more efficient.

Yes, introducing new ways of doing things is a challenge in the short term. But this change is necessary because technology:

Facilitates efficiency and achievements

Allows employees to work smarter and faster

Permits employees to be mobile and work from anywhere

Enables everyone to interact at a deeper level of detail

Phil: Can you provide a real world example?

Mike: We developed a solution in India for the farming community, which is composed of a lot of small family farms. Traditionally these farmers don’t take advantage of the available science to determine what kind of fertilizers to use depending on their specific land and the crops they want to grow. It was just too expensive to understand the soil content, weather patterns and chemicals that would improve their yields.

Accenture combined digital technologies which gave them access to this information and expertise. The result: they were able to make better decisions. They put the correct amount of the right chemicals in the proper places based on the weather and crop patterns. Indian farmers using this simple combination of technologies significantly increased their crop yields per acre, making them more productive.

Look at how distance learning has changed education. Or the new ways doctors and technology are delivering healthcare. These are all structural changes in the way people do things. These structural changes do more than just make us more efficient. That efficiency enables some of us to work on problems no one has solved yet-like how to tackle new forms of cancer or reorganize cities to reduce congestion. Digital technology has freed us to work on societal issues we all know we need to work on.

Phil: So…you are anointed as Digital Emperor for one week, what two things would you do to change the industry?

Mike: The first thing I would do, Phil, is create a public directory of all known sources of data that enterprises could combine with their own data. This is a good move because many of our clients simply don’t know what’s out there or how to access what they need. I believe we can improve our society significantly if we had a better understanding of how to use the data. For example, looking at energy usage, crop yields and healthcare requirements from a global level allows us to do a better job of feeding, housing and clothing the world’s population. I think this global data amalgamation will mature fairly quickly.

The second thing I would do is engage more aggressively with both regulators and the various layers of government to challenge the current regulations. Are the historical regulatory control structures we have in place now going to be equally valid in this new digital world? I want to determine if what’s in place currently is the most effective. Now that we’ve got access to these digital capabilities we can determine the most effective regulations to put in place. Please note I am not challenging the need for effective regulation. What I’m saying is we need even better regulation. It’s time to start now (it’s not too early!) to start engaging government in this type of conversation. How can we work together to create digital policy to allow more effective regulatory controls moving forward?

I’m sure you’re surprised that I would talk about the importance of regulation as a digital emperor. But I think the pace of digital change is significantly faster than the government’s reaction to that change. Hopefully, early conversations with government regulators would allow the world’s population to gain advantages from the digital technology faster.

Phil: That’s right, Mike. Most governments are still catching up to the impacts of earlier Internet evolutions. Maybe we can help them get it right this time… I appreciate your candid views here – am sure our readers will enjoy reading them.

Mike Sutcliff (pictured) is Group Chief Executive, Accenture Digital. You can download your complimentary copy of “Disrupt of be Disrupted: The Impact of Digital Technologies on Business Services” by clicking here.

There’s nowhere better to test the temperature and mood of the global IT and Business Services industry than at India’s NASSCOM Leadership Forum, where the bigshots from all the major India-heritage providers, and the leaders from the major Western-centric providers’ India operations, get together for three main purposes:

1) To be seen as a player at IT services’ premier networking fest;

2) To partake in presentations and panels that are all pretty much sung from the same hymn sheet;

3) To have great conversations that cut through the glossy digital lipstick veneer and elaborate entertainment, to debate the reality of whether this industry can truly evolve beyond its current “all about scale” predicament.

And this year, did we get just that – with a new energy that has been lacking in recent years since the recession. What I love about this networking event is the sense of common purpose, community and belonging you get as part of the services industry, which you do not get at most other events (especially Stateside, where some conferences still seem to be stuck somewhere in 2004…).

At NASSCOM, you don’t feel that outsourcing was that “accidental career” choice you just happened to fall into because you could never figure out what you wanted to do with your life. You actually feel part of something – and part of history as well as the future. Just bumping into the legendary (and very fit and energized) Pramod Bhasin (the founder of Genpact), who could (and probably should) be lying prostrate on some beach checking the number of zeroes on his bank balance – and hearing his passion for doing more for the Indian services industry – tells you something about the DNA that will keep brand India at the forefront of technology-driven business services for a very long time to come.

How India’s services stars can shine with their Digital lipgloss

But let’s not get too carried away by the hype of the moment. India’s services economy has some big challenges, but it really does have the nuts and bolts to lead the way into this unraveling Digital future, and play a significant role in the emerging As-a-Service Economy.

There are three dimensions we need to consider when we evaluate India’s ability to continue on its services growth-path:

1) Leading with digital technology and an appetite to cannibalize short-term revenue for longer-term profitability and value. HfS success probability = 90%

For example, the more I learn about Robotic Process Outsourcing (RPA), the more convinced I am that some of the ambitious Indian-heritage firms will be at the forefront of development and capability here. I am already witnessing a strong appetite to cannibalize some shot term revenue with clients to develop beta solutions that can be re-used for the future, and scaled across multiple clients. The common-sense to transform a $10m engagement that has 20% profit margin into a $7m engagement at 50% profit, is not just lip service from the service provider executives attempting to placate cynical analysts, we hear this from an increasing number of clients.

Meanwhile, too many of the traditional Western-centric providers have massive scale deals involving hundreds, and even thousands, of FTEs and have a real problem when it comes to changing the pricing model at the risk of taking a hit on short term income. Sadly, most of the incumbent service providers are today looking at their current client portfolios and thinking “Why on earth did we take on some of these low-value FTE-centric deals where the clients refuse to do anything beyond complain about us not taking out enough cost, and are too insecure to increase the scope of the work to create a more value-driven, rewarding relationship”.

Conversely, most of the leading Indian-centric providers have built up their businesses on a plethora of mid-size deals ($5-$25m) where the FTE model simply will not make sense for their clients in 3-5 years’ time – why pay for the same 20 bodies every year? They will want to see some incremental improvement on cost and efficiency, and will change to a new service provider if their incumbent insists on a status quo scenario. What’s more, RPA will shift services to be delivered smarter not cheaper, where business-centric staff can focus on delivering services at higher value, as opposed to surplus numbers of programmers and transactional staff being employed simply to keep workflows and operations functional.

There are a few Indian-heritage providers today who must be thanking their lucky stars they never dived headfirst into the lift-and-shift BPO business – it’s so much easier to drive value into less complex engagements, where there is less risk as stake to make a few sensible bets for the future.

With regards to mobility, I have only been impressed with the focus of many Indian-centric providers to embed consumer-centric mobile processes into enterprise solutions. Digital is about bringing the service providers closer to the customers of their enterprise clients, and is driving the need for capable mobile, social and analytical solutions to be weaved into the service delivery. And however to do this, you really need to be able to transform the automation layer for clients, which is the foundational building block for digital transformation.

And last, but certainly not least, is analytics. I am only impressed at the appetite of Indian-heritage firms to take on analytics service for clients, no matter how small or complex the client requirement. Without trying to make a sweeping generalization (and clearly failing to do so), Indians just love data. Analyst firms hire analysts in India because they are just so adept at foraging around for data points, crunching them up and presenting them. The challenge here is going beyond generating great data – and truly interpreting it for clients in relevant business contexts, which takes me to the second dimension…

2) Leading with business services. HfS success probability = 60%

This is where India’s stars are facing some significant challenges, namely transitioning and training staff to approach client solutions from more of a business, and less of a technology, context.

In 2020, I am willing to bet my house on the fact that NASSCOM will be all about business solutions, with noone being remotely excited by the digital plumbing that has made it all possible. So what does this mean for the millions of developers who just live for code?

It means we’re going to need a bit less tech and a lot more business-context support. It means India’s universities need a bit less ABAP and a bit more MBA. It means India’s most ambitious service providers will be investing heavily in world-class HR to identify their talent potential, retrain it and frame entirely new career paths. It means India’s services industry leaders and populace are going to have to demonstrate a stomach for change, the likes of which they have never experienced.

At NASSCOM, about 40% of the service providers I spoke with really get what’s happening, and are already making some investments to make this tech-2-busness shift; about 30% recognize what’s going on, but are still figuring out their play; however, a good 30% are like deer in the headlights – they just can’t grasp the change and I generally worry whether they can continue on a healthy growth path, and can break out beyond their pure-tech approach to service delivery.

Yes, talent transformation is a big, big challenge for India’s services economy, but it’s not as if all the North American and European service providers and consultants are making massive investments to change their delivery model? Most of they seem more focused on shedding costs than buying capability.

3) Managing the pace of change clients demand. HfS success probability = 75%

This is critical, in my opinion. Nearly all of the solutions today are largely being driven by vendor-push as opposed to client-pull, which is fairly typical as new ideas and technologies are launched onto the market. At HfS, we get calls from clients to discuss Digital, RPA and so on, but more because they just want to know what the fuss is all about, than the fact they are ready to move with an executed strategy and plan.

Most of the traditional incumbent Western-centric providers are masters at managing the pace of change that works for their clients. In my experience, services clients are falling into two quite distinct camps;

‘Born in the cloud’ firms which are rapidly emerging today, who want everything sourced, delivered in the cloud, mobility-enabled and perfectly automated. They don’t have that legacy operations infrastructure of dysfunctional ERP instances, poorly stitched-together processes and staff still living somewhere in 1996 running it all. They will also make up a good portion of the Global 2000 in 2020. These clients are demanding a fast journey to As-a-Service, and want to move to a platform-driven environment as quickly as they can, where they can literally “plug-in” to standard digital processes and capabilities. This is where investments in digital platforms that bring immediate process solutions is critical – and the ability to work at speed with impatient clients not waiting to make massive upfront investments in transformation services.

The ‘traditional enterprise’, which has a quagmire of legacy business process and technology that need overhauling and will take years to ease its way toward as As-a-Service mentality. Change is expensive and painful for these firms and they will only really invest in it when their core business model is under true threat. For example, healthcare payer firms in the US must have digitized customer management capabilities now they are directly servicing consumers via their iPads and not only corporations. And most retailers will simply die if they can’t have digitally effective commerce solutions to sell their wares and manage their supply chains effectively. While these clients will demand fast change, most have/are/will struggle to evolve from breaking from their legacy systems and writing off their technical-debt. Moreover, they need the skilled consultative ability of a services partner who can help steer the change management program for them at a pace they are comfortable. This is where Indian-heritage firms can often struggle, where a “white shoe” approach is often needed.

India-heritage service providers need to figure out how to approach their clients to develop a plan to take them where they want – and need – to go. Most of today’s Indian-heritage providers struggle to diversify their approach with clients – they are trained to sell, sell, sell and it often results in clients being turned off by their approach. The Indian-heritage firms need to make serious changes in how they manage their clients, the behavior of their account managers, and their ability to have much more of a listening and consultative relationship.

The Bottom-line: Complexity and change drive major opportunities. This is India’s time to prove it can do it once more

When India built its IT services economy in the 80’s, 90’s and 00’s to become truly formidable, it did so with incredible purpose from its leading IT services providers and support from its government. The plan was simple – go after the incumbents like EDS and IBM with much lower-cost offerings that changed the game. The incumbents were asleep at the wheel and simply let it happen. In the last few years, the likes of Accenture, IBM, HP and Capgemini have developed huge Indian organizations to remain competitive and win back some of the lost market share.

So today, the playing field is now a lot more level, and there are no more surprises in store – everyone will have their Digital/RPA/Mobile/Analytics platforms beautifully designed on a PowerPoint deck winging its way to you very soon. This is now more about talent and culture than anything else – and the race is on across the leading providers to develop their own people programs to deliver more business-centric solutions to clients, to solve problems proactively than merely fix processes.

This isn’t going to be the cakewalk it was in 2003, when all you needed was an army of programmers and project managers, and a decent internet pipe. However, where I see India having a genuine advantage here is an ability to go where the business is – a tenacious culture to push new ideas and innovations onto clients, many of whom love the humble, can-do attitude of most of the leading Indian-heritage service providers. Whether all of these firms can become more MBA and less ABAP is still very much open to question, but at least the smart ones have their eyes wide open and know what they need to do.

Net-net 2015 is a phenomenal time to be a services professional – there is so much opportunity for career growth, whether you are an analyst, consultant, practitioner or service delivery professional. Complexity and change drive new growth and opportunity – it’s time for the ambitious people to get ahead of this and embrace the challenge!

Phil: So, if you were to look out five years to 2020, what do you think we will be talking about?

Phil: So, if you were to look out five years to 2020, what do you think we will be talking about?