With the HfS Blueprint season now in full swing, we can celebrate the coming-out party of one of our rising star analysts, Barbra McGann, who’s put together one of our finest pieces of research (yet) looking at the rampant Population Health and Care Management business services industry:

There’s such a loud call for change in the U.S. healthcare industry these days, Barbra. Please tell us a little bit about what you see going on…

Healthcare is just too complex. Through the Patient Protection and Affordable Care Act, we all have the right to access healthcare, but for a lot of people it’s still difficult and expensive to do so. Healthcare providers and payers are on a mission to take the “sting” out of healthcare. The goal is to make healthcare more personal, user-friendly and cost effective. That’s a monumental task and requires change in the way many of them do business. It will take some creativity and new approaches to get it done.

Of all the activities in healthcare, Barbra, why did we zero in on Population Health and Care Management?

Organizations need to help individuals engage and manage their own health – empower them to be healthier. This is the scope of population health and care management. Population health involves understanding who needs what kind of support to live a healthy lifestyle, reaching out and connecting early when there is potential need for medical support. Care management covers the coordination of care for people who are managing chronic conditions, helping them achieve better health, and the authorization of that care from the financing entity. While there used to be a pretty clear distinction between healthcare providers addressing population health and health plans covering financing and care management, these two are overlapping more and more with the focus on the individual as a whole rather than on a single stage.

So How can service providers help healthcare organizations get more personal with consumers, members, and patients?

Service providers have been providing BPO support for healthcare organizations for years now to operate more efficiently and lower costs. And to do it, they have hired clinical executives and staff, developed industry certification and training programs and technology enabled IP, and established onsite and global centers. We believe they have the capability now to work closely with healthcare organizations of all sizes to help them be successful. Service providers have proven they can partner to help increase adherence to care plans, reduce readmissions, and reduce administrative costs, for example. They work with sets of population data to help design models that identify and drive interventions, and make calls to targeted patients to remind them about appointments and help them figure how to get there, and provide smooth back office operations for utilization management with a combination of skilled clinical and non-clinical resources and automation.

How is this Blueprint going to help current and potential services buyers?

There’s a lot of discussion about healthcare IT capability for population health, and not much about BPO. So we took a look at which service providers are offering business services and experience addressing:

Consumer engagement and interaction: identifying whom to target and reaching out with assessments, wellness programs, and medical interventions

Utilization management: processing authorizations, reviews, appeals and grievances administration for medical care

Care Coordination: referring and enrolling members and patients in programs, helping them navigate and manage their care and administration, planning and documenting discharge after hospitalization, and remote patient monitoring

Performance management and operational analytics: measuring outcomes, analyzing, reporting, and providing insight on metrics for administrative and compliance purposes.

It’s a collection of activities that together help healthcare organizations manage outcomes focused on well-being, health, and care – wellness in every day life or specific times like pregnancy, adherence to care plans and medications, emergency room visits, hospital stays, and readmissions, for example.

How did the Blueprint analysis turn out?

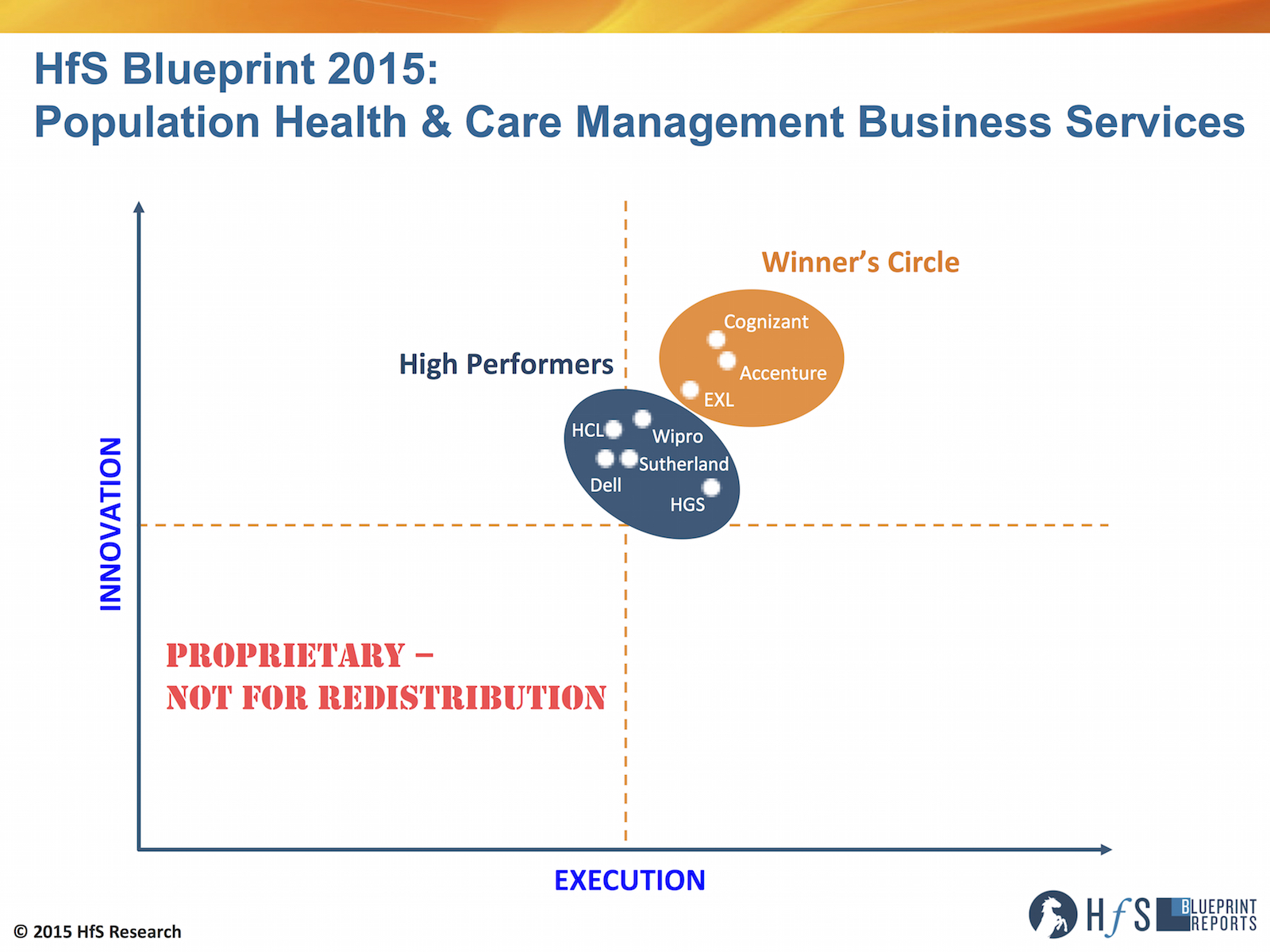

There are 8 service providers who stepped up to the opportunity to share their current capability – skilled resources like clinicians and healthcare data scientists and technology IP and platforms – as well as vision for the future of population health: Accenture, Cognizant, Dell, EXL, HCL, Hinduja Global Services (HGS), Sutherland Global Services, and Wipro.

Winner’s Circle:

Cognizant, a flexible, adaptive risk taker; led by technology and building up the strategy and consulting layer

Accenture, an engaging thought leader with a full suite of services and community connections

EXL, leveraging platform-based business services, analytics, and relevant depth in financial services into healthcare

High Performers:

HGS, a quiet, smooth, dedicated operation with unique linkages to hospital for talent, delivering what’s asked.

Wipro, partnering with software / SaaS provider to offer patient-centric platform-based business services

HCL, tapping into and evolving client systems and customers with a technology led healthcare program focused on patients

Sutherland Global Services, creating consumer, patient, and provider experience through close collaboration

Dell, with a technology led, data driven, partner-oriented approach

What separates the Winners Circle members from the High Performers is the depth and breadth of experience in healthcare business services within this value chain, clarity of vision for population health and care management in the healthcare industry, and collaboration with clients to date. Each of these service providers has capabilities that can match a business need or challenge of a service buyer. The key is to make the right match.

Thanks for your insight, Barbra. So to sum up this Blueprint research, how do you see this market evolving further down the road?

Barbra McGann is Managing Director, Research, at HfS (Click for bio)

For the most part, population health management has been the realm of healthcare providers, while payers drove care management. Healthcare providers in an annual ‘check up’ looked for opportunities to identify and intervene in potential on-set of health issues. Payers identified candidates for care management after an event through claims analysis. But all healthcare organizations, and pharma and medical device companies, need to help in achieving a healthier society. So, activities are overlapping and shifting as healthcare becomes more proactive and individualized.

To be successful, services buyers and services providers will need to build tightly knit ecosystems and interoperable networks of technology, process, and people. We will see an increase in hybrid operating models, therefore, that combine internal and external resources. This enables them to get to know and connect with patients in a more individual and friendly fashion, and take the “sting” out of healthcare.

HfS readers can click here to view highlights of all our 23 HfS Blueprint reports.

HfS subscribers click here to access the new HfS Blueprint Report, “HfS Blueprint Report 2015: Population Health and Care Management Business Services“

Meet Tom Reuner, HfS new Managing Director for IT Outsourcing Research, with wife Ayesha

As you all undoubtedly know by now, at HfS we are relentlessly dragging the world of IT and business operations kicking and screaming into the As-a-Service Economy. So what better than to convince the only other analyst with real chops in autonomics and cognitive computing (who wasn’t at HfS) to come and become part of our bandwagon of belligerence?

Not only does the arrival of Tom Reuner corner the analyst market in autonomics and cognitive computing for us, he also brings real depth in IT services and adds to our growing European analyst presence. He’s also a terrific bloke with great taste in premier league football teams.

So, without further ado, let’s hear a bit more about the latest excellent addition to the HfS analyst ranks…

Welcome to HfS, Tom. What on earth went wrong in your life to have ended up doing this? Tell us a bit about your background…

Cheers Phil, I am really excited to join HfS. And well, unlike my lovely wife I hadn’t learned anything proper. Back in the days I was expecting to become a lecturer in history and as part of that I planned to stay for half a year in London to do research for my PhD. But as so often in life things turned out quite different. For personal reasons I ended up staying in London and had to completely change direction. To cut a long story short my first job took me to a company I had never heard of before at that time: Gartner. I never looked back and the rest is “history”.

I just love being an analyst, meeting constantly new people and track technology evolutions through the course of time. I am getting a kick of being able to help client think in different directions and to help them to overcome their business challenges. After Gartner I had a stint at the buy side with KPMG Consulting. But my heart was always with being an analyst and I had the privilege to work for some outstanding organizations and with some inspirational people. My career took me to IDC to hone my consulting skills, I ran my own company for a while and learned lots from marketing to boring cold calling. Before joining HfS I worked with some great folks at Ovum, where I had the freedom to develop thought-leadership in sourcing and IT Services.

Why did you choose to join HfS… and why now?

The first time I heard suggestions that you guys were tracking me and supposedly considering making me an offer was late in the summer last year. I must admit that it must have been one of the most thorough due diligence jobs in the industry. But on a serious side, when you approached me about joining HfS, I sat up straight and it didn’t take me long to make up my mind up. Over the years and from out the outside I always highly appreciated what HfS had achieved: Being recognized thought leaders, leading the way in evolving the analyst model through the leverage of social media and to constantly push the boundaries to stay ahead of the game. And having been given the remit of expanding HfS’s research coverage across the “As-a-Service-Economy” was the icing on the cake.

What are the hot topics that you will focus on in your new analyst role…and what trends and developments are capturing your attention today?

As suggested I will be responsible for driving the HfS research agenda for the “As-a-Service Economy” across SaaS applications, cloud eco-systems and IT. For the last two years parallel to the efforts by Phil and Charles, I spend most of my time developing a research agenda around process automation and cognitive computing in both IT and business processes (and on purpose I am avoiding the moniker RPA here). We will not only be combining our insights but broadening our focus to the emerging technologies around artificial intelligence and how all these technologies impact the transformation of knowledge work. For me the fundamental question is what comes after labor arbitrage?

With all this talk about disruptive solutions, will the world really look that different in five years’ time?

Some people call me a dinosaur (among other things) but largely I expect most innovations – be it cloud, digital or RPA – to end up in blended models leveraging both traditional as well as hugely disruptive models. Far too often the industry is looking for simplistic answers, the quest for the next panacea, but life is more complicated. The biggest challenge remains how to transition from legacy environments and how transform the clunky ERP backbones that appear to be like millstones around the neck of many clients. And it is exactly that journey that we focusing on at HfS when we are talking about the emergence of the “As-a-Service-Economy”. It is easy to point to beacon clients or to organizations that are born in the cloud, but how are plain vanilla organizations that are representing majority in the market dealing with all these issues? But as to be not shying away from your question, in five years’ time the industrialization will have accelerate strongly, on the buy side consolidation will fundamentally alter the landscape while a new breed of advisors will be finally aiming to tackle the business alignment of IT.

What are you working on first for our clients?

Expanding the coverage on process automation will continue be both a strong focus as well as a means for differentiation. And artificial intelligence as bundled option in RPA or as disruptive innovation will be high on my agenda. But the first Blue Print is likely to be around cloud orchestration and brokerage underlining HfS’ holistic view as to how the “As-a—Service-Economy” might take shape. However, most importantly a significant part of my time will spend on discussions with clients and prospects as to how best to map out the journey into this new “Economy”.

And, what do you do with your spare time (if you have any…)?

Tom Reuner, HfS Research

I wish there would be more spare time as travelling continues to take up a big portion of my time. But on those precious occasions my wife and I love hang out with and entertain friends and family. I feel very privileged that I have married into lovely but huge family. We recently moved house just to be able to accommodate all those visitors. Thus my duties revolve around driving to the airport to pick up family and to be the cook in our house. But if I am honest this probably just a futile attempt to distract me from the sufferings of being a Spurs supporter used to times of despair and depression.

Welcome to HfS, Tom. Delighted to have you choose us as your analytical home and join our As-a-Service revolution =)

Tom Reuner is Managing Director, IT Outsourcing Research, at HfS – you can view his full bio here, email him here and follow his tweets here.

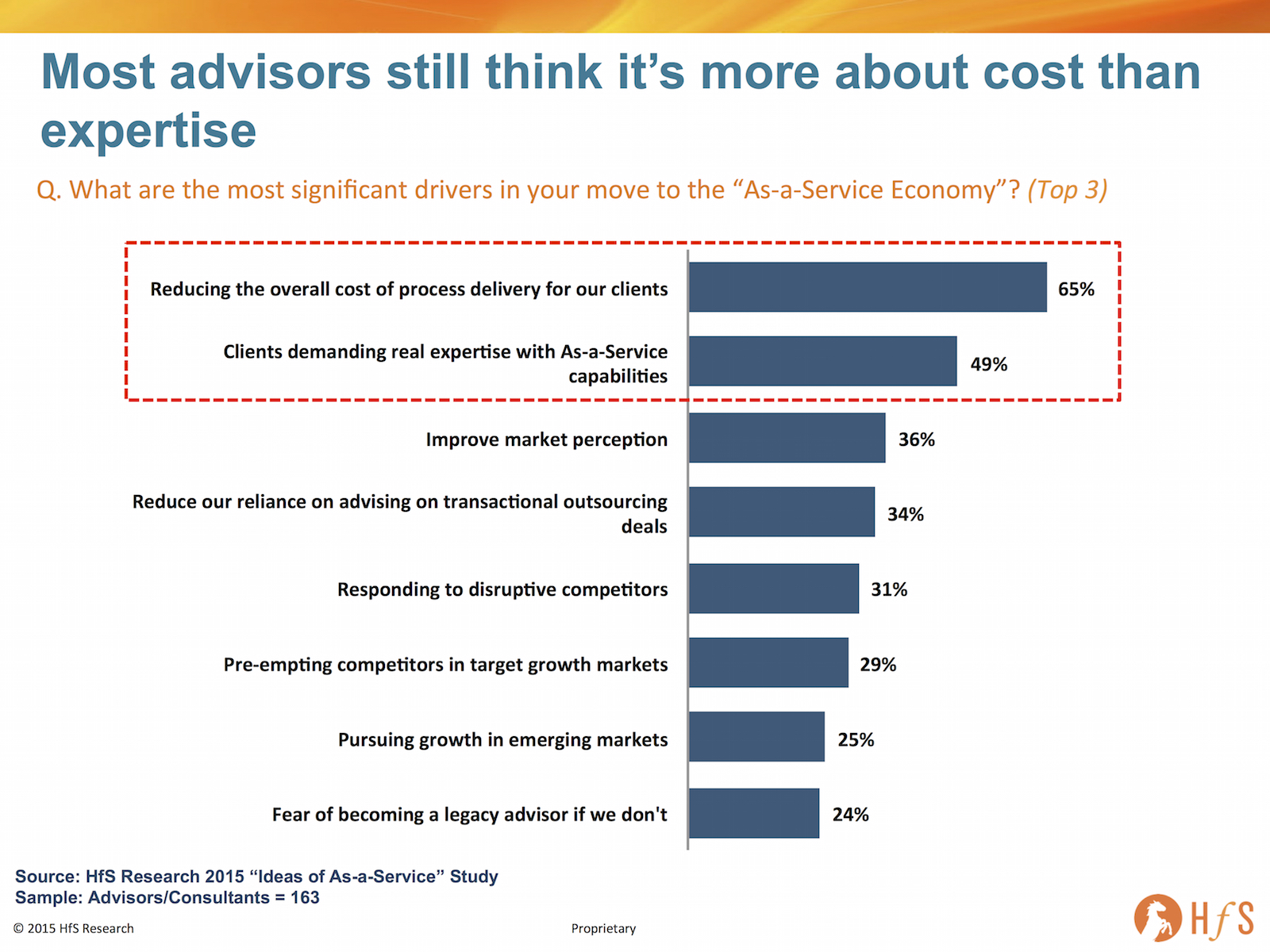

If I told you that only 13% of sourcing advisors have plans to invest in cognitive computing and 15% in Robotic Process Automation skills, you wouldn’t believe me, right?

We’re just about to close off our new study that probes into the ideals of the As-a-Service Economy where 716 industry stakeholders reveal how they are faring with their As-a-Service readiness, intentions and aspirations. And one major services market influencer, the local friendly sourcing advisor, is seriously missing the mark when it comes to sawing off some of the old, to embrace the new. Simply put, at least half of today’s advisors are pretty much, well… Un-as-a-Service. Let’s take a closer look:

Click to Enlarge

Advisors have been schooled on driving out their clients’ costs, as opposed to adding real expertise and value. Encouragingly, 49% of advisors are getting sucked into As-a-Service because their clients are demanding it, but the sad fact of life is that two-thirds of them still think it’s still really all about driving out cost. As-a-Service is all about providers delivering and buyers receiving more productive, more intelligence, more cost-effective services through the use of smarter automation, analytics and business context – and there is, typically, a considerable amount of pain and transformation the client needs to endure to attain that next threshold of productivity.

Hence, the mechanisms advisors need to offer clients to steer them through an As-a-Service transformation, require a very different type of resource investment, than simply adding more deal guys who’ve er… done lots of deals. So let’s see where our beloved sourcing advisors are placing their bets to make themselves more relevant to satisfy their clients’ As-a-Service needs:

Click to Enlarge

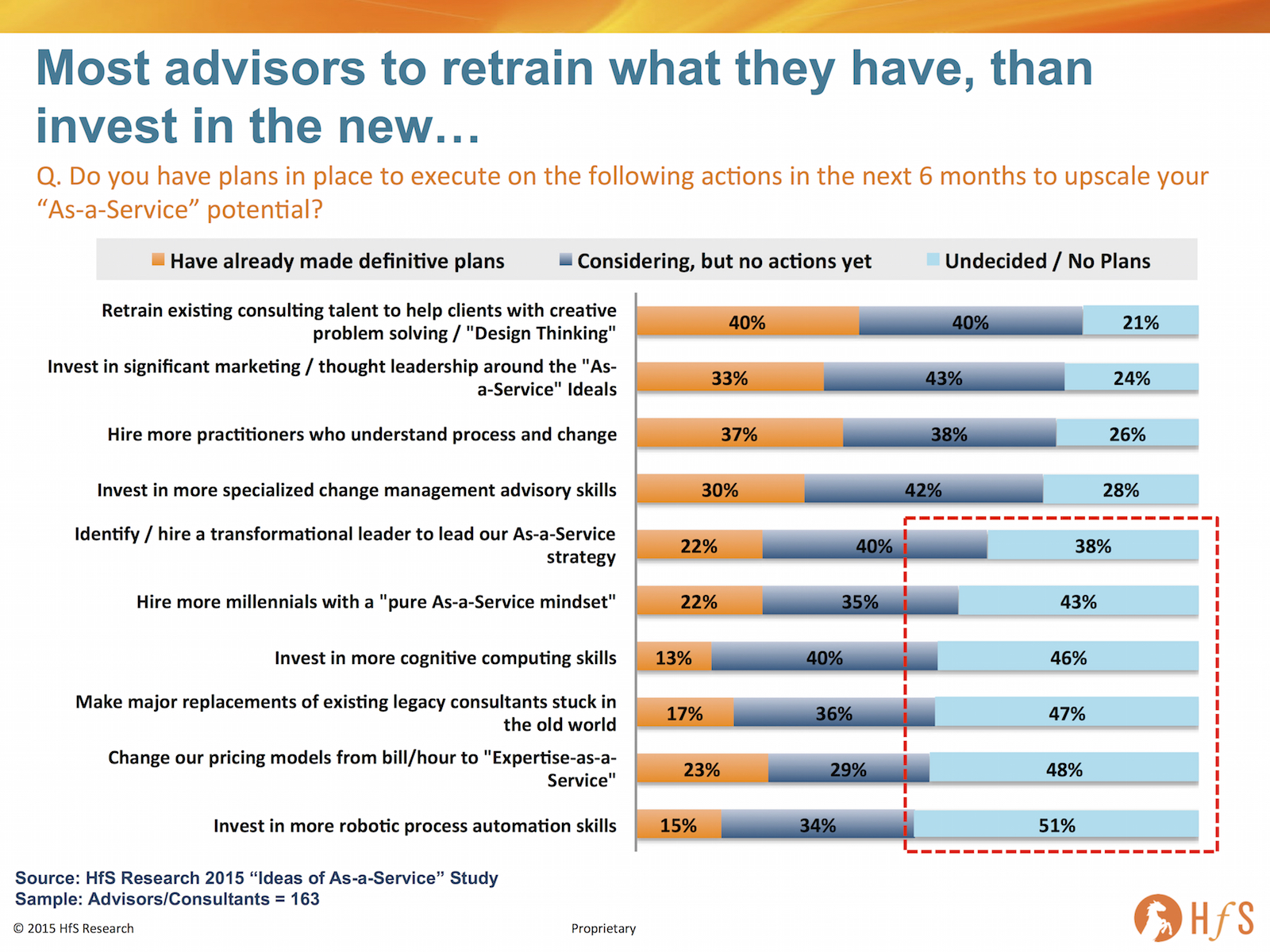

Most advisors are only focused on making cosmetic changes to their existing practices. As you can see here, it’s all about making a few tweaks to what they have, as opposed to making genuine upgrades to their pool of talent and capabilities: 80% are focused on / thinking about retaining their existing team, 76% on puffing up their marketing, and a similar number on hiring process-focused and change management-focused consultants.

A large majority of advisors are unwilling to make fundamental investments to change they way they work with clients. Conversely, only one-in-five actually have plans to hire a transformational leader to shepherd their move to As-a-Service (which I find incomprehensible), or invest in millennials who have As-a-Service potential ingrained into their DNA. Even more depressing is the fact that only 13% have plans to invest in cognitive computing skills and 15% in Robotic Process Automation. And to cap it off, only 17% are actually seeking to counsel out their dinosaur consultants still stuck in the old world of labor arbitrage and big clunking scale deals.

The Bottom-Line: Our industry is lacking the leadership to make the right investments to break away from the legacy outsourcing model

There just seems to be the complete absence of a burning platform to force the change so many industry stakeholders need to make, to prepare for the future model. While there is still money to be made eking out a living feeding off the scraps of legacy outsourcing deals, many advisors, similarly to many providers, are failing to make the adjustments and investments that will position them to compete for As-a-Service engagements as they increase in demand. While this isn’t a short term crisis for these firms, my fear is that when the old stuff does peter out, it’ll be far too late for many advisors (and providers) to make the changes they need to make to survive.

I don’t believe this is a conscious decision by many advisory firms not to make the right investments, it’s more they simply do not know how to find the right talent and leadership to make it happen for them. Many know the change is coming, but simply are in denial that they can force through the internal investments that they need to make. And many still have senior executives whose careers got stuck in a 1990’s timewarp, and simply haven’t evolved their own knowledge, skills and experience. It’s like going to a dentist and not being able to see a digital X-ray of your teeth… would you keep buying services from someone who hasn’t read a text book, or had some form of new skill development over the last couple of decades?

If I was a betting man, I’d predict a very different landscape of advisors competing for market leadership in a couple of years at the current rate of legacy-ness and Un-as-a-Service-ness we’re experiencing today.

The world of enterprise mobility continues to unravel at a breathless clip, with a host of application, infrastructure and niche specialist service providers claiming to deliver (much) more than a bunch of Blackberries, mobile servers and basic help-desk support to enterprise clients.

Enterprise mobility has quickly propelled into the corporate mainstream, with almost every consumer-facing, employee-engaging, supply-chain-enabling process requiring critical mobility interfaces and integration points to avoid becoming obsolete. And with so many processes now going completely native to the mobile world, from membership programs for healthcare insurance schemes, through to governance productivity tools, through to tax management applications etc., the mobility prowess, from a business transformation aspect, is the Holy Grail the winning service providers are seeking to stay ahead of this fast-commoditizing digital marketplace.

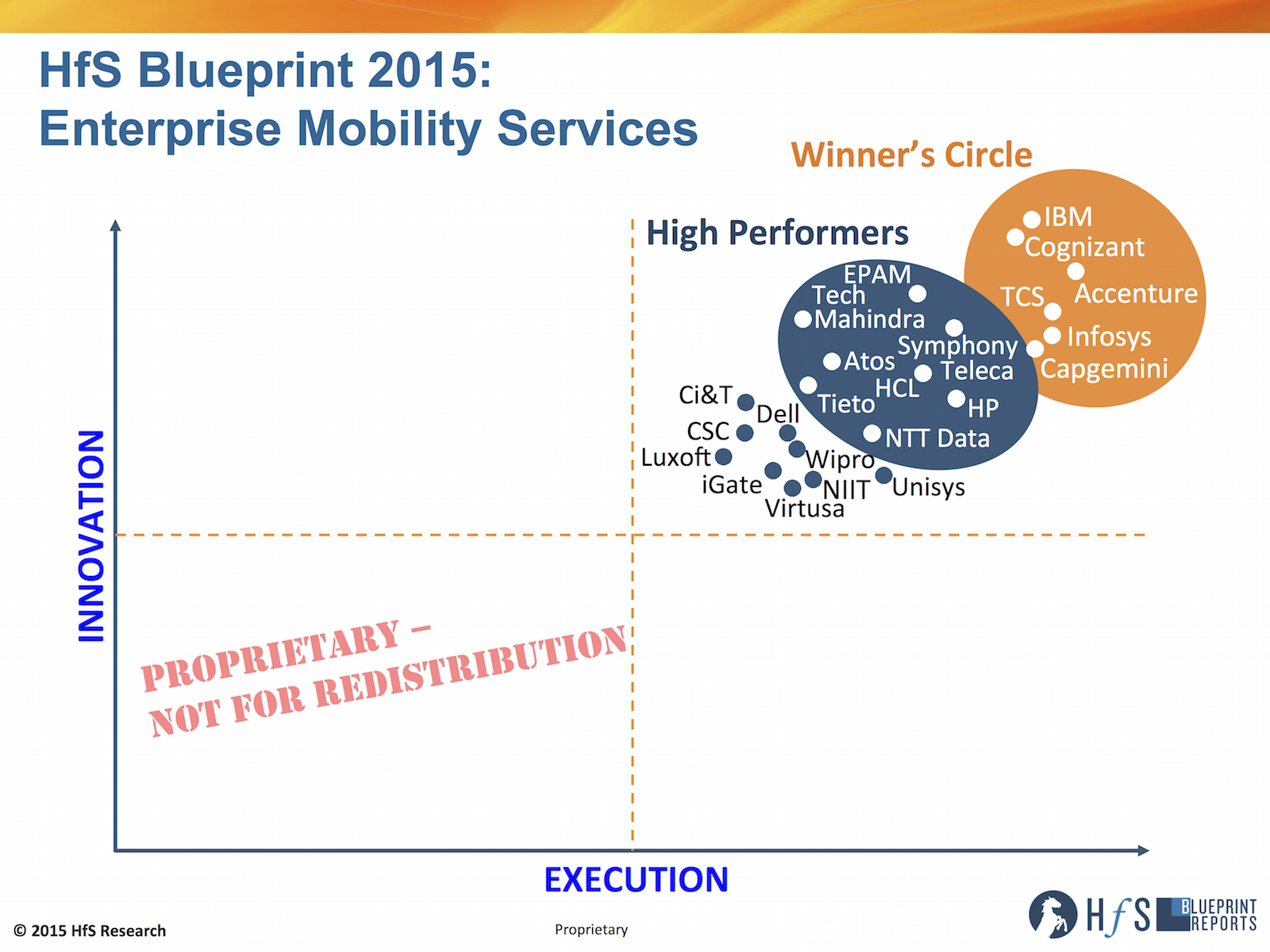

So, without further ado, let’s focus on how the 2015 enterprise mobility services environment is shaping up with HfS’ digital research guru, Ned May’s, new release of the 2015 Enterprise Mobility Blueprint:

Click to Enlarge

Hi Ned, what has changed in the enterprise services mobility market over the last year?

I am pretty amazed at how fast the market has shifted. In the year that’s passed since my last Blueprint, we now see a majority of enterprises undertaking efforts to integrate their mobility portfolios deeper into legacy systems. Few enterprises were at that stage a year ago when it was the build out of point solutions that dominated the activity sourced from service providers in mobility. Even just a year ago, efforts to integrate these apps were largely aspirational but now it is a major area of effort between service providers and enterprise clients.

This increase in market demand for more sophisticated solutions translated into impressive results for some leading service providers. For example, IBM’s mobility revenues grew over 300% in 2014 to reach $2 billion. That makes Mobility a significant contributor to IBM’s services revenue. In short, the opportunity has arrived and I expect the current level of activity around mobility to continue. “Digital” may have become the de facto term service providers use to describe their practices around enabling technologies but when you peel this activity back a layer you quickly find the bulk of activity has a significant mobile component. Whether an enterprise is looking to drive increased efficiency across a current processes, open up new customer channels, or developing a new business model, more often than not today it involves some type of mobile device.

And how did the Blueprint analysis turn out?

The big surprise this year was how well the largest service providers faired. In a rapidly shifting market you might expect smaller and perhaps nimbler service providers to excel but what we saw was the largest service providers fared the best. Topping this off was the success of IBM which I already mentioned grew over 300% in 2014 and that is off a base of $650 million in revenue the year before. That grow would be impossible off the back of new Apps alone. It is a result of the big push from clients for deeper enterprise integration.

At the same time, we saw a second tier of service providers emerge in an area of what I’d call focused scale. These were all large enough to drive efficiency across their delivery models while addressing the myriad of related technologies but not necessarily in the same breadth of industry or end-to-end fashion as the largest service providers. Arguably, these second tier service providers are in great positions position for 2015 as the maturing market looks for further specialization.

So what are your key takeaways from this study and what should we be watching for in the next few years?

One of the most significant takeaways our analysis yielded was a realization that the relative positioning of service providers has become greatly compressed. Every service provider analyzed offers significant capabilities across our criteria for both execution and innovation.

Our Winner’s Circle of Service Providers included: Accenture, Capgemini, Cognizant, IBM, Infosys and TCS. Our High Performers were: Atos, EPAM, HCL, HP, NTT Data, Symphony Teleca, Tech Mahindra and Tieto.

Yet, the differences are getting more difficult to discern and that makes for a buyer’s market at least for the next year or so while integration remains king. We expect this to change in 2016 as a few service providers begin to demonstrate the unique advantages they gained by extending their definition of mobility to include the Internet of Things. Until this occurs the market will be led by those service providers who can drive the greatest efficiency around areas like running App Factories, providing Testing-as-a-Service and embedding security across every interface.

Ned May, SVP Digital Transformation and Mobility Services Research

Another takeaway is that we don’t expect to see a great deal of commercial demand for mobility-led transformation in 2015. When enterprises tapped their IT departments to rationalize the disparate mobile efforts underway, they inadvertently put the brakes on innovation. IT organizations are notoriously conservative and as they work to integrate the mess, they are reluctant to let go of any recently reclaimed control. This means we don’t expect to see significant activity around transformation just yet and that could be a lost opportunity as enterprises spend perhaps too much energy on neatly tying together loose ends rather than embracing these new mobile technologies as a way to drive fundamental change. The only caveat here would be for those enterprises that have a strong Chief Digital Officer in place. Where this type of leader exists we expect to see some healthy conflict between running processes more smoothly and running processes in new ways. But again, the bulk of activity in 2015 will be around developing apps more efficiently and integrating them into existing systems.

HfS readers can click here to view highlights of all our 22 HfS Blueprint reports.

HfS subscribers click here to access the new HfS Blueprint Report, “HfS Blueprint Report 2015: Enterprise Mobility Services“

We’re proud to announce our role as exclusive research and content development partner for NASSCOM’s Business Process Management Summit 2015, to be held in Bangalore, on September 24th-25th.

We’ve been closely working with NASSCOM in designing this year’s theme: “The Emerging Digital Economy: Thrive, Survive or Die”, developing session topics, identifying speakers, supporting content for key speeches and producing a definitive white paper on the Digital theme, in addition to supporting the marketing and promotion of the event. This year, I will be hauling myself back to India along with Charles Sutherland to deliver a keynote presentation on the Emerging Digital Economy and its impact on the BPM industry, along with helping organize the other sessions and content themes.

At the NASSCOM BPM summit, participants will debate the emergence of digitally empowered business process services in horizontal areas such as finance, procurement, supply chain and HR, in addition to industry domain specialties, such as financial services, healthcare, life sciences, retail and manufacturing.

Key Digital Themes being discussed at the 2015 NASSCOM BPM Strategy Summit 2015:

Embracing Design Thinking: Generating creative solutions by understanding the business context

Smartly Automating: Blending of automation, analytics, and talent

Intelligently Managing Data: Applying analytics models and techniques to achieve meaningful business insights

Writing-off Legacy: Use of platform-based services to make many tech investments redundant

Being Brokers of capability: Governance staff managing towards business-driven outcomes

Entrepreneurial Intelligent Engagements: Striving for relationships based on expertise, gain-sharing and outcomes

For members of the HfS global knowledge community interested in speaking at the summit, please email [email protected] .

I recall back in late 2010 when an eager young research firm practiced what it preached and scoured talented resources on the Indian subcontinent to support our research reports. One such resource was a bright young woman called Reetika Joshi, who worked with us to produce the industry’s first ever assessment on “Offshore Analytics Providers.”

Fast-forward four years and said analyst has now survived her first Boston winter (she did nearly perish) to produce a fine assessment on where today’s far more sophisticated analytics services market is today headed:

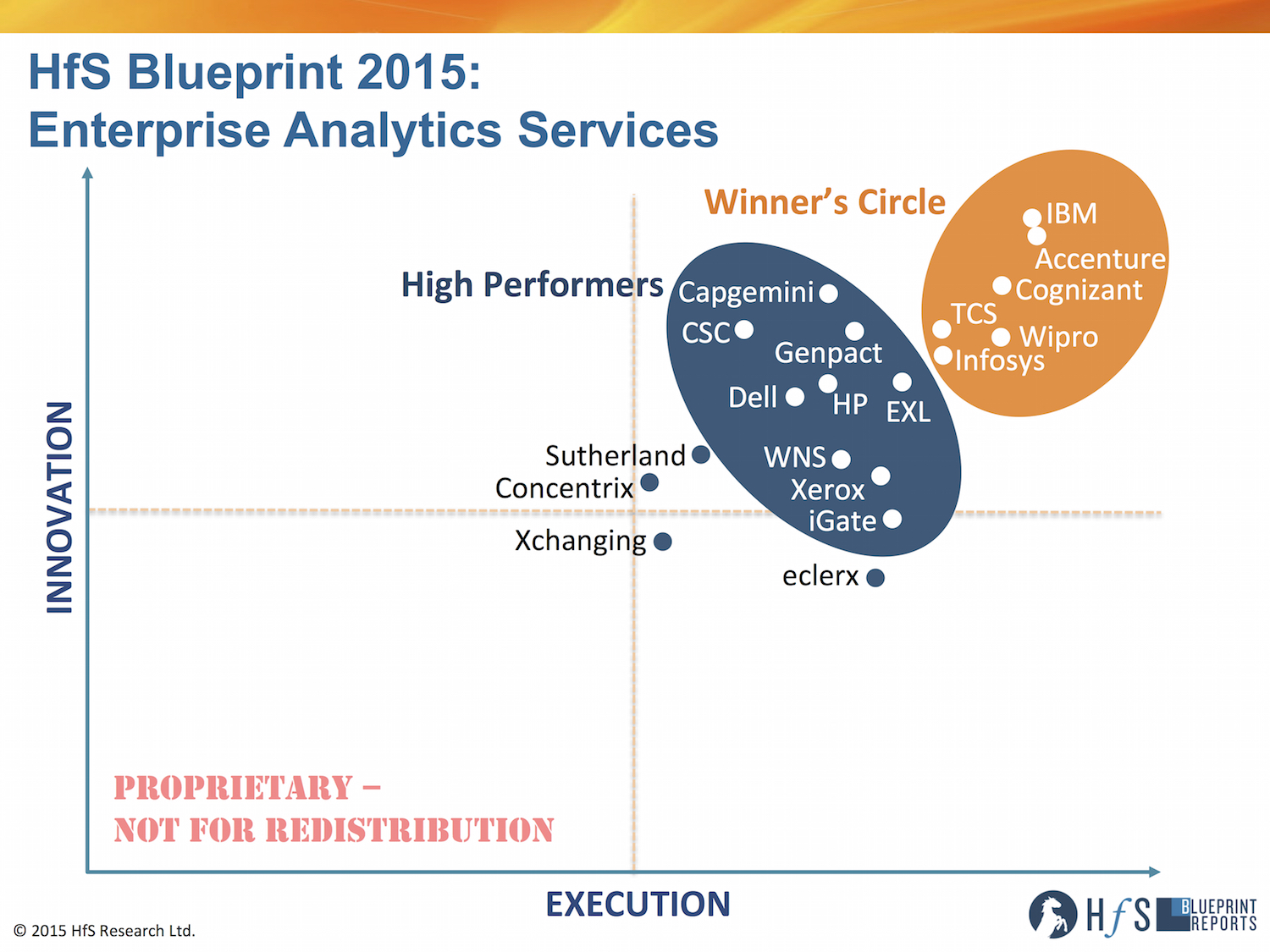

Click to Enlarge

Hi Reetika, how do you see the enterprise analytics services market evolving?

The 2015 HfS Enterprise Analytics Services Blueprint Report is a refresh on our initial assessment in November 2013. Compared to 2013, the market is seeing an overwhelming change – an increased focus on applying business context and doing more meaningful analysis, rather than the isolated procurement of analytics tools and technologies. This is impacting the stakeholder dynamic, the decision-making process and day-to-day relationships with service providers for services buyers. It also spells great news for service providers with analytics consulting backgrounds and/or domain expertise for analytics managed services, as services buyers perceive greater confidence in working with these service providers for strategic analytics initiatives that are highly visible in the enterprise. This also means that analytics service providers are having to change their pitches to become less technical (for a non-IT audience) and offer services and solutions that solve specific business challenges. For most service providers, big data and analytics services are the fastest growing businesses in their portfolios. Analytics has been a key area of investment to move up the value chain and provide higher value services for service providers across the market.

In terms of demand, we see managed services grow significantly, while analytics project work remains strong. Services buyers are gradually expanding the amount of ongoing decision support services they do with service providers, beyond short term project based work and routine reporting or data cleaning and consolidation. This is due to growing adoption of data-driven decision making within different parts of the enterprise and the need for more analytical support than internal staff can support. Analytics projects are as prevalent as ever, especially with advancements in big data applicability within specific industry verticals and functions giving rise to new opportunities.

And how did the Blueprint analysis turn out?

Phil, as you know, this year’s Blueprint, based on our updated crowdsourced methodology, has increased the focus on Innovation in analytics service delivery, with 47% of the Blueprint scoring being tied to proven innovation capability and performance for these engagements, beyond the standardized processes in reporting and data management. Overall, we see a shrinking divide between the different categories of enterprise analytics service providers. While this vision hasn’t fully been realized, service providers over the last couple years have invested heavily in developing capabilities across the analytics value chain. Whether they started from traditional strengths in information management, consulting, BI reporting or ongoing research support, they are as aggressive in playing for a piece of the high-value advanced analytics pie with emerging technology expertise. The proof of this pie is in the eating – you can see how placement of service providers across the Blueprint grid is more condensed than in 2013 with high levels of innovation coming from various service providers from a mix of analytics backgrounds.

Winner’s Circle features four mainstays and two new entrants. Accenture, IBM, Infosys and Wipro continue to hold onto their market lead based on solid execution of analytics services and delivering on innovation capabilities that are visible to clients. Cognizant entered this group based on its strong connect with clients – account management, playing in its industry specialist niches for advanced analytics and integrating and modernizing its existing information management business. TCS advanced for a focus on developing industry specific solutions.

Intense competition among the next hopefuls. HfS sees strong competition to the Winner’s Circle coming from Capgemini, Genpact, and EXL amongst others. The gap is becoming much smaller for this next rung of service providers that are investing aggressively to win in a rapidly changing market that is rewarding success across the analytics value chain.

So what are your key takeaways from this study and what should we be watching for in the next few years?

Overall, we believe that the analytics services market is still opportunistic. Service providers are creating more rounded-out offerings by industry verticals and investing with clients to gain more domain expertise in new, emerging areas. Clients, increasingly from business and not IT, are steadily scaling their investments using multiple engagements models depending on their unique business environments and organizational culture. We see an across the board willingness by both services buyers and service providers to experiment in different kinds of pilots and POCs that go into the next level of analytics use case development – not just applying cross-vertical learnings (from retail banking to healthcare), but in conjunction with newer sources of data (e.g. sensors, geolocation mobile data), and new uses of other emerging technologies (e.g. cloud based data warehousing, mobile delivery of reports and insights). Of note, service providers in a bid to develop robust solutions to take to market are funding a significant portion of these initiatives. So expect to see more modernized vertical and functional analytics solutions in the next few years, and a lot more co-innovation coming from service providers partnering with clients and channel partners.

Clients will continue to use a wide mix of internal and external talent and technology for different analytics implementations, with no clear model emerging. For some, carving out standardized and repeatable reporting and analysis tasks for third party providers while honing internal talent to do advanced analytics seems to be the answer. Others are collaborating with service providers for technology decisions and implementations more than ongoing analytics support. Others still are critically reliant on the industry-leading insights generated by their service providers’ staffs that are almost seamlessly blended alongside internal teams.

Increased deployments of big data programs. A lot more clients are willing to make investments in big data platforms and the analytics and reporting services wrapped around them, through careful piloting and experimentation over the last two years. Service providers finally have a growing roster of large-scale client implementations for big data programs, though some are focused in specific functions/industry verticals. We see a significantly higher number of big data platform implementations, along with the surrounding descriptive and predictive analytics layers, reporting dashboards, ongoing decision support and big data consulting capabilities.

Growing aspiration to become an end-to-end analytics partner to clients. Service providers are offering more ‘integrated’ analytics solutions that cut across the analytics value chain (ETL, data prepping and integration, model development, etc.). Instead of focusing on selling these components, providers are promising to integrate them and deliver to business outcomes. However, services buyers in our study were quick to point out relative strengths and weaknesses of the majority of service providers for areas like information management, BI reporting and advanced analytics – both from a capability and perception standpoint. Thus service providers over the next few years will spend much time in a) rebranding their market perception on their ability to service the entire big data and analytics stack and b) integrating and expanding on relatively weak areas. This means more acquisitions to fill gaps, and massive investments in internal capability development. Budgets are now coming from multiple business functions and the potential for growth is huge if the service provider is the first to be established as the company’s enterprise-wide analytics partner – not just for data integration, BI or analytics projects, but essentially a COE to draw various capabilities across this value chain. There are a few examples of where market leaders are experimenting with buyers on this model. Success will be determined by how far the service provider is able to penetrate into the client organization’s functions and processes and impact day to day decision making.

Reetika Joshi is HfS Research Director, Consumer-centric Operations and Analytics Strategies (click for bio)

In summary, the market for enterprise analytics services remains dynamic and evolving and we see potential for significant change to come in 2015 as emerging service providers increase their investments and focus on this offering. We will continue to cover this market throughout 2015 in our HfS soundbites and POVs and expect to see even more improvement in the innovation and execution metrics of all service providers between now and our next Blueprint for this market.

HfS readers can click here to view highlights of all our 21 HfS Blueprint reports.

HfS subscribers click here to access the new HfS Blueprint Report, “HfS Blueprint Report 2015: Enterprise Analytics Services“

After our dramatic fake announcement that we had entered the sourcing advisory business on 1st April, our phones have been ringing off the hook from service providers desperate to get included in our deal pipeline (no joke).

While, in hindsight, HfS& would likely have been a roaring success disrupting the legacy sourcing advisory business, we fundamentally have no desire to be an advisor shop. Sorry. Back to the research grindstone…

And for all of you who sent congratulatory notes, please do read beyond the first paragraph next time we announce something. Especially on April 1st =)

HfS Research, the leading analyst firm covering outsourcing strategies, today launched HfS Advisory (abbreviated to “HfS&”) and announced its exit from the research analyst business. The firm, once lauded for disrupting the research industry by giving its research away for free, finally conceded there is actually no money to me made from a business model where there the core product does not have an associated price tag.

As part of its relaunch as HfS&, the firm announced the following new advisory service lines, designed to disrupt today’s outsourcing advisory marketplace:

1) FTE-Lite . HfS& will disrupt the traditional outsourcing transaction marketplace by offering a series of unique advisory services designed to broker the lowest-priced FTE-based outsourcing deals for enterprise clients. HfS has contracted with a SWAT team of professional negotiators whose fees are paid by the winning service provider, allowing HfS to undercut other advisors by up to 75% on advisor fees.

2) Business Outcomes Definition Creation. HfS& has also recognized a dire need in the sourcing industry to help clients define business outcomes, so that they can be executed on, and ultimately achieved. HfS& intends to use the latest techniques in Design Thinking to make this all happen.

3) Digital Transformation On-demand. HfS& is also getting ahead of the curve with digital transformation, by offering leading edge digital transformation expertise to clients – again at much lower fees to clients as the providers will pay HfS& directly to get invited to the shortlist.

Charles “Hank” Sutherland, preparing to take the reins at HfS&, is spotted trading in his Prius for an F250

4) Robotic Process Automation Starter Kit. HfS& will also move the disruptive advisory needle by offering up real, transformative solutions to help early phase clients take their first baby steps into robotic process automation in one, complete, off-the-shelf do-it-yourself RPA toolkit. Like other advisors, HfS& has actually no clue what it is doing in RPA, but acknowledges it needs to have some semblance of a practice to appear relevant in the market.

As of today, HfS& will no longer produce research and be a fully-fledged outsourcing advisor, and has even made the steps to relocate its headquarters to Dallas, Texas under the watchful eye of Charles “Hank” Sutherland, who today was spotted trading in his Toyota Prius for an Ford F250, equipped with gun rack and complimentary enrollment to the NRA FIRST Steps Shotgun Orientation course.

Commenting on the strategic move, HfS& CEO, Phil Fersht added, “We were getting increasingly fed up giving away all our research for free and getting little appreciation for it from industry. While we did a great job putting our competitors out of business, we found it hard to develop any for ourselves either. So all we really achieved was putting the whole research business out of business. Hopefully, now, we can still glean a few bucks feeding off the stagnant remains of the legacy outsourcing advisory market before that also winds up on the scrap heap of putrid old-world business models.”

Photos of Mr Fersht and Mr Sutherland will be available once you register here.

And of course… this was an:

Please, please don’t tell me you fell for this again! (Even though the business model might kinda work…)

And while we’re reminiscing about falling for April Fools’ gags, here is 2014’s classic:

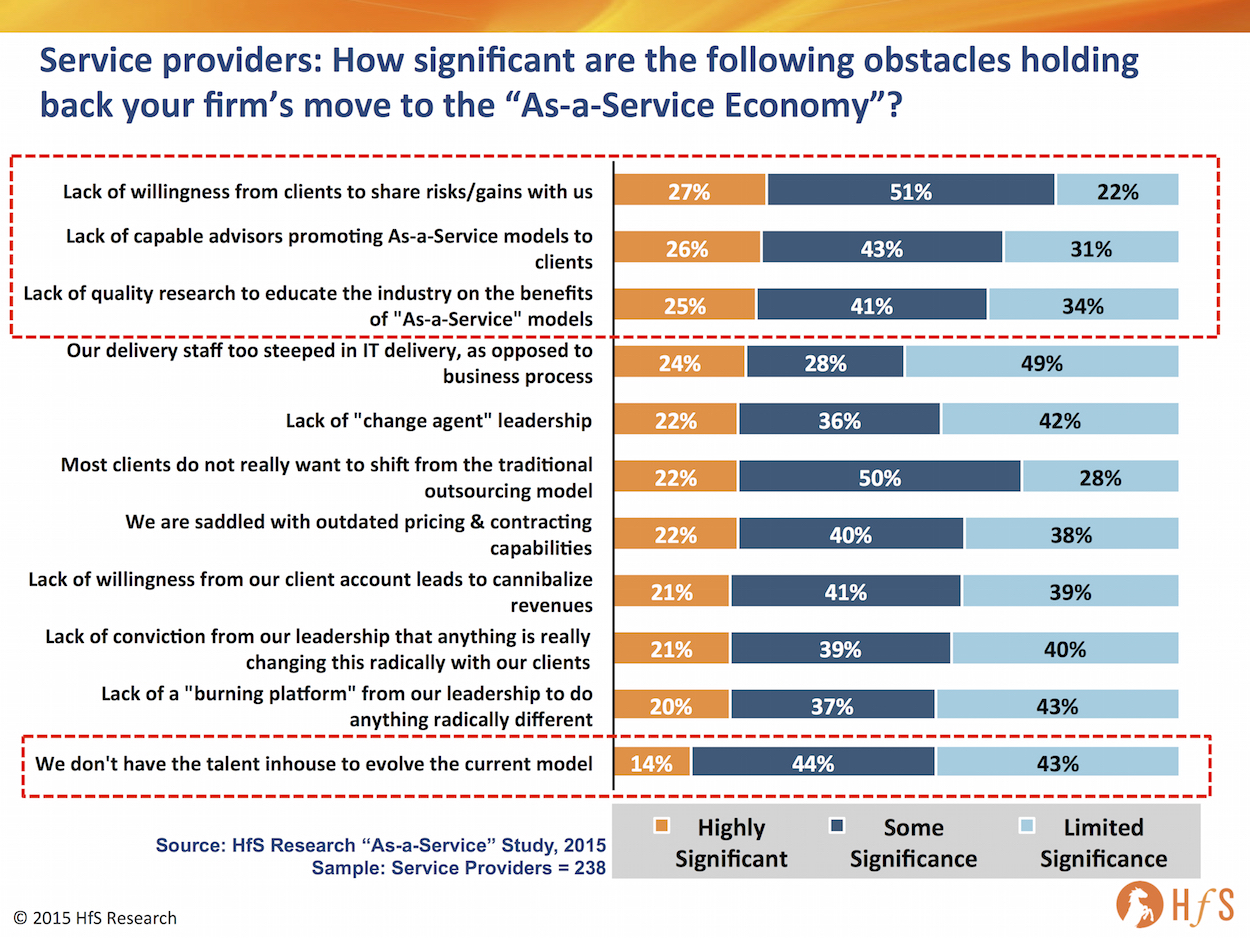

We couldn’t resist sharing a quick snippet from our new “Eight Ideas of the As-a-Service Economy” study that reveals some rather alarming news: service providers are blaming everyone bar themselves for obstructing their progress towards As-a-Service.

Click to Enlarge

At fault number 1 – the Clients. Top of the lists are their clients themselves, with 78% of service provider executives (from a pool of 238) citing their unwillingness to venture into risk/gainshare models with them. Considering most enterprise clients we talk to complain that their provider refuses to budge from their predictable, profitable FTE delivery model, baffles me here.

At fault number 2 – the Advisors. Next up are sourcing advisors – those lovely folk who bring them to the table and horsetrade to get deals done. Apparently, they are not selling the evolving model to enterprise clients and are just not very capable. We are starting to see more As-a-Service traits in some mid-tier deals, where there is less wiggle-room to make huge profits on wage arbitrage, and these frequently are too small to warrant several hundred grand being spent on an advisor. The advisor model is still built for the old world of big scale deals, not the new world where analytical and creative skills, technology enablement and automation are the watchwords.

At fault number 3 – the Analysts. And third on the list appears to be a pot shot at analysts, where providers claim a “Lack of quality research to educate the industry on the benefits of As-a-Service models”. We apologise and promise to write more coherently… and this time make sure you read it, Mr and Mrs provider executive, because we know how much time you spend trawling your way through analyst reports these days….

Least at fault – the Providers themselves. And very last on the list (no sh*t) is the fact that they are struggling with their own inhouse talent to shift the model to As-a-Service. Well that’s great news, as I thought it might be a bit of a struggle for providers to retrain their developers and project managers to think analytically, help clients with design thinking, laying out an automation roadmap etc. Now we can all rest easy with the knowledge that the providers will save the day, while the rest of us clients, advisors and analysts can all go away and die somewhere on the scrap heap of legacy labor models, SLAs and dull irrelevant research.

Bottom-line: We’re all pretty much at fault for perpetuating the old models. This is a collective learning effort across all stakeholders to adopt the ideals of As-a-Service

As we reach the end of the runway with the legacy model (which still has a way to go for many enterprises) there needs to be a much better effort collectively to discuss the actual measures enterprises need to adopt to take better advantage of the technology enablers and hone our skills accordingly. Many advisors are clearly still making a good living advising on the old model, otherwise many would cease to exist, while analysts clearly do a poor educating the market on real world examples of how to make the shift (and persist on an old world model themselves to engage with clients). Meanwhile, if service providers are as good as they think they are, they need to find better ways to convince their clients to trust them more, to work with the on joint projects of discovery etc. Lee rhetoric, more dialog among the key stakeholders and better real-world education is the only real formula for success here.

One growing talent issue I have increasingly become concerned about, is observing people whose career development quickly nosedives when they isolate themselves in a work-at-home model.

I personally believe being able to work effectively within a virtual environment warrants a completely different skillset and attitude, if you want to advance your career and keep developing your potential.

So here’s my guide to being an effective virtual worker in six easy steps:

1. Use voice and video as much as you can. Staring into a computer relentlessly typing emails for 16 hours a day with little voice contact with your clients/co-workers makes anyone miserable – and anti-social over time. Make considerable effort to talk to people as much as you can. Use video for conference calls too – it forces everyone to pay attention (and get dressed) and have a much more personal series of dialogs.

2. Sort out your voice technology. There’s nothing worse than communicating with people who have a crappy wifi connection, with whom you can never get a clear skype/google conversation without the echos, constant disconnections etc. If your wifi’s garbage, you can get great quality Skype (for example) over 4g LTE these days on your iPad or iPhone. Oh, and while we’re at it, stop slurping coffee and eating into your microphone on calls, it’s disgusting…

3. Stop using email for every bloody communication. Email is a tool for passing along information and instructions. Learn how to be cordial, get your message across and use voice as much as possible to communicate. Never use email for heated conversations that have emotion (especially negative emotion).

4. Buy an exercise machine and work out everyday. Without fail. You’re sitting on your bum most the day burning zero calories and likely visiting the fridge on an hourly basis. You have to exercise, or you will balloon and die. Buy yourself an elliptical trainer, exercise bike or treadmill, use it everyday, and after a while you’ll get so fit you can even take calls while you get even fitter. I would recommend going to a gym, but who has two hours to carve out when you’re an overworked virtual nutcase glued to your machine all day and night?

5. Invest more time getting out to see your clients, your peers and do more networking. When you see noone bar your family, pets and the plumber on a daily basis, the only way to stay motivated and continue to develop yourself is to go to more conferences, make more effort to visit your clients / peers etc. You learn the most from your collective discussions with others, from having discreet conversations. Everyone’s fed up with social-media – meeting people and being social is back in vogue. Really – get out of the house!

6. Stop complaining about how stressed and overworked you are. Boohoo – just suck it up, we’re all over-bloody-worked. It’s all in the mind – so get healthy, get social again, start enjoying your work and you’ll forget about stress and go with the flow. Just go with the flow, it’s the only way to survive these days.

There endeth my lesson for the day. Go back to your weekend…

If I told you that only 13% of sourcing advisors have plans to invest in cognitive computing and 15% in Robotic Process Automation skills, you wouldn’t believe me, right?

If I told you that only 13% of sourcing advisors have plans to invest in cognitive computing and 15% in Robotic Process Automation skills, you wouldn’t believe me, right?

We’re proud to

We’re proud to

One growing talent issue I have increasingly become concerned about, is observing people whose career development quickly nosedives when they isolate themselves in a work-at-home model.

One growing talent issue I have increasingly become concerned about, is observing people whose career development quickly nosedives when they isolate themselves in a work-at-home model.