I recently attended a graduation ceremony and was amazed at the number of students engrossed in their phones, occasionally looking up to applaud a graduate.

What’s happening here? Have we created a whole generation of socially-retarded morons preferring to network on Instagram and Snapchat than engage in physical dialog anymore?

Welcome to the entitled job market for the twenty-somethings where BPO doesn’t quite fit in…

What’s even more disturbing is the lackadaisical attitude displayed by so many of them when you ask them about their career plans and ambitions. Most seem pretty happy to sit around at home staring into their phones for a couple more years until their perfect job just happens to turn up on their doorstep. If you haven’t gone down a specific career track such as medicine, law, finance or engineering, the future is an apparent wilderness of vagueness, deluded desires and uncertainty. Doesn’t anyone have a plan to start somewhere and work their way up to a better place in the future? Isn’t that what us mid-career folks did when we were starting out?

So let’s focus on our industry – the one of servicing enterprise IT and business operations effectively. Whether we buy, sell or advise on business operations, if we don’t have succession plans to blood the next generation of talent, we’ll just become an industry of old farts with over-bloated salaries and a culture of preserving the past, not advancement into the future.

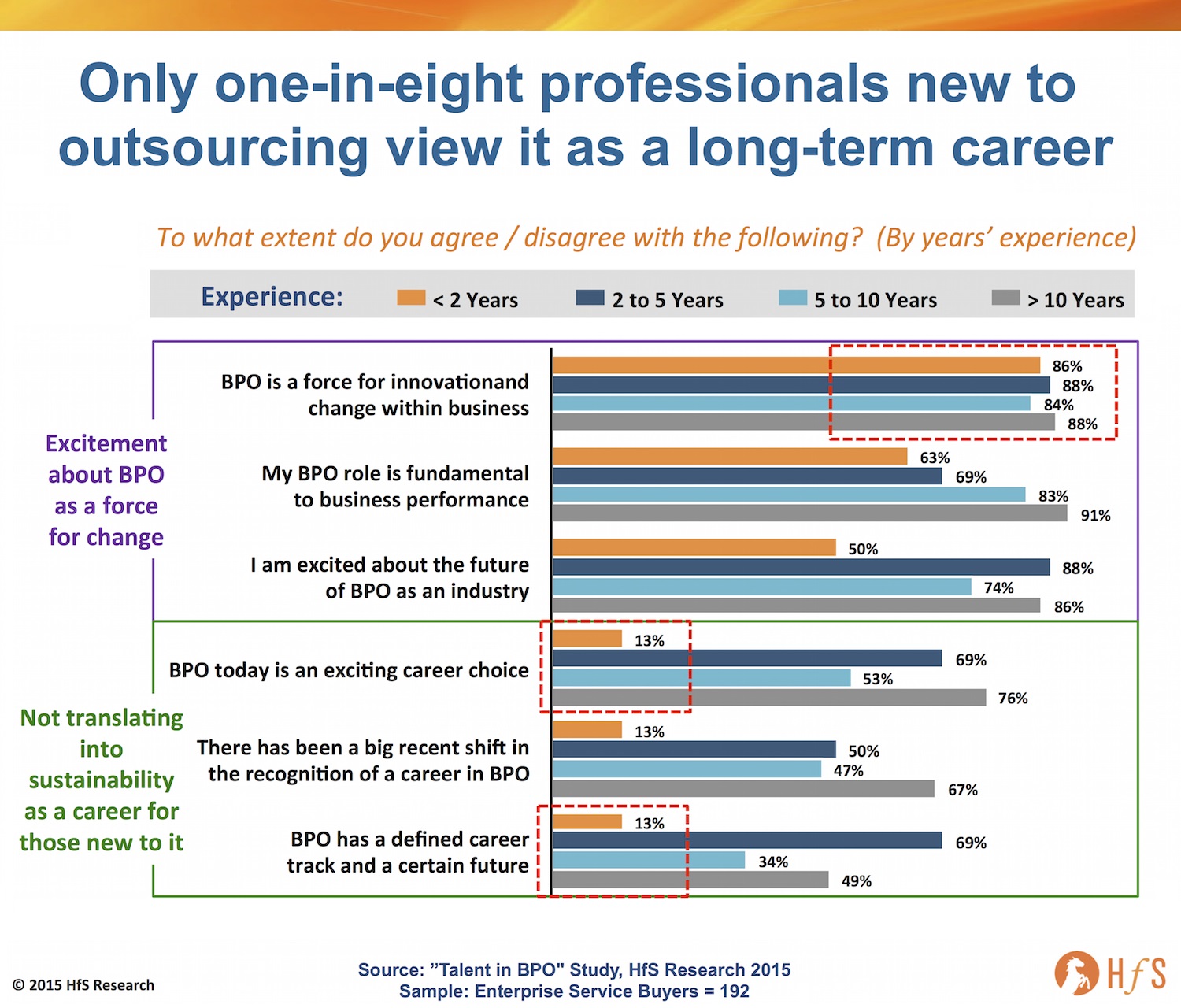

New data from our Talent and Trust in BPO study, where we spoke to 540 business stakeholders on the topic – and you can read the full report here – is pretty damning in this regard, with the vast majority of newbies in BPO seriously struggling to see a career path around BPO practices, despite being impressed with the potential of BPO as a real change agent within their businesses:

Click to Enlarge

In my view, failure to develop a Millennial Strategy will be the ultimate death-knell to a long fruitful future for business and IT services, and we may as well accept the reality that we will become mimicked into a piece of RPA software and erased into the ethernet of digital retirement within the next decade. Our problem isn’t one of setting out challenging work and even creating exciting roles for people, it’s about getting them focused and interested in building a career as a Capability Broker.

Six ideas we can embrace to try and create the next generation of Capability Brokers

There is no quick fix when it comes to creating work ethics and motivating people who are only ever willing to do just enough not to get fired (or even less, but don’t really care), but we can craft a better defined career path and set expectations of what it means to work in the business services industry. Here are some ideas:

1) Establish the Chief Services Officer role. We need transformational leaders to define and drive Capability Broker roles. There are several excellent governance leaders today developing these careers who are helping define the next generation of services professionals. We had some of the at our recent Dallas event. We need to give these people an identifiable role in the organization that inspires others to join their teams. CPO, CHRO roles are too broad and, let’s face it, not exactly inspiring to the younger generation. As Fast Company famously revealed ten years ago now, the bottom 2% of MBAs end up in HR, and I dread to think the number that wind up on procurement. We need a services leader who sits over the operations of a business to ensure the right partnerships are being brokered and the right careers are being developed internally to take maximum advantage from them.

2) Promote the career path of the Capability Broker. Today’s service practitioner is increasingly becoming less about having specific skills wrapped up in a nice bow, such as “ABAP programmer”, or “Vendor Contract Manager”; it’s now about being a Broker of Capability – people who can multitask across multiple disciplines and find business problems, in addition to solving them, who can work with multiple delivery vehicles or partners, such as service providers, SaaS platforms, crowdsourcing firms, shared services COEs etc. And these brokers must operate as real integration points of capability, not simply procurement administrators that negotiate rates and manage contracts. This sounds much like an exciting career path that incorporates genuine resourcefulness, ingenuity, consultative acumen and ability to think out-of-the box in order to achieve real outcomes for an enterprise. So let’s start promoting these roles as such… they’re exciting and require smart people to grow into the roles, where there is no defined curriculum and need an ability to handle ambiguity and go with the flow.

3) Orient towards Design Thinking over Six Sigma. Six Sigma, Lean and process excellence saved the BPO industry over the last decade from the unprofitable excesses of the early days of off-shoring – and gave service providers a frosting of process excellence by which to brand their offshore-dominant strategies. However, we at HfS believe that these are no longer the most suitable approaches by which to improve business processes. Six Sigma is about eliminating waste and solving imperfections in processes. Instead, we believe that, as a market, we need to lead our process improvement efforts with a starting point based in Design Thinking, which is about finding problems, not just solving them. We need to see the desired outcomes from clients and, in turn, their customers, as the lens by which to look at processes rather than the process itself. All too often, we have “optimized” processes for cost, based on a very inward looking view of the business process, which either keeps the view of the external connections of the process static, or just ignores those considerations outright. In the As-a-Service economy, it is flexibility in process design and delivery which will win out, and starting with a Design Thinking approach (after training and converting many of the existing process excellence teams) will be the best model for future success.

4) Ensure outsourcing contracts have real actionable measures to develop Capability Brokers across the buyer/provider relationship. Moving beyond the “lights on” tedium of an operations contract has to become paramount in all new contract negotiations. When you listen to experienced governance executives today, many are proudly talking about how they are emphasizing the joint workshop sessions, the bonuses for achieving innovations and improvements, the incentives for achieving productivity enhancements beyond merely moving work offshore. It’s not easy to contract for innovation, but many firms are now trying – and finding some success.

5) Ban personal smartphones from being used during the office hours. It’s just got to be done. It’s the disease terrorizing today’s business environment – too many people just cannot focus on their jobs anymore because they are completely distracted by the sheer volume of social media impacting their lives. Seriously, I know hundreds of people (and not just Millennials) who cannot concentrate on one single work task for more than five minutes at a time (and you do too…. you just know it). Force them to focus – you’ll be doing them a huge favor… the best performing shared service centers do it, so why not follow their example?

6) Focus on locations where young people still appreciate a service career and have some company loyalty. When you visit smaller cities, there is often still the culture of people going to an office and staying with one company for several years to develop a career with it. They appreciate a job with some security tied to it and have less grandiose career ambitions. In most big Western cities, today, the cost of living is far too high to justify a modestly paid job. Someone was trying to convince me the other day that a family of four in Massachussetts needed a household income of $300K a year just to live reasonably well. Sounds a bit excessive, but they are probably not too far off. Clearly services jobs starting at $25k a year are not going to be very appealing to people wanting to raise a family on the expensive Eastern seaboard of the US (and let’s not even get started on California).

The Bottom-line: There is no quick fix, but we need to get ahead of this now

I dread to think what could happen if we hit another economic downturn (if HSBC’s recent viewpoint is correct) with today’s working attitudes of the younger generation. There will be millions of unemployed youths angry that the living they felt entitled to never transpired. We can’t simply send them to work with a kick up the behind, but we can try to create a career path with a mission, a purpose and strong leadership that inspires the next generation. That’s probably the best we can do for now, so let’s start doing it!

Moving at Warp Speed into the As-a-Service Economy?

Thanks to all of you who spent a fabulous day with us in Dallas for our first HfS Working Summit, dedicated purely to a joint unravelling of how we can find a way to the As-a-Service Economy.

What struck me was how quickly our industry has genuinely become focused on achieving business outcomes over the past few months – and this is being weaved into many of today’s new contracts and governance performance metrics. The conversation has moved along quite markedly and I view this is a major leap forward for many industry stakeholders to change the way we manage service delivery that isn’t purely based on valueless metrics and squeezing out those last remnants of bloated labor cost.

However, it’s also clear that ambitious enterprise leadership teams are growing increasingly frustrated with their teams’ struggles to progress their capabilities, which will be the ultimate burning platform for many enterprises to make the shift and write off their legacy back office. Here cometh the As-a-Service Economy, where stagnation and legacy will no longer be tolerated…

So what are we learning, at HfS, about the current readiness of enterprises to outsource and leverage As-a-Service delivery?

In short, we’re on a train hurtling towards something resembling “As-a-Service” and we need to make sure we stay on it:

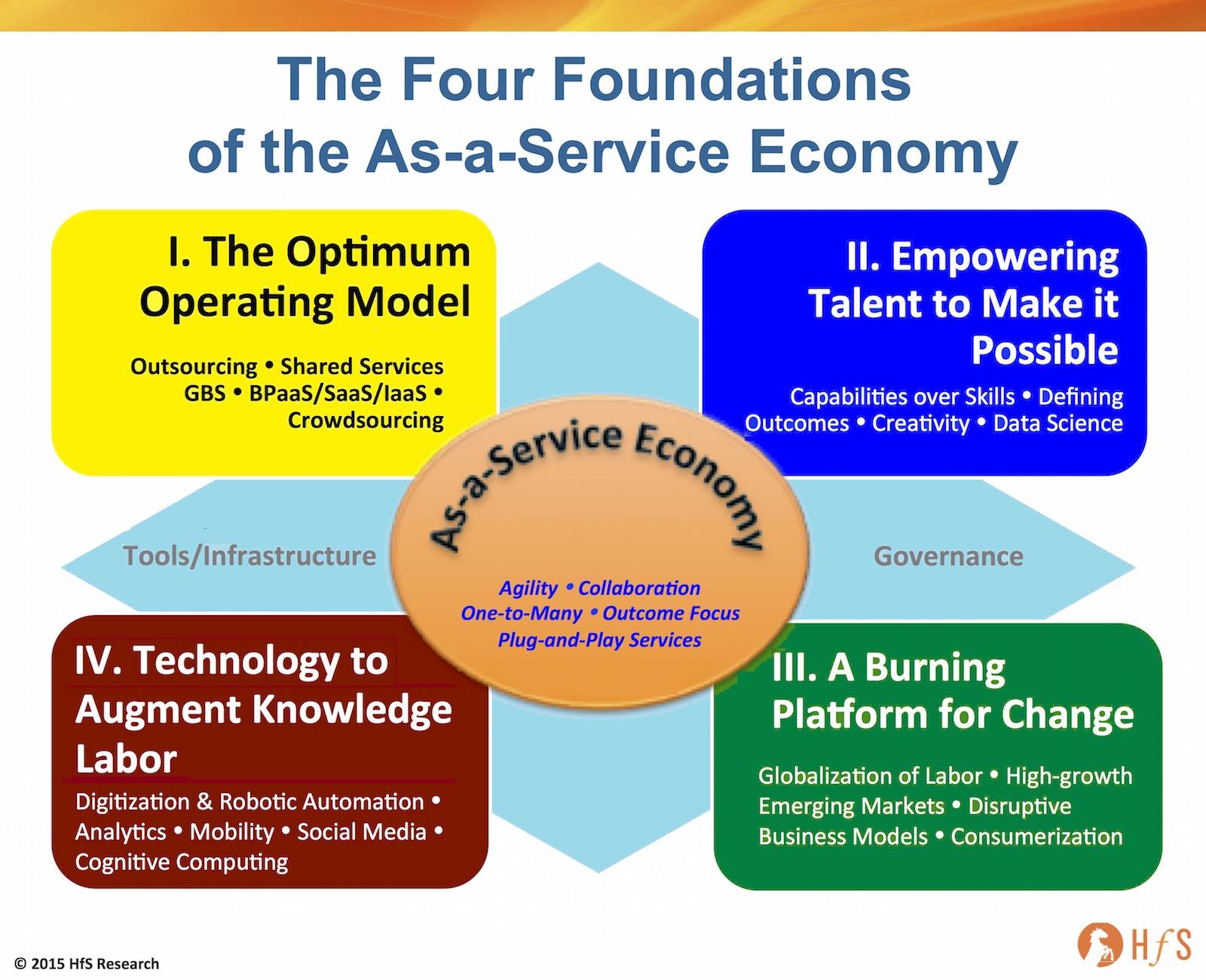

At HfS, we are baking this unraveling of As-a-Service delivery into four distinct foundations:

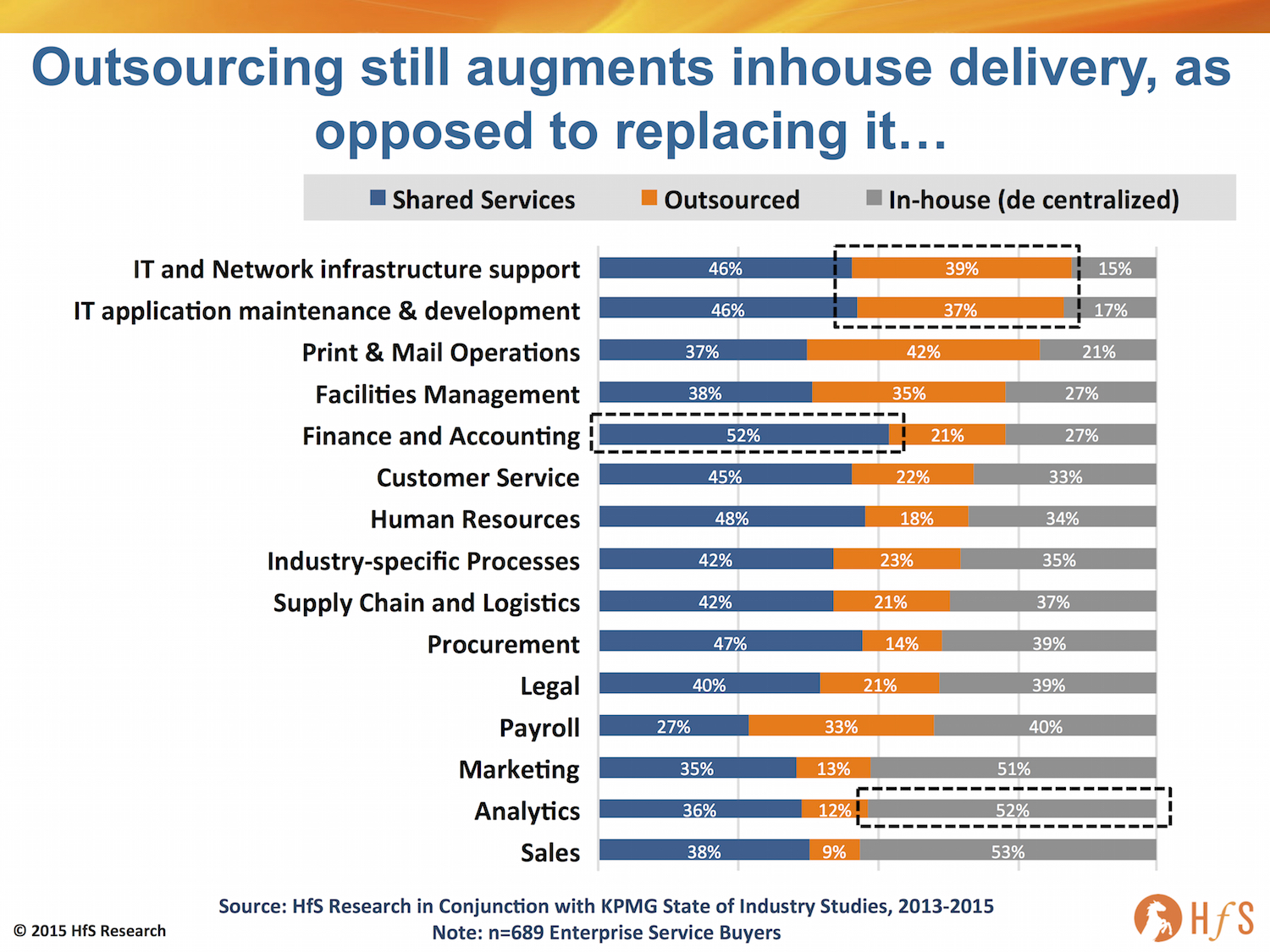

Foundation I. The Optimum Operating Model: Outsourcing not exploited nearly enough by ambitious enterprises

Today, most buyers are still using outsourcing as an augmentation vehicle for most of their processes – filling occasional delivery gaps, but more as a vehicle to drive scale and cost efficiency:

Click to Enlarge

Our new research shows only a third of buyers today view outsourcing providers as a real strategic partner, while half see them as efficiency vehicles for themselves. However, it’s becoming abundantly clear that the desire to shift towards As-a-Service delivery is much stronger at the senior levels, and we believe many enterprises will turn to their service providers more aggressively over time as they simply lack the skills and capabilities inhouse to get them past the traditional service delivery model.

What’s clear in the chart above, which illustrates a view from our recent industry studies with KPMG on how enterprises run their business operations models, is that outsourcing is still predominantly an augmentation vehicle to support business processes, as opposed to the end-to-end delivery of business functions themselves. For instance, less than 40% if enterprise IT s outsourced, 20% of finance and accounting – and only (amazingly) a third of payroll.

When we look at real value-add areas, such as analytics, where As-a-Service focused providers can really help clients, we can see that over half of analytics work is still conducted in decentralized models, with only 12% currently being serviced externally.

Foundation II. Empowering Talent: The Focus shifts from Skills to Capabilities, from solving business problems to finding them

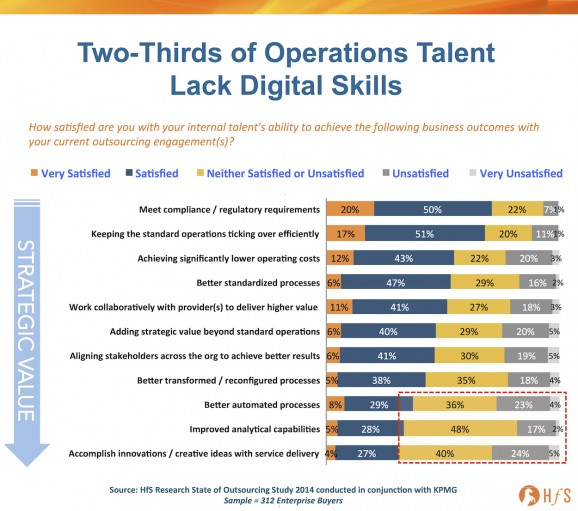

The biggest issue impacting buyers, service providers and advisors in the industry today is the challenge of broadening, not only skillsets of delivery staff and leadership, but changing their mindsets and capabilities.

Our State of Outsourcing study clearly reveals two-thirds of operations jobs are now under threat if staff fail to reorient their capabilities. Simply put, barely a third of enterprises, today, are actually happy with their internal talent’s ability to drive positive outcomes from their analytical and creative capabilities, with their current outsourcing engagements:

Click to Enlarge

This is nothing new; organizations have been trying to reduce their labor costs for centuries, but something feels very different about the emerging digital reality in which we operate. Many of us believed the onset of web technologies would be the big game changer with how we utilized labor, but it actually increased our reliance of humans – many business processes became web-enabled, which necessitated training on new applications and helped us work more effectively – but they didn’t fundamentally change how we operated. The web really just enabled us to run things the same way as previously, except with more global capabilities and much more effective communication and collaboration.

It was this earlier wave of digital evolution which really enabled the great outsourcing boom of the last 15 years, as communication costs plummeted and web applications made it possible to work with people anywhere/anytime. The initial web evolution helped globalize the workforce, but didn’t have as much impact on how we could automate processes, mine vast lakes of data and embrace mobile applications to drive interactions across our employees, partners and customers.

We have entered an era, today, where there is real capability – and need – to change how we run our businesses – from back office transactional processing through to the front office customer interaction: we have tools and apps to target and interpret meaningful data, we have developing software solutions to automate and even robotize processes to mimic human tasks like we never could in the past, and we have all submerged ourselves in a mobile culture where all forms of business are conducted on all types of devices and interfaces.

Perhaps, even more importantly, cloud-based platforms are being developed which allow us to share these capabilities, re-invent the way we run services and process transactions that require such a lesser amount of human intervention and oversight.

Hence, the onus shifts to the capabilities of our talent to add value to their organizations that are insightful to help base decisions; that are creative, which help try new ways of doing things, or targeting new markets; that are innovative, where their organizations can find entirely new ways of competing, or developing unique products or services. Whether they work in finance, HR, marketing, procurement, IT, supply chain, their job is to leverage digital technologies and platforms effectively so they can refocus their time adding value, because the need for people to sit around and fill in spreadsheets all day is being gradually eliminated. People need to do a lot more thinking, and less executing.

It’s less about having specific skills wrapped up in a nice box that can be marketing, such as “ABAP programmer”, or “Vendor Contract Manager”. It’s now about being brokers of capability – people who can multitask across multiple disciplines and find business problems, in addition to solving them.

The Bottom-line: The As-a-Service business world is moving the talent goalposts, and many workers will struggle if they can’t adapt

I truly believe the oncoming wave of As-a-Service is going to be driven by the inability of enterprises to reorient their existing talent to move beyond the traditional transactional outsourcing model.

This talent crunch is already coming. The old safety nets of years gone by have bigger and bigger holes in them – you only need to look at the job ads and the types of skills smart companies are now looking for to understand quickly how irrelevant you could become if you don’t embrace the digitally transforming world we are now living it. It really is time to get with the program, people, or start preparing for an early retirement.

Stay tuned for Foundations III and IV coming As-a-Service style to a screen near you very soon…

After all these years, CSC is finally separating out its public sector and commercial businesses. So what does the HfS analyst team think of it all?

This week’s announcement that CSC would be dividing into two new entities, one for US Public Sector contracts and the other for Global Commercial contracts is a welcome and necessary step. CSC is a capable, trusted veteran of the services industry but it has been disappointing the market for some time now. Lacking the scale of IBM and HP, the brand of Accenture and the overhead structure of leading Indian heritage service providers it has been stuck in a poorly defined market position.

CEO Mike Lawrie has been pulling all the available operational levers since his arrival, by putting CSC back on a sounder financial footing, recruiting new executive talent, streamlining the offerings and building the partnerships required for success in the As-a-Service economy. However, those levers still are not enough and without access to new investment capital to build global sourcing and new technology resources as well as a further refinement of the strategy we wonder how CSC can compete in an increasingly globalized, industrialized and automated market.

CSC’s large and challenging public sector contracts acted as a virtual “poison pill” limiting who could take a stake in the combined entity. Breaking this off will free the leadership to further shape the business than they have been able to do, so far.

CSC has carved itself up into a more manageable portion that will, in HfS’s view, make each entity an attractive investment target that, in turn, will maximize the return for current shareholders. The most likely candidate for the Global Commercial entity is a Japanese service provider and for the US Public Sector portion, we envision a PE firm.

If the goal of this action is to do more than just make it easier for each part to be acquired on its own, then we think CSC for the enterprise market needs to do the following:

Ignite the enterprise sales engine and refine operational processes to make it easier to contract with CSC for deals of all sizes

Invest in the brand so that it stands for something more in the As-a-Service Economy

Look at much larger acquisitions of their own if they want to create momentum and bring in new capabilities. Infochimps and ServiceMesh were strategically sound and brought new leadership into CSC but on their own they aren’t enough to move the entire organization.

Finally, HfS believes they should double down on emerging markets such as Digital and IOT in concert with the rebranding. There are no clear leaders yet in this space and there is still an opening for CSC but it needs rapid and decisive actions on the part of this slimmed down CSC Global Commercial to make this happen.

The data from our brand new “2015 As-a-Service Study“, where we canvassed the views and dynamics of 716 service buyers, providers and advisors, is fresh off the analytics tools, and we’re starting to unravel just how messed up our industry is, as we try and forge a path away from legacy outsourcing practices.

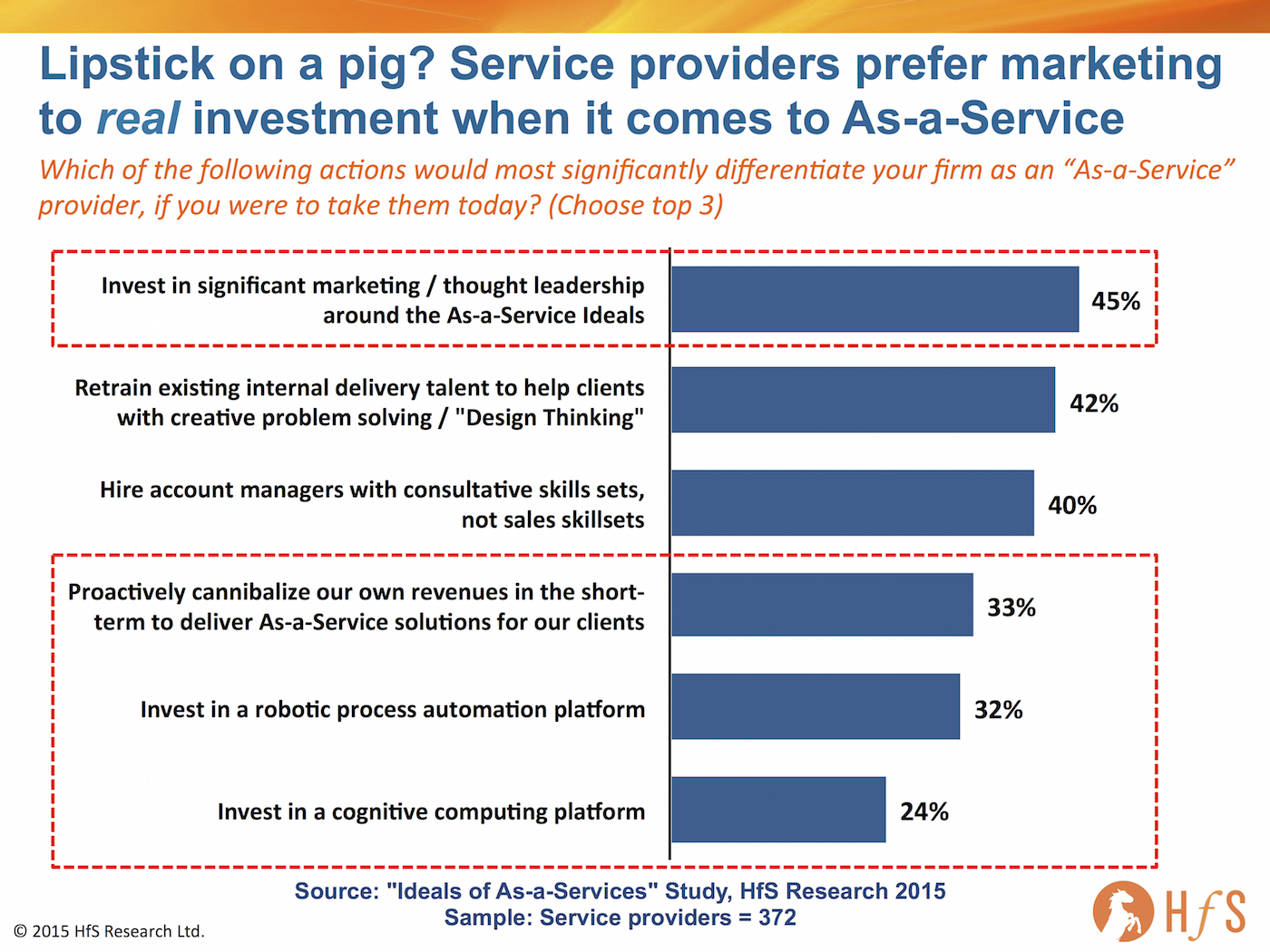

For starters, we asked 372 service provider executives to reveal what actions would significantly enhance their As-a-Service credentials. Naturally, you would expect them to plump for some serious investments in new tools, platforms, talent etc. But, sadly, that’s not quite the case…

Click to Enlarge

Most providers want the glitzy veneer more than the real deal

Yes, folks, most provider executives (45%) want the nice glossy magazine ads, website banners, white papers, airport billboards, webcasts etc., more than anything else. Barely a quarter (24%) want to invest in a cognitive computing platform, a third in robotic process automation, with a similar number wanting to see their firms proactively cannibalizing their own legacy revenues to develop As-a-Service solutions for their clients.

However, providers do view upgrading their talent as a higher priority than investing in new technology, with 42% prioritzing the retraining of existing delivery teams with Design Thinking skills, and 40% bringing in consultative talent from outside to replace the long-outdated cheesy sales approach. The services purists among us can appreciate that providers need to upscale their talent in order to take advantage of evolving technology solutions, analytics and automation offerings.

The Bottom-line: Several providers are facing a slow death if they can’t make genuine changes to the old delivery model

In all honesty, I find this data both depressing and alarming. Most of our beloved providers want to talk a big game more than having the real chops to prove it. It’s just like it was ten years ago when most providers were selling cheap offshore deals under the guise of helping clients with genuine “transformation”. Now, it’s simply many providers selling a more mature offshore delivery scenario with much more sparkly and jingly bells and whistles to impress their clients.

My concern, today, is we’ve become so obsessed with thought-leadership and big ideas that we’re losing touch with reality. What’s more, it’s almost impossible to tell apart most of the service providers – they all have a digital story, an outcomes strategy and at least one guy wielding some form of RPA game plan. We can’t continue in this vein for much longer – we’re all getting increasingly bored hearing the same old guff. What we need is hearing from the clients who are actually investing with their providers. We need to hear about the incremental steps and investments providers are making with their clients to start that long transition from legacy world to that far-off As-a-Service nirvana. We need more reality and less fantasy.

So let’s all dial back the rhetoric and focus on the real investments in talent and technology that have to take place if we’re going to survive in tomorrow’s As-a-Service Economy…

Just a few short years after ADP introduced the basic fundamentals of Business-Process-as-a-Service to the corporate back office with its managed payroll offerings, Workday has rapidly introduced HR-as-a-Service to the corporate, world with its comprehensive HR platform suite, creating a whole new ecosystem of service providers eager to slake the Workday thirst of so many HR heads.

Mention the very words “Workday” to any HR executive today and their eyes light up – they need a Workday go-live on their resumé, just like CMOs need Salesforce experience and most CIOs, in the past, an SAP or Oracle roll-out. However, what’s truly disruptive about the new HR-as-a-Service environment that has sprung up practically overnight, is the emergence of a whole new breed of As-a-Service providers now feasting on the lunch of the traditional providers. What once cost $50m for a complex technical implementation, can now be done for a fraction of the price, with the bulk of the investment being refocused on post-implementation support and HR transformation.

Being able to tap into consultative support that can help with organizational design, or workforce analytics, that is delivered via virtual on-tap models, in addition to the bread-and-butter fulfillment work, has changed the game forever – and for those only just waking up to this seachange, it is already too late.

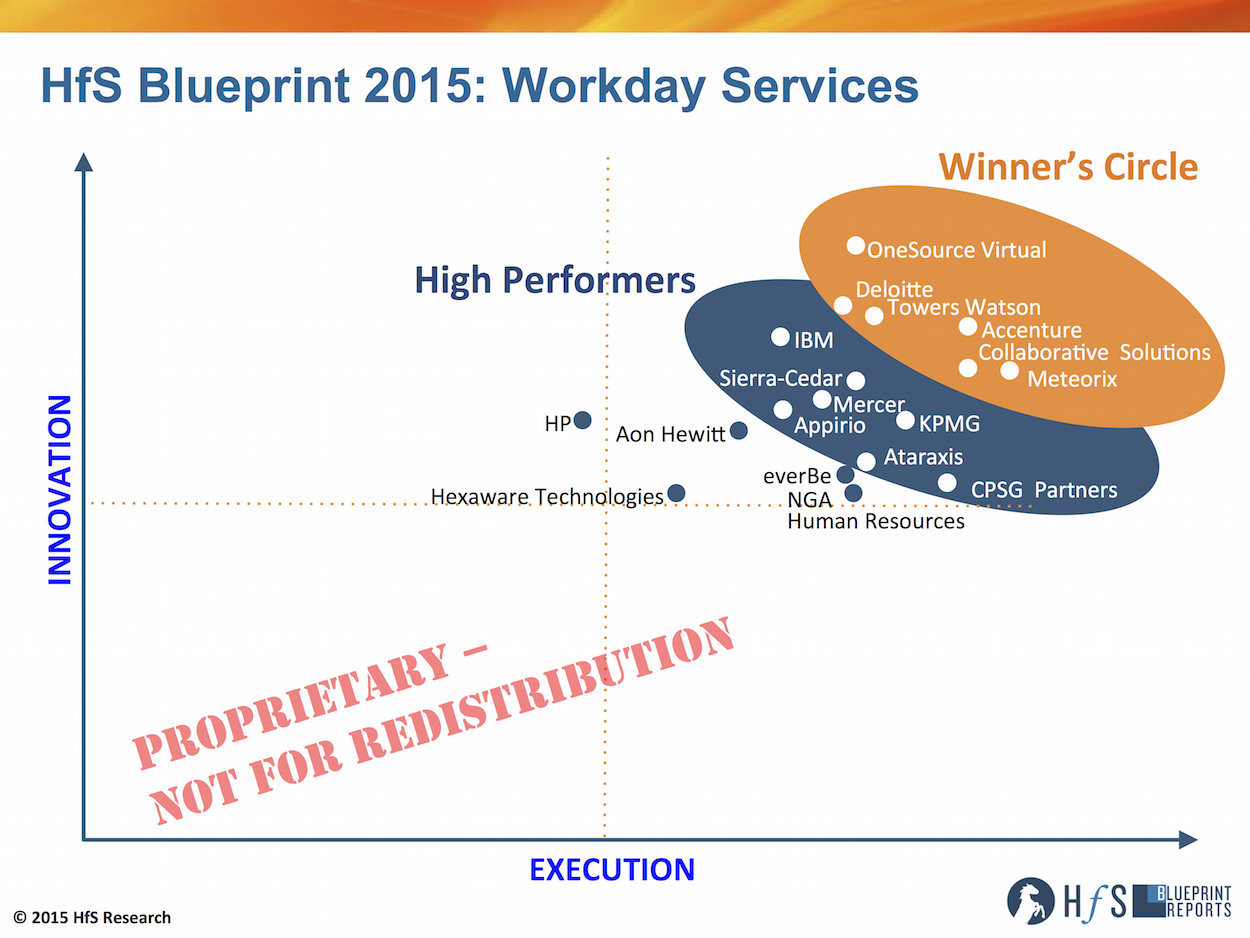

So let’s take a look at how the Workday services environment is shaping up with the industry’s first ever Blueprint report into Workday services, with the help of HfS principal analyst and report co-author, Khalda de Souza:

Click to Enlarge

Khalda…. why do so much research into Workday?

Enterprises are increasingly interested in SaaS applications, as they promise speed, cost effectiveness and simplicity. We’ve seen great and growing interest in SaaS for HR functionality over the last several years and momentum behind the Workday HCM product has been especially strong. Today there are medium and large global enterprises alike deploying Workday, mainly because of its functionality, attractive user interface and its common code instance. Customers are increasingly fed up with constantly adding complexities to their application environments which is often the result of some of the on premise options.

Most Workday deployments to date have been for North America-headquartered enterprises, in some cases including their international offices. In the next year we expect deployments in other regions to increase, particularly in Europe. In addition, other Workday modules are also in growth mode, including Workday Financial Management. So this is the right time to highlight the trends and the leading providers for plan, implement, manage, operate and optimize Workday services in this exciting growth market.

So if SaaS is so easy, why do enterprises actually need a service provider?

Workday wants to help its customers to be as self-sufficient as possible. To this end it has developed the innovative Workday Community, which is an online resource for all customers to ask questions, share experiences and even find partners. Customers can also find resources on the Workday Consulting Services Marketplace. These are invaluable – and our research shows, very popular – resources, but there are still massive opportunities for service providers to provide additional value-add services.

While SaaS applications are generally easier to deploy than on premise applications, it does not mean that enterprises do not require any in-house services skills at all to make the SaaS adoption successful. Unfortunately, some enterprises have learnt this the hard way, by radically reducing their in-house IT team when deploying SaaS. Workday service providers have seen demand across the value chain of services, from consulting through to BPO services. For example, enterprises need to understand the implications of using a SaaS application including the organizational change management that may entail. Workday partners with a deep knowledge of HR and/or finance have also brought deep functional expertise in a holistic manner to customers.

So who are these partners offering to Workday the organization… and how did they do?

Workday’s services ecosystem is one of a kind. For starters, it’s a closed ecosystem, with Workday carefully selecting and inviting partners to join the club. To date there are 28 deployment partners, including Workday boutiques (such as Ataraxis and OneSource Virtual) , HR specialists (such as Aon Hewitt), consultants (such as KPMG) and global general service providers (such as Accenture and IBM). Moreover, all partner consultants are trained by Workday so that they all use a consistent deployment methodology to maintain the same high standard. As a result, there isn’t a weak partner, as they are all at least technically very capable. The differentiators lie in commitment to developing proprietary technologies, customer engagement methodologies and having a clear vision for the market.

In our Blueprint, the boutique partners shone, especially for their commitment to making customers’ Workday experience a success. The HfS Blueprint Axis shown today captures a healthy mix of each category of service provider in both our Winner’s Circle and our High Performers, highlighting the need for the global partners to not take their usual dominant position for granted.

The members of our Winner’s Circle for Workday Services include: Accenture, Collaborative Solutions, Deloitte, Meteorix, OneSource Virtual and Towers Watson.

Our High Performers include: Appirio, Ataraxis, CPSG Partners, IBM, KPMG, Mercer and Sierra-Cedar.

In our Blueprint we also profile the capabilities of other Workday partners including: Aon Hewitt, everBe, Hexaware Technologies, HP, NGA Human Resources as well as of Workday itself.

Thanks for your great insight, Khalda. So… to sum up this Blueprint research, how do you see this market evolving further down the road?

Khalda de Souza, Principal Analyst and Report Co-author (click for bio)

Most Workday engagements to date have focused on consulting and implementation services. We are now seeing an increasing demand for application management and BPO services. Some of the partners have these capabilities but have not necessarily fully marketed them yet as the demand has not been there. We expect these partners to strengthen their offerings and step up the marketing effort. As the Workday financial management (FM) product also grows in demand, partners with both the HR and finance capabilities will be in a stronger position to offer Workday as a platform. Overall, partners with international capabilities will have increased opportunities to grow in the growing Workday services market. For those partners with a gap in any of these capabilities, they will have to at least have an answer for it all – that being, build it, acquire it or partner for it.

HfS readers can click here to view highlights of all our HfS Blueprint reports.

HfS subscribers click here to access the new HfS Blueprint Report, “HfS Blueprint Report 2015: Workday Services“

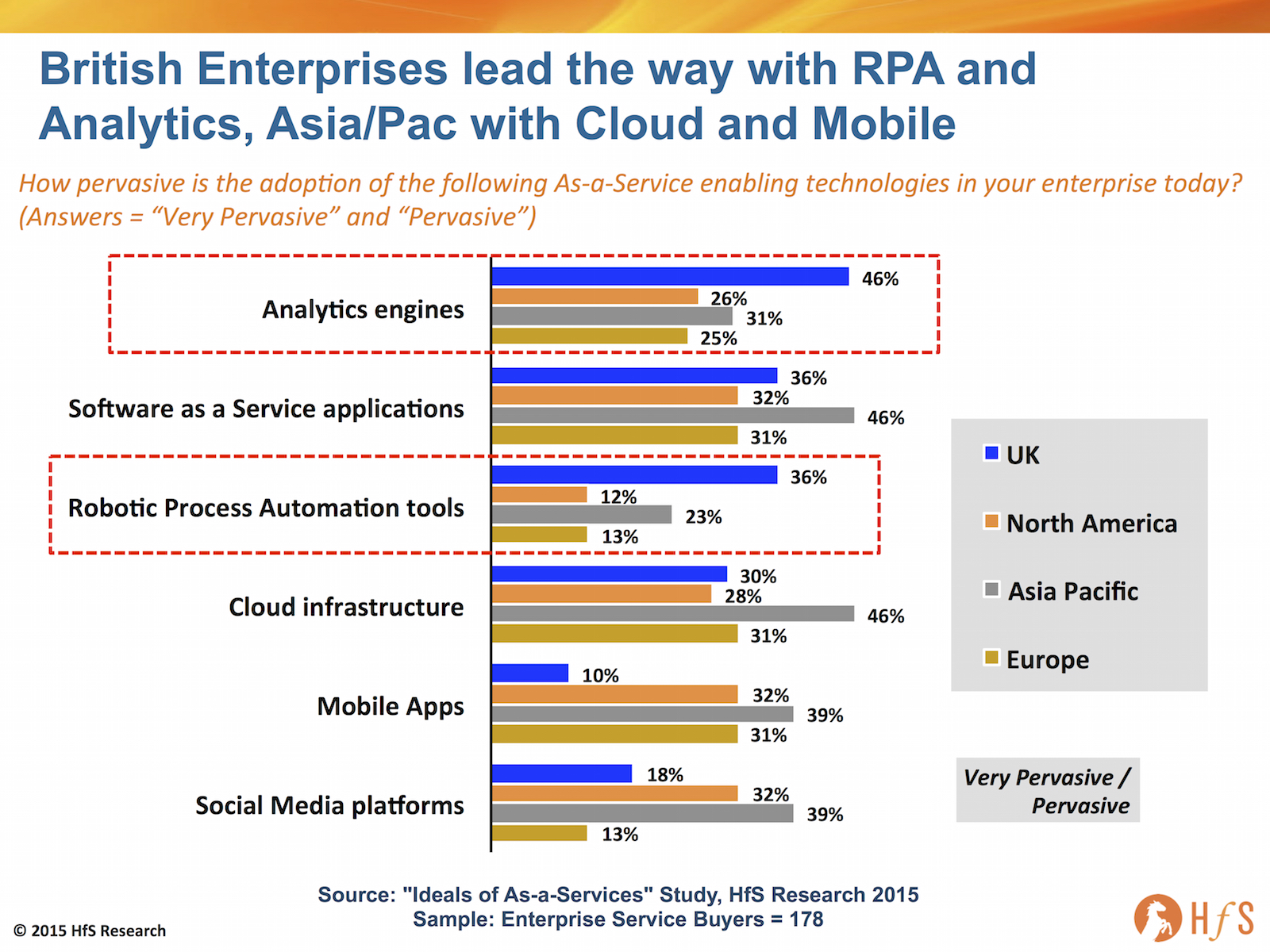

There are a lot of negative viewpoints on Britain’s capabilities to rebound as an economic superpower, after its heyday leading the world into the industrial revolution a very, very long time ago now. However, when it comes to driving out costs, privatisation and outsourcing of labor, and mercilessly adopting new tools and techniques to make themselves more efficient, their leading organizations are pretty damn good at jumping on the train.

And while the British government is the world’s biggest customer of offshore outsourcing (in fact its government has created a whole outsourcing economy of its own), Britain is also home to several of the upcoming automation software firms, such as Blue Prism, Thoughtonomy and IPSoft (a major presence there), the artificial intelligence firm Celaton, and several start-up robo boutiques, such as Genfour, Symphony and Virtual Operations.

Yes, people, when it comes to being first on the bandwagon for experimenting with solutions that can drive out cost and improve productivity, the UK – amazingly after all these years – still leads the way. Our soon-to-be revealed As-a-Service study, which canvassed the viewpoints of 716 industry stakeholders, including 178 major enterprise service buyers, clearly shows how much more pervasive the adoption of both Robotic Process Automation (RPA) and analytics tools are among British enterprises, compared to enterprise service buyers in the other major global regions:

Click to Enlarge

The Bottom-line: As-a-Service is changing the service industry dynamics forever, making it possible for smart businesses to get ahead of the disruption curve

As we delve into these unprecedented survey findings, it’s becoming abundantly clear that the evolution to As-a-Service will be a long and painful one for many buyers, providers and advisors, but the core fundamentals are about enterprises operating with more speed and predictability, a higher quality of processes and more value-based provider relationships, that can enable them to “plug-in” to the services experience.

Enterprises which have opened themselves up to a lot of global outsourcing relationships in recent years, for example many UK-led businesses, are clearly forging ahead more aggressively with the next wave of As-a-Service value, which is building the foundation for smarter automation, more realtime, meaningful analytics capabilities and a much more accessible, standardized cloud driven delivery infrastructure. As-a-Service is a global phenomenon and the future Fortune 500 in 3-5 years’ time will be made of of many nimble As-a-Service driven firms, which are globally ubiquitous, where most services are sourced, and delivered via intelligent cloud models. Yes, the Germans will probably still make great cars, and the American leading in life sciences, the Chinese in hardware manufacturing etc., but the true As-a-Service driven organization? Now that can be anywhere…

Christopher Stancombe is Chief Executive Officer, BPO Division, Capgemini (Click for Bio)

On the week when Capgemini opened its wallet to make one of the largest services deals in history, with the $4 billion acquisition of IGATE, we thought it high time to focus on one business division that’s really been on fire the last couple of years – Business Process Outsourcing.

With Capgemini’s proven capabilities delivering global Finance & Accounting services (see our recent Progressive F&A Blueprint), one of the areas where the firm has needed to invest is in the industry sectors, so I, for one, am excited to see how Cap integrates IGATE’s insurance BPO delivery.

But the one aspect of BPO that keeps us grounded, is the simple fact that’s it still really about people and relationships – about talent and trust, which is why we went out and spoke to 540 business stakeholders on the topic – and you can read the report here. So, without further ado, let’s talk to geologist-cum-Capgemini’s BPO CEO, Chris Stancombe, on how his division is faring under his leadership and how he views the emerging disruption in the market…

Phil Fersht (CEO, HfS): Good afternoon Chris. Great to have you back with HfS – I think it’s been at least a year since you took the reigns as the CEO of Capgemini’s BPO business. Maybe you could start by giving us a bit of an update on how that’s really fared. In the last year, we have seen some really strong performance from your firm, from our analyst vantage point. Maybe you could share a little bit with our audience how it’s evolved internally, how you have built out the team and where you feel you are today with the business.

Chris Stancombe (CEO Capgemini BPO): Thanks for that Phil. It’s good to be back. I have been here now for ten years. And as you kindly said it’s quite a success story really with the growth that we have experienced and the position that we have established for ourselves in the market. When I took over from Hubert Giraud, we had a plan that the two of us had worked on together. With Hubert moving on and also our CFO, Oliver Pfeil, taking on a new role there was quite a significant change at the top so the first thing I wanted to bring was stability.

When we moved into the three year plan, my most conscious thoughts were how do we build on our strengths and go broader and deeper within our portfolio to bring more value to our clients. So clearly we have a number of areas of strengths. F&A is one of those, analytics is another as well as Supply Chain and HRO.

So it was really taking those strengths and being honest with ourselves around where could we really compete strongly in the market and then determining how we go broader. And to me broader really is in two areas. Firstly, focusing on value-add services that unlock new benefits for clients. And secondly, on the volume side, making sure that we leverage our size and capability to deliver processing cost effectively.

In terms of going deeper, things are working very well as we introduce better linkages with our Application and Infrastructure Services colleagues, and all the things that we have been doing on technology like robotics and artificial intelligence and how we bring that into play. We also benefit greatly from developing deeper capabilities for specific industry sectors. As you know, we group our portfolio around sectors which means we can really deepen our knowledge base and develop some very specific, very interesting propositions.

Phil: So do you feel things have really changed all that much, from a client needs perspective, in the last three years? There is obviously a lot of noise in the market around disruption and technology-driven solutions, but when you talk to clients, do you see a dramatic change in their needs? What do you think is moving the industry?

Chris: I would say there is definitely more desire for transformation now. I mean, there is widespread acceptance that just moving some process to an outsourcer and that element of the process being done better and cheaper is not the whole answer. So I think it’s more of a recognition of choosing a partner that can deliver some of the service cheaper and better but also working together to deliver a real transformational impact.

When it comes to technology-driven disruption, one of the big consequences is the speed with which transformation needs to be delivered. The Cloud means a lot of things to a lot of people. Many think you can just summon up an App and then load the app on your mobile. You have a BPO app. And then it’s done and you immediately implement. I think patience is much much lower.

So I think we have seen much more pressure for speed and the ability to convince clients that you can deliver transformation quickly at low risk. As you know, some of our assets around the Global Enterprise Model have really helped us in that because clients can see the route map against which we plan that transformation.

Phil: Chris, you know one of the areas where Capgemini fared very well in our recent F&A blueprint was in the area of talent – and when you read our new report, you’ll see we did pick up very strongly that there was a lot of satisfaction from BPO professionals, in terms of their intellectual challenge. But there was also some ambiguity where it led to in the long term, especially from less experienced staff. How do you view this, when you look at the career paths of the BPO professionals? Do you think this is something people try for a while and then move on to something else, or is BPO evolving into a genuine long-term career choice for many, and will become more widely recognized by our fellow professionals over time?

Chris: Well, Phil, my view is we have created a new profession. I have been in BPO now for 13 years and I view myself as bit of a latecomer to it. There are a lot of people that have been in BPO where that’s the only career they know. They joined as graduates, they stayed in the profession, they have a fantastic client service mentality, they are very innovative, they are very agile. They are keen to work towards continuous improvement. They recognize they want to move into new clients in new sectors. It’s a very exciting industry to be in.

I think what we need now is to create some structure around the profession like other professions do such that therefore there is a bit of prestige. You know if you become a lawyer you are a qualified lawyer and then you have got letters that go after your name, if you are a qualified accountant similarly. I do think we need to start challenging ourselves. What are we doing for the next generation such that people are proud to be in BPO in the same way that lawyers are proud or doctors are proud and engineers are proud? It should be a similar type of professional approach. And I think that’s what we need to bring to BPO now.

Phil: Yeah – it seems that providers like yourselves are doing a good job of creating career paths because it’s your core business. You deliver BPO, Finance, IT “as-a-service” for your clients. Whereas, on your client end it’s often not their core business. It’s support operations. So do you think part of the issue is that providers are getting good at creating the career path, but it’s actually more of a struggle on the buy side to sort of figure out what it means to them?

Chris: I would say obviously it’s much much better to use a BPO provider than try and do it yourself. But in areas where you have a global business service it often becomes a separate company- a captive with its own dynamics, its own leadership. And I do think that rather than just having an accounting and finance captive and then an HR captive under separate leadership, it can all be put under a global businesses service leadership with IT as well. I have seen some very dynamic organizations that create opportunities because in those cases obviously you don’t have the multi-client multi-sector opportunity but at least you do have the multi-disciplinary opportunity.

So I think the less choice you give, then the less interesting it is for people to develop their careers. The very least you need to do is create a global business services organization.

Phil: Chris, so what do you think of the measures that both buyers and providers can take to improve the level of trust in a relationship? What do you see working?

Chris: It’s still a people’s business, isn’t it Phil? So you still have to have the good cultural match between the people in the engagement and the people on the client side. The tone has to be set from the top. So making sure you have regular meetings at the senior level, CFO to CEO. They set the tone. You talk to each other regularly. Make sure that you are transparent and open and have the right people on the account with aligned coaches. Sometimes it’s rotating two or three people through the account until you have the right people working together. So it is being sensitive on both sides you know. I mean the people have to want to work together, they have to want to build a partnership, and be aligned around the same measures. And then if you get people on both sides pulling in the same direction the tone is “We’re in this together. Let’s move it forward” When people like each other, spend time together, and build a relationship then that’s how you get that trust.

Phil: So do you think clients, in general, are warming to a more a trusting relationship with their providers?

Chris: I think it does depend on the client and what the client wants. But the good news is more clients are now open to that part of the transformation. They recognize the value of the people and their longevity, their different experiences, the knowledge they bring, and the assets that we have built. The right client wants to be able to leverage and tap into that value. So I think the evaluation of suppliers is not just around “what’s your price and what service will you agree to”. Increasingly it will be about what assets are you bringing and how you are going to help us transform ourselves, how are you going to help drive that change, create that vision for us because you’ve got a better view of what ‘good’ looks like. It’s the moment where they think “wow, that’s what we want to be like”.

Phil: And you know when we look out maybe a couple of years, how is the conversation going to evolve? Do you think it will get more and more into how much RPA can you do, how good are your analytics? Or do you think that stuff is all going to become absolutely staple to the BPO diet, and it’s going to shift beyond that? Where do you think this conversation is going to evolve to in a couple of years?

Chris: I think CFOs are going to be asking themselves “How are you going to help me drive my customer satisfaction index with the business?” The discussion in two or three years will be how are you going to help me with my measures around the customer satisfaction feedback I am getting from the business units? Also how are you going to help me with my ethics and how are you going to portray the right culture in my organization so your culture and our culture are aligned strongly? I think we are seeing now interestingly when you look at risk and compliance that more and more people are saying actually it’s the culture of an organization that manages the risk better than any policies or policing that you may put in place. If you have the right culture in your organization your risk is lower. And whether that’s ethics and compliance or it’s CSR, all of those things are important and they lower your risk.

So to me the top three critical questions that the CFO should be asking are: How do I build better customer satisfaction with my business? How do I drive value to my shareholders? And how do you help me create the right culture in the organization such that my risk is mitigated?

Phil: This has been great, Chris. I really appreciate the time today. And I look forward to sharing this with the network. It’s been really good to hear your views and how your business is faring.

Chris Stancombe (pictured) is Chief Executive Officer, BPO Division, Capgemini (Click here for bio)

As we correctly predicted last week, Capgemini and iGATE have announced their nuptials after finding many areas of common interest to consummate a long-term flourishing relationship.

In short, this merger further builds on our weekend argument that service providers need to blend the best parts of each other to address better the journey to the As-a-Service Economy, and not solely the really disruptive stuff that could be 5-10 years out on the horizon. OK.. there’s more chance of me being the next Gartner CEO than IBM actually buying TCS, but we wanted to set out the argument why a bout of lovely big service provider marriages could provide an ideal distraction from the spate of depressing quarterly results, while allowing for them to co-develop their investments in areas of real value.

At HfS, we believe this acquisition makes a lot of sense for Capgemini to address several holes in its global service portfolio, shoring up its India presence and adding some serious pep to its US clientele (and brand), financial services capabilities and analytics depth.

What Capgemini Gets From iGATE

North American Clients

iGATE derives over 70% of its revenues from North America with anchor clients such as General Electric and RBC and particular strength in financial services and manufacturing. By contrast, Capgemini gets around 20% of its revenues from North America with the stated intention to grow that very significantly and rapidly across the services portfolio.

Indian Delivery Presence

Capgemini has worked hard over the last few years to build its presence in India starting from the acquisition of Kanbay back in 2006. Today it has 55,000+ FTEs in India as compared to 30,000+ at iGATE. The iGATE delivery footprint may be especially interesting to Capgemini who have been trying to grow their presence in Tier II cities in order to reduce labor costs and iGATE may be an accelerant to this effort.

Analytics

Through its Business Intelligence, Extract Transform and Load and Enterprise Datawarehouse work, iGATE has penetrated into some really large accounts in industries like quick service restaurants, and is now moving up to higher value analytics work for these same clients. This would bolster Capgemini’s already strong BI and analytics practice, particularly with US client, and add ~2500 analytics FTEs, which is always a plus.

Vertical Business Process Outsourcing

Capgemini has historically been a horizontally-oriented BPO service provider with a comparatively limited vertical capability, offering a proven market leading F&A capability, but less impressive in industry-specific BPO areas. iGATE brings real depth in financial services vertical BPO, especially insurance, where the firm been making investments for the last several years as a TPA and a provider of transactional services For example, iGATE has also recently opened a center of excellence for insurance BPO in Dartmouth, Nova Scotia, a first class delivery location for higher value work, and is very active in embracing onshore/nearshore talent to supplement it’s offshore delivery engine. iGATE would also bring vertical business processes (with analytics) in other verticals such as healthcare and life sciences, which would also compliment Capgemini’s growing needs.

Governance, Risk and Compliance services

This was was one of the key ‘emerging services’ areas for Capgemini in the last couple of years, and HfS believes it wanted to build particular depth in domain-specific regulatory compliance services for financial services. iGATE’s client footprint in financial services may be an accelerant for these efforts.

Engineering Services

iGATE can complement the Capgemini’s Engineering services practice which is oriented significantly towards aerospace and utilities clients. By contrast, iGATE engineering services serves medical devices and mining clients including several marquee clients. However this is still a small offering out of the grand total and so it is unlikely to be a significant source of strategic benefit immediately.

No more Capital Letter Confusion

Everytime I try to type “iGATE” I have to double-check where to put the capital letters. Thanks for erasing this headache!

What Capgemini Won’t Get From iGATE

Automation and Cognitive

Capgemini is making strides bringing Process Automation into especially its BPO operations but so too are their competitors especially in Cognitive where the Capgemini vision isn’t clear today. We like what they are doing in process automation but iGATE isn’t going to be a force multiplier to this capability and in fact the integration may distract the team from making advances in this critical investment area today.

The Bottom-line: A solid acquisition to shore up the old model and address the transition to the As-a-Service Economy, but more is needed down the road

Most of the leading service providers today are looking at niche buys that specifically add software IP or a vertical capability, such as Cognizant/Trizetto, or Infosys/Panaya. However, in Capgemini’s case, there are still some significant holes in its portfolio to fill out, most notably a more powerful presence in India, a stronger portfolio of US enterprise clients, and a deeper foothold in financial services. iGATE brings these to the table.

Net-net, we applaud the boldness of this move, and hope, for Capgemini’s sake, the French mothership can integrate the two firms effectively. However, we also hope Capgemini can quickly focus on some specific niches that have real As-a-Service elements so them, such as strong analytics depth in discrete functions, and further industry vertical strengthening. In addition, we are still awaiting the firm to pack its punch in automation and cognitive, where it is beginning to talk a big game, but needs to demonstrate some real investment plans.

When IBM announces a 12th consecutive quarterly decline, when practically every other service provider is trying to mask layoffs and austerity plans as strategic moves to delink revenue from headcount, you have to hold your hands up and admit the services industry is going through a secular transition that is going to get considerably more painful, before it eventually reemerges in the As-a-Service Economy.

Service providers need to address the transition years we are currently in, to reach the As-a-Service promised land

With consolidation of the current environment clearly very much on the minds of senior leaders in the service providers (e.g. Capgemini and iGATE widely mooted to be close to tying the knot), it’s pretty clear that we’re distracting ourselves from entering the As-a-Service world anywhere as quickly as we should be. There are simply too many operations and IT careers tied to legacy ERP and business processes, and too many providers making too much money feeding off this legacy, for the change to happen at anything bar a snail’s pace. There simply is no burning platform for change – no Millennium Bug, no Dot.com bust, no Great Recession in the offing (perish the thought…).

It is my belief that we’re at the start of a ten-year cycle of interim change as operational human labor is gradually replaced by automated platforms that are in turn augmented by analytical and creative talent and cognitive computing. The smart service providers are those which are going to address this ten-year phase of transition head-on and not get distracted by maximizing their position in the old model.

So let’s pick on the biggest service provider of all in the middle of this industry transition, IBM, to assess its options:

The cool stuff is all great, but the dollars are relatively small

While IBM is making many right moves investing for the long-term, it’s this long drawn out medium-term period that’s the real problem. Watson, Apple and Twitter alliances, its new $3bn IoT unit, Softlayer etc. all create As-a-Service mojo, but it’s going to take years to get to the revenue levels that can replace the traditional services dollars that are in gradual decline.

IBM needs to work with clients at the pace they are comfortable with, if it wants to maintain its wallet-share with them. The problem with the current business is that prices are getting squeezed and second tier providers are getting desperate and practically buying deals with the hope of making them profitable down the road and keeping their investors happy.

The solution: Buy TCS and create a dominant giant to crush its competitors

It’s simple – make a move on the largest, most aggressive and dynamic of the Indian-heritage providers: TCS. Together, they would crush the market across all aspects of delivery, all verticals, all technologies because their individual forays in the As-a-Service world could play off each other and get scale even quicker. They would have skill at massive scale and could undercut the competition on key deals – almost at will – if they needed to. Together, they would have the footprint for global delivery, transformational talent, low-cost transactional labor, proprietary automation and cognitive capability, analytics, BPO, cloud platforms, mobility, digital consultants, unique software solutions and product engineering… the list is endless. An acquisition would also give the incentives to restructure the existing labor base of both providers through a very active program of automation.

The Bottom-line: This industry needs a mega-merger (or three) to change the game

Let’s face facts, we’re in a worrying downward spiral in the services business as enterprises and service providers face unprecedented challenges on this inexorable journey to replace operational and IT labor with products. Rather than price-compete each other out of business, the service providers need to figure out how to blend the best parts of each other – especially from the As-a-Service world – to get ahead of the change and the pain, and there is nothing like mega-mergers to mask the change that is needed for a few quarters to keep the Wall St investors at bay. Providers need to buy some time and some air-cover to get this right, and what better than complex mergers?

Now would IBM really buy TCS? Probably never, as there is simply too much history in both providers, and this is just too bloody big. Plus, it would create a leadership challenge of unprecedented proportions in this industry. But this industry needs change, it needs real disruption like this to shake us to our foundations and force the new thinking and new behaviors the As-a-Service Economy demands. Let’s hope this impending consolidation has this impact and we’re having a very different discussion in a few months… let’s keep the conversation rolling!

I recently attended a graduation ceremony and was amazed at the number of students engrossed in their phones, occasionally looking up to applaud a graduate.

I recently attended a graduation ceremony and was amazed at the number of students engrossed in their phones, occasionally looking up to applaud a graduate.

After all these years, CSC is finally separating out its public sector and commercial businesses. So what does the HfS analyst team think of it all?

After all these years, CSC is finally separating out its public sector and commercial businesses. So what does the HfS analyst team think of it all?

There are a lot of

There are a lot of