When we look back at this current era of IT services, we’re going to remember this as the time when many of the leading providers launched their platforms to help orchestrate, analyze, automate and artificially intellectualize the delivery of technology to enterprises.

We’ve already had IBM’s Watson™ and Wipro’s sidekick Holmes™, in addition to the several specialist IT autonomics platforms such as IPSoft’s IPCenter™ and Arago’s Autopilot™, so surely, it’s just a matter of time until we get the full gamut of branded autonomics-driven IT management platforms from all the major service providers. The most recent launch comes from TCS, which has been putting a significant amount of investment and attention into its new IT autonomics “neural” platform ignio™.

So we recently got some time with ignio’s mastermind, Dr. Harrick M. Vin, who’s the Chief Scientist and Global Head of Innovation and Transformation, and IT Infrastructure Services at TCS. Maybe he should just call himself the Platform Professor…

Phil Fersht (CEO, HfS): Good afternoon Professor Harrick Vin! It’s great having you on the blog. Maybe you can start by giving us some color into your background, and earlier career–and how you ended up working for a major service provider like TCS.

TCS’ Dr. Harrick Vin launches ignio this June in New York City (click for bio)

Dr. Harrick Vin: First of all it’s a pleasure to be here, and I appreciate the opportunity to talk to you, Phil. Let me first introduce myself. My name is Harrick Vin and I’m vice president for R&D and Chief Scientist at the Tata Consultancy Services (TCS). I look after our largest R&D center in Pune, India. For the past several years, I have also been driving the overall strategy and innovation for the infrastructure services business unit of TCS. Most recently, my team and I have been involved in developing a product called ignio, which we are launching in the market. I have been with TCS for about 10 years. Prior to joining TCS I was a Professor of Computer Science at the University of Texas at Austin for almost 15 years. At TCS, I have had an opportunity to closely work with and analyze some of the most complex systems, ranging from human systems, technological systems, to large engineering systems. We have used a lot of the learnings about how to manage complex systems, to design ignio.

Phil: So talk to us a bit, Harrick, about why automation is suddenly the flavor of the month in the industry. Why is it suddenly such a talked about topic as we look at the future of services and where things are going?

Harrick: Automation is not at all new, Phil. In fact, the whole IT industry is about automation, because that’s what IT does to the business. In fact, in my mind, the words IT and automation are synonymous. But what is interesting is that while IT has been used to automate business, the way we have been running IT and operations behind the scenes involves a significant amount of manual work. We are still very dependent on a lot of tacit knowledge, experience and intuition that people gather over a period of time while running these systems. Most organizations have exercised several people and process optimization levers to reduce cost, make technology and operations more efficient and consistent. And this has served us well to date.

However, I think the next decade is really going to be all about speed or agility. While the digital revolution has created many opportunities for businesses to transform themselves, it has also created some very tough challenges for the enterprise technology and operations teams. For instance, in most enterprises, technology complexity is on the rise; on one hand, most enterprises are struggling to reduce legacy, while on the other hand, new technology, new applications, new businesses processes are being introduced at an unprecedented rate. Data volumes are on the rise, and decisions are becoming difficult to make. Rising complexity is also leading to increased operational risks resulting from failures, technology misconfigurations and human errors.

Because of these, conventional methods for running technology and operations in most enterprises are starting to fall a bit short. In fact, to deal with complexity, most enterprises IT teams have organized themselves into lots of layers and silos, and deployed many workflows. This essentially ensures that everybody who needs to know or who needs to have a voice gives an approval before something gets done. Unfortunately, this slows things down. Work essentially flows and doesn’t get done very quickly. The lack of an end-to-end view resulting from layers and silos also increases operational risks from human errors.

Thus, the combination of rising complexity, lack of agility or sluggishness caused by complex workflows, and significant increase in operational risks are some of the key drivers that are really making automation of technology and operations essential for the future.

Phil: As you look at the value that a service provider can bring in this space, obviously it’s bringing a lot of capabilities around system integration, bringing together platforms and processes. What do you see new evolving from a technology perspective, that is really changing the game here? Is it that new things are coming on to the market that are creating better types of platforms that are more effective, or do you think it’s just increased skill sets on the services side?

Dr. Harrick Vin talks to us about neural automation…

Harrick: Most enterprises have failed to use conventional automation products or practices to create scalable or sustainable automation. We have seen automation applied in pockets, leading to islands of automation. However, we have not seen most enterprises being able to scale the benefits of automation. This can be attributed to two primary reasons.

First, today’s best practices and tools often require enterprises to embrace a standardize-first model: standardize technology and processes first before you spend the time and effort to automate and thereby derive efficiency and other values. This has often failed because standardize-first requires a fairly large lead-time and there is also no clarity on what is the necessary diversify that one has to actually support. So when you say standardize-first, the question is standardize to what? This is difficult to answer for most enterprises.

Second, perhaps, what has really resulted in lack of scalability and sustainability of automation, is the very fact that most of the current tools or products for automating operations, implement run-book automation, in which a standard operating procedure for doing something manually is converted into a workflow, a script, a program, or a set of rules. This run-book automation model has its roots in manufacturing, where once you configure an environment for automation, the environment doesn’t change much. For example, if you consider a BMW factory that produces a 3 Series car, it produces exactly the same car design for the next several years. But in the case of enterprise IT, everything changes all the time: the workload keeps changing, the underlying technology and their versions keep changing, application functionality keeps changing, new applications keep getting introduced, among others. And all of these changes make automation obsolete, and often leads to automation maintenance nightmare. In fact, because of the challenges in accommodating changes, many enterprises automate only things that are not changing very frequently or things that are at lower layers of technology stack. The higher up you move in the technology stack, the greater the rate of change hence the greater rate of obsolescence.

Thus, to be effective, we need new technologies and products that will enable enterprises to build automation that is inherently designed to accommodate change, designed to accommodate diversity and designed for high degree of reuse, such that automation benefits can be obtained quickly. So, in effect, we need highly intelligent automation with the head-on, rather than dumb automation.

Phil: So let’s look at the next generation solutions to help clients. We talked just recently about an exciting offering that TCS is coming out with called “ignio.” What is different about what you are bringing to market with ignio?

Harrick: Phil, ignio is the world’s first Neural Automation System for the digital enterprise. Let me explain what neural automation means to us. To us, neural automation means four things.

First, it means connected. Ignio has ability to collect data and assimilate data from a large number of enterprise data sources, to create context awareness about what the enterprise environment looks like. In a typical enterprise today, there is no one data source that gives you everything you want. There are hundreds of thousands of data sources that actually contain relevant information. ignio taps into all of these data sources to build context awareness.

Second it is adaptive, in the sense that it does not require an enterprise to make changes to its tools or systems; it does not require standardize-first. It simply connects to what an enterprise has and adapts to the enterprise environment.

Third, it is intelligent in that just like how our brain works, it breaks any complex activity into a large number of smaller simpler tasks, performs each of these tasks and then composes these tasks together on the fly in order to carry out a complex activity. Because it has the ability to create the context awareness, it also has the ability to predict an emergent condition and take proactive actions. So that’s why it is intelligent.

Last but not the least, it is resilient. It is able to accommodate changes or failure gracefully, and reconfigure itself to accommodate change. Which as I said a little while ago, is a fundamental requirement for automation to be scalable and sustainable.

So, in a nutshell, it’s connected, adaptive, intelligent and resilient. These are exactly the characteristics that you would actually associate with a human brain, and how our neural system works. This is exactly what ignio does.

Phil: Why “ignio”? What was the thinking behind the brand?

Harrick: Interesting question. Let me explain. ignio converts every service into a piece of software. By doing so, it is essentially allowing us to create a technology-first service model, whereby ignio has the right of first refusal to do any work, and ask for help when it does not know how to perform the work. So, ignio in our mind is this invisible, evolving intelligence that will ignite and drive change for a large enterprise. That’s what led us to the name ignio.

Phil: So last question, Harrick. When you look at the world today, if you were crowned the emperor of IT services for one week, what’s the one thing you would do to change this industry?

Harrick: That’s an interesting question; let me think a little bit, Phil!

To answer this question, let me draw an analogy between IT services and manufacturing. In manufacturing, because of the industrial revolution, we’ve gone from manual engineering or craft, to mechanized, to now precision engineering. That happened because of the sophistication of automation. If you look at IT services today, we are still very much a manual engineering type of industry. We rely very heavily upon intuition, experience and tacit knowledge to perform different types of complex operational tasks. I believe that the IT services industry is ripe for undertaking this industrialization journey, and this is what I would try to promote and drive.

I also think that converting services to software, like what ignio is designed to do, to enable a technology-first service model for enterprise technology and operations is a critical step towards realizing this industrialization vision. If you look at the last decade or two, we have witnessed disruptions in many other industries, whether it is retail, whether it is taxi rental, whether it is video rental, and so on, where a people-centric model of service has been converted to a technology-first model of service.

Phil: That was very well answered! It’s been a pleasure having you talk to our readership today, Harrick; we look forward to sharing your views with everybody. And good luck with ignio!

Dr. Harrick M. Vin (see bio), is Vice President and Chief Scientist, Global Head of Innovation and Transformation, and IT Infrastructure Services at TCS. He holds a PhD in Computer Science and Engineering, University of California, San Diego, an MS in Computer Science from Colorado State University, and a BTech in Computer Science and Engineering from the Indian Institute of Technology.

We’ve been talking about the great divide between consulting and outsourcing models for decades, but – finally – it’s time for the two to get much closer together as the forces of the As-a-Service Economy combine to weld the two models into a new services mongrel which combines simplicity, efficiency and capability for enterprises finally attempting to drag themselves away from their perpetual treadmill of obsolete technologies and valueless process flows.

The whole premise behind As-a-Service is one of a fundamental cultural change with how enterprises approach their operations and partner more collaboratively with capable service providers to re-imagine their processes, based on defined business outcomes. Simply put, it’s a huge, huge challenge for most current services relationships to morph into anything closely resembling an As-a-Service model, with the current mindsets of most buyside and sellside delivery staff. Buyers need deep expertise to help them reorient their skills and capabilities – and their service providers need to make serious investments and sacrifices to help them, which give their accountants and shareholders hives.

Coupled with the troubles facing buyers and their service providers, is the abject failure of most of today’s sourcing consultants to do anything difference to reform their old way of doing things. Yes, it’s a Catch-22 of many service industry stakeholders not wanting to change their ways, but being forced to address these issues to remain relevant and – let’s face it, employed. In short, the pace at which the services economy is evolving will render many people unemployable in a few short years who fail to get ahead of this.

Just remember how foreign the concept of cloud computing was just five years’ ago… you think it’s going to take that long again for RPA to take hold, and significant advancements in artificial intelligence to reshape how enterprises run their operations? Think again, people; things simply have to change – and these market forces will make sure there will be winners, survivors and losers who will fizzle away into insignificance.

But the answers are staring us in the face – the future of services is a combination of the ability to create business value based on processes that are run efficiently, simplistically, and to common standards we find acceptable.

Consultants make a living demonstrating value in order to create demand to sell their capabilities. This is where too many service providers will terminally struggle

Clever consultants find problems, not just solve them. The only way to get buyers to do anything different is to convince them that hiring you will inspire them to make these changes. This is what able consultants do – they want to be billing themselves out 2,000 hours a year to their clients, so they are constantly looking to find problems, not merely make incremental improvements to existing processes that add minimal value.

BPOs need consulting skills – at scale – to succeed. I hate to say this, but you can’t achieve real success with the next wave of labor-lite solutions with a couple of smart visionary guys living on planes with their PPT mosaics. That may have worked for BPO rounds one and two, but this is round three and there needs to be lots more feet on the ground to be effective. Most of today’s BPOs are operating with very thin layers of consultants to front their client relationships. Simply put, they do not have enough to genuinely scale this beyond a few discreet engagements.

Clients will pay when they see the value in front of their faces. BPO grew up on the sale of immediate cost reduction – a unique value sale that created the industry we are in today. However, as the labor savings run out of room, the sale has to shift to one of future ROI and value – something, let’s face it, which is very challenging for our legacy service providers and advisors to succeed at and manage. However, clients frequently pay for skillful consultants who can come in and make a difference, who will find problems and sell their capabilities to solve them to their clients. The As-a-Service value proposition is really a combo of this consultative prowess and the efficiency and simplicity of effective BPO. So, the two need to be better conjoined to grant clients what they really need. (I stress the term need, as opposed to want, as many enterprises do not know what they need, so there isn’t too much to want until they have it spelled out in front of them…)

BPO delivery staff are simply not very “right-brained”. It’s just how the industry has evolved – lots of people who have a transactional mindset. They do what they are told, they follow a process… that’s nigh-on impossible to change. However, put BPO staff under the management of skilled consultants and this impossible mindset may just start to be molded.

Consultants will struggle without an As-a-Service delivery model behind them. While BPOs clearly need consultants, the same applies vice versa. Clients increasingly do not want to spend millions on custom engagements – the cash just isn’t there, like it used to be, to reconfigure their operations. However, they will buy managed services that are predictable and have a sustainable value proposition. I have used the term Expertise-as-a-Service for a while now, and it’s making increasing sense as the realities of the As-a-Service Economy continue to unravel.

There is no written curriculum for this industry to follow. Yup – we can rewrite the rule book, folks. We’re really venturing into unchartered waters, so what’s preventing this marriage of business models?

New market entities can chase after As-a-Service projects without the risk of self-cannibalization. This is significant. Let’s just assume, for example, Deloitte purchases an F&A BPO business and launches a spin-off As-a-Service provider business that doesn’t conflict with its audit business. This new entity can bid for brand new As-a-Service deals that incorporate the benefits of RPA, AI etc without any legacy revenue that will get eroded – it can pick off re-bids from legacy deals that have become stagnant, in addition to bidding for “virgin” As-a-Service deals from clients venturing into the model for the first time. Bottom-line – all new business is gravy.

As-a-Service demands the whole gamut of people-process-technology change. The pilgrimage to As-a-Service is all about simplification – people willing to offload the transactional work to focus on higher value talks; IT willing to write-off legacy applications and systems that may have absorbed millions of dollars to keep them functioning over the years; and processes that have become obsolete and need re-imagining to align with providing genuine value.

Clients need to trust providers to give up more… consultants are successful because they build trust. This is what consultants do – they invest in clients to trust them, as trust is all they really have. Service providers struggle to build trust because it’s all about the deal to them – once they have a contract, it’s about meeting the obligations, as opposed to really building that trust. It’s just the nature of the relationship.

The Bottom-line: Change is coming with the advent of As-a-Service, and it might not be quite what you expect

You only need to have a few conversations with key industry stakeholders to realize something isn’t quite right with the industry these days. Many buyers are in denial that they need to do anything different, despite all the disruptive technology emerging; most service providers recognize the disruption, but are more concerned with sounding impressive than actually delivering. Can we really progress in this era of denial and bullshit? Of course not…. we will see a few bold moves to get ahead of this market, and some may well come from this potential marriage of big consulting and big BPO.

It’s high time we brought the HfS show back to our hometown of Cambridge MA this December, where we’ll give everyone a big reality slap around the face with a wet kipper:

Yes, people, it’s time to dial back the rhetoric, stop talking about fantastical things that will probably never happen, and get to the heart of the matter: how can we actually define and realize business outcomes from outsourcing?

This will be a service buyer event, where we have 45 exclusive enterprise buyer seats reserved for the chosen few, and we will wheel in some unsuspecting service provider leaders for our famous face/off debate, where we are going to challenge them on why they aren’t self-cannibalizing, why they all insist on using the same lingo we can barely comprehend, and how they plan to be different from each other when the fog lifts.

We’ll be holding the HfS Working Summit in Harvard Square just down the road from our headquarters. So mark your calendars now:

Defining and Realizing Business Outcomes

HfS Working Summit for Service Buyers

December 1-2 2015, Harvard Square, Cambridge, MA

More details–including the agenda, accommodations, how to apply for registration and sponsors–to follow very soon.

Bookmark our event site to stay up to date! Drop us a note to apply for a seat (Service Buyers Only)

We hope you can make it to Harvard Square this December. It will be a great way to end the year and get ready for 2016. And, of course, we’ll have a little fun, great food and booze while we’re at it.

This will be an invitation only event, but we do encourage you to drop us a note if you are interested in applying for a seat. It’ll be great to have you there to celebrate the year we’ve had and get stuck into some unvarnished debate!

The beauty of procurement is that is was never really geared up for cheap and cheerful labor-arbitrage based BPO. In short, most procurement functions have been cut to the bone in most organizations, and many still rely on fax machines, photocopiers and copious filing cabinets of yellowing contracts to get the job done.

Shipping this stuff off to far flung offshore destinations for a few FTE savings has rarely proved to work very well. However, creating a capability where clients can plug in to a whole new experience of procurement capabilities, category expertise, spend management analytics and gain-share opportunities As-a-Service is now happening for many ambitious buyers and service providers.

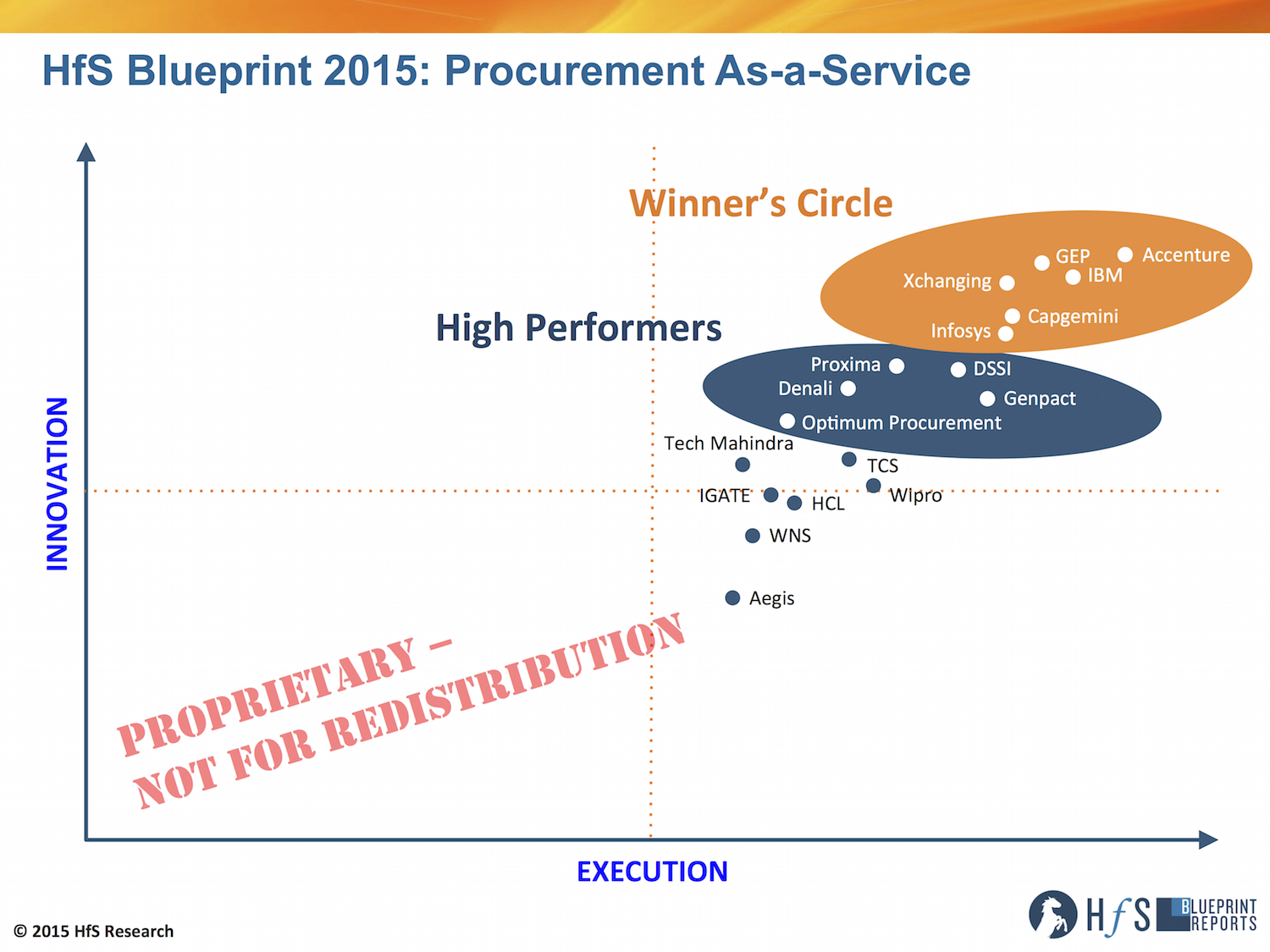

The procurement outsourcing market has evolved significantly since 2013 since HfS launched its first Blueprint, covering 14 service providers, to this new report that covers 18, co-authored by analysts Charles Sutherland and Hema Santosh. This new report is looking very closely at the evolution of procurement services from its legacy outsourcing roots in lift and shift mega-deals, coupled with strategic sourcing consulting, to the increasingly available As-a-Service solution models offered today.

The latest HfS Procurement-as-a-Service Blueprint captures the transition of service providers into the As-a-Service Economy:

Click to Enlarge

What has changed since 2013 in procurement outsourcing services?

If we look at where we are today, or starters, we’re living in a post Procurian world, as its acquisition by Accenture in late 2013 shifted the competitive landscape. Both were in our 2013 Winner’s Circle and when combined they created a market leader by share and by innovation. When we first commented on the acquisition we expected several more would quickly follow especially for Genpact and Capgemini who needed to replace the partnerships they had been developing with Procurian. It turns out that rather than buy at least for now, those service providers who had gaps in capabilities or technologies turned to partnerships instead.

Indeed, partnerships between service providers born out of the transactional procurement market (e.g. TCS, Genpact, WNS) and those out of the technology (e.g. GEP) or strategic sourcing (e.g. Proxima, AT Kearney) are more prevalent in 2015 than they were back in 2013 as service providers construct end-to-end offerings to better compete with Accenture and IBM in particular.

But acquisitions didn’t end with Procurian. Xchanging has followed suite with two more that have revitalized their presence in North America and brought them a new proprietary technology base. While Infosys has accelerated the value of the 2011 acquisition of The Portland Group by utilizing their procurement consulting skills

Internal investments have also mattered over the last several years with service providers increasing their development budgets significantly while also spending on adapting solutions models. In fact over the last two years we have seen previous solution models of end-to-end procurement lift and shift and sourcing consultancy become impacted by the arrival of more modular technology supported service delivery models. While still not the broad norm, this “As-a-Service” approach is setting roots in many service providers and we expect this to increasingly be the norm in the years to come.

So in many ways the last several years have been less revolutionary than they have been evolutionary with a slow and steady acceleration for all end-to-end service providers in the breadth of their offerings and only modest movement in their Blueprint positioning as a result. It should be noted though that the specialist service providers have markedly picked p their game in the last few years and now have a much more prominent place in our evaluation than before.

What matters today in procurement outsourcing

We are seeing slowing growth. Procurement outsourcing while still much smaller than F&A or HR is becoming a substantial multi-billion market and with that we have seen a slowdown in overall market growth from 10%+ a few years ago to something more in the 6% range and so the competition for new clients and renewing deals is greater than ever.

The nature of transactional procurement is changing. Transactional Procurement for the last decade has often looked like a “lift and shift” model supplemented by post transition process excellence projects by service providers. In the last 18 months, we have seen a rapid evaluation of the potential first for robotic process automation and of late cognitive computing as well to this process in order to move away from the labor arbitrage heavy model of the past and to improve overall delivery speed and quality

Sourcing and category management still in demand. Client value creation and service provider differentiation often depend on the breadth and depth of the available sourcing staff in the service provider. The battle to hire and retain sourcing expertise is significant especially as clients in both North America and Europe are looking for the on-site availability of consultants from their outsourcing service providers. Many of the strategic actions undertaken over the last several years by the service providers including acquisitions and partnerships have been made in order to address gaps in organic indirect sourcing category coverage.

Procurement technology and technology management has never been more important. Service provider technology has always played a role in procurement delivery but in the present market with the increased availability of SaaS solutions it has increased again in importance. We have increased the attention and weighting given to technology in this iteration of the Blueprint and spent even more time reviewing service provider capabilities and strategies for technology as well as what it feels like to be an enterprise client today that is increasingly reliant on technology they no longer control to deliver procurement results.

Moving to As-a-Service. We are certainly not there yet, but procurement outsourcing service providers have made extensive efforts over the last several years to further transform their offerings from “lift and shift” transactional procurement together with consulting led sourcing to more modular, integrated, technology based as-a-Service solutions.

Which service providers are taking advantage of this market?

Our 2015 Blueprint Winner’s Circle members who led in our evaluation of the criteria on Service Provider Execution and Innovation are: Accenture, Capgemini, (promotion) GEP, IBM, Infosys and Xchanging (promotion).

Our 2015 High Performers include: Denali (new entrant), DSSI (new entrant), Genpact, Optimum Procurement (new entrant) and Proxima.

So what does HfS expect will happen next as this market unravels?

HfS’ Charles Sutherland, report co-author, having a bit too much of a good time in Kraków last week

Crystal ball gazing in procurement has proven to be challenging over the last few years but let’s throw caution to the wind and make at least three bold predictions about where we will be by the next Procurement As-a-Service Blueprint.

There will be a much greater commercial adoption of As-a-Service in procurement as current trends towards modular processes and hosted software make further inroads.

There will be much more extensive adoption of robotic process automation and cognitive technologies in procurement than we have seen so far. For most service providers these are still at the PoC or limited deployment stage in procurement but we don’t see that being the case for much longer.

Some of the recent partnerships especially for sourcing and category management not lasting the test of time and leading to increased efforts to grow organic capabilities

Attracting and retaining leaders in strategic sourcing and category management will continue to be a struggle for many service providers as that is part of the solution we don’t see diminishing in value or importance anytime soon.

So that’s our take on Procurement As-a-Service in 2015. Please do share your thoughts with us as this important segment of the business process market continues thrive, and…

For you HfS subscribers, please click here to download your full copy of the report

We’re participating in two sessions at the NOA Symposium held at etc. venues, St Paul’s on Wednesday 24th June. We’re also sponsoring the pens (which will surely create an avalanche of new delegates)

Click the logo to get more details on the 2015 NOA Symposium

I’ll be part of a panel with a motley assortment of legacy analysts from Gartner, Everest and NelsonHall as part of “The Outsourcing Debate”, moderated by the Professor of Process himself, Leslie Willcocks. This meeting will surely produce some fireworks as we vehemently debate the most overhyped and underhyped ITO and BPO trends in the UK.

Then, I’ll be chairing a workshop session on “Transitioning to the As-a-Service-Economy.” This is a subject sure to be close to the hearts of many of our readers and we’ve lined up a couple of HfS community friends to co-host with me, John Ashworth, VP Finance Transformation and Systems at Pearson, and Steve Turpie, Deputy Chairman of West Suffolk NHS Trust.

NOA Symposium… all the outsourcing royalty will be there

We’ll weigh the importance of the ideals of the As-a-Service industry vision, discuss how to get the right mix of technology and talent, and evaluate how the painful shift to As-a-Service is/will impact traditional buyer/supplier relationships.

The Symposium will be followed by the NOA Summer Party (we guarantee it will not rain), where booze and entertainment (whatever that is) will be provided for the rest of the evening. I’ll hopefully see you there!

You can book your tickets for the NOA Symposium online via the NOA website.

If you have any questions, you can email NOA Events Manager Stephanie Hamilton at [email protected] or call her on 0207 292 8692.

We’re excited to be heading to Krakow next week to participate in the two-day 6th ABSL Conference from June 16-17.

The great agenda features 80 speakers who will engage the 800 delegates in attendance in discussions about strengthening talent management and supporting regional business leaders for their next global roles in (and beyond) the industry, achieving sustainable and accelerated growth of the sector for the next decades, stimulating innovation and improvement culture, and taking advantage of the technology and client expectations revolution.

With any luck, I’ll get a selfie with Tony. Show up yourself and see what happens.

I’ll be standing on the same stage as Tony Blair (he actually shows up right after our panel discussion where I will attempt a selfie… stay tuned) when I deliver the Keynote Presentation, titled “The Four Foundations of the As-a-Service Economy: The Industry Has Spoken” at Auditorium Hall from 12:40 – 13:00 on Day 1. My talk will look at how the emergence of As-a-Service represents the most disruptive series of impacts to the traditional global services industry that we have ever seen. I’ll share some of our new research, covering more than 2,000 enterprise service buyers in the HfS global community, which paints the picture of what our industry needs to do to get ahead of this impending disruption.

HfS Executive Vice President Charles Sutherland will facilitate a Day 2 Panel, titled “Looking for more fuel! – how to build on current success?” The discussion will focus on the experience of world class GBS organizations, as well as the next SSC trends and opportunities.

Charles will be joined by a group of industry luminaries, including Tom Bangemann, Senior Vice President Business Transformation, Hackett Group; Adnan Behmen, Associate Director GBS, Procter & Gamble; Wojciech Karpinski, Services Head, Global Operations Manager, Infosys BPO Ltd.; Agnieszka Kubera, Managing Director, Accenture Poland; and Magdalena Wlodek, Director Finance Service Center Europe, PMI.

This will be a terrific two days. I hope to see you there!

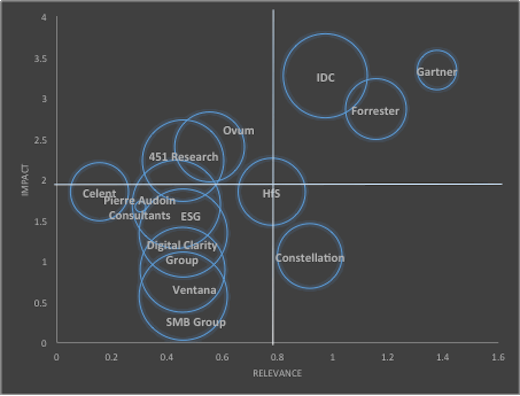

We’ve been doing this research things for a while now. The blog started in 2007 and HfS Research has been around since 2010. It’s really a blink of an eye when you think about it–especially compared with the established firms that we knock heads with every day:

But what keeps us going, apart from the great (and sometimes insane) clients we work with, is the knowledge that we’re doing the right thing – or at least we convince ourselves we are. But, occasionally, there is independent confirmation that tells it like it is, for example this new analysis from the International Institute of Analyst Relations, which surveyed analyst relations professionals from 60 organizations.

Again, here we are in the mix with the Gartners, Forresters and IDCs of the world in The IIAR’s now infamous “Tragic Quadrant,” which IIAR just released on the impact and relevance of IT analyst firms. As you can see, we’re square in the bullseye on the Impact and Relevance quadrant, along with Interaction (which is depicted by the size of the bubble). What’s really encouraging for HfS is our reach beyond outsourcing and services into mainstream coverage of technology – we really seem to have left some of the niche analyst firms in the outsourcing space behind.

We’re not much for living in bubbles, but it’s not bad for your favorite insurgent firm. And we assure you, we won’t let it go to our heads. Honest we won’t =)

The world we’re venturing into is demanding a very different approach to how we progress our capabilities and careers, and I’ve never seen so many enterprises so fixated on finding innovation-capable talent, when looking to hire senior executives. The hiring process for new talent has never been so complex and challenging for ambitious enterprises, desperate to avoid yet another disappointment of ending up with someone who talks a big game, but fails to deliver the goods.

And while it’s harder than ever to re-invent yourself to satisfy ever-demanding employers or clients, it’s also a great opportunity for many of us who have the determination, willingness to improve and application to take our careers into the As-a-Service world. However, today’s work environment is also posing a huge threat to those of us unwilling to change with the times, or are simply seeking to ride out our final working years in the hope we can escape unharmed with our retirement nest eggs.

However which way we look at this, building our personal brands is the critical ingredient for furthering our career potential in this unraveling As-a-Service world. So let’s evaluate how to make some basic shifts from yesterday’s reactive worker to one which ambitious employers are going to want to lure…

Seven Simple Steers to avoid Screwing up your Personal Brand

1. Get rid of the 9.00-5.00 work mentality.It’s amazing how many people still operate like this. You can’t possibly function if you still have this attitude to work and never take calls / return mails in the evenings or weekends etc. Ambitious business leaders no longer want people who just don’t want to put in the extra effort and time to be effective in their roles. If you really don’t want to work hard, then find a career that doesn’t warrant that – sadly, it won’t likely be very intellectually stimulating… but that’s the tradeoff these days.

2. Be a people person… or at least pretend to be. Networking and having people want to engage with you has never been as critical as it is today. Email and social media is fun to communicate in soundbites, but nothing beats meeting up socially, talking on the phone etc. I know many people out there who just don’t like people very much – it’s just in their DNA. This is something you have to fix – if you’re not great to engage with, it’s going to hold you back. You don’t really need to like people to have a functional relationship with them.

3. Stop being an asshole… you know you can try. Let’s face it, we all have to deal with them. Just don’t be one yourself. I know several people who just persist in badmouthing me and my firm because they compete with us – or just are assholes. Can’t we all get along? Share a few jokes or have a drink at a conference? Can’t we even pretend to like each other, or at least be civil? In today’s world, it just isn’t the way anymore – we work hard enough not to need to deal with negativity and bad vibes.

4. Use social media to promote others, and not just yourself. Nothing irritates me more than those people who only tweet or use LI to promote their own work. These people who self-promote to the point of narcissism, and never bother to promote others….ugh. It’s like going on a date when you were younger and having to listen to someone just talk about themselves all evening. If you only ever promote yourself, people will quickly notice and start to avoid you. Fix this habit and force yourself to me more than being all about YOU.

5. Become genuinely collaborative and don’t just pretend to be. Yes, we all know the types, but the more you collaborate, the more people will enjoy working with you and the more you will learn from others. Take the attitude that if you give, you will mostly get back. However, nothing beats having a genuine reputation for being collaborative – it’s such a big plus in the emerging work environment. Noone likes the non-team players and it’s easy to uncover who they are in today’s environment.

6. Figure out how to self-improve by looking at yourself and being honest once in a while. It still amazes me everyday how many people are simply incapable of being able to take a good look at themselves, identify their weaknesses and work out how to improve on them. Deep down we all know what we’re good at and where we are falling short, we just need to work harder at the latter independently as we’re not always going to have someone telling us where we need improvement. Being able to self-improve is an amazing quality in today’s world if you can open your mind to doing this. If computers are self-learning these days, we need to be too…

7. Be creative and unafraid to refocus your abilities on achieving business outcomes. This is so important today – you can’t just box up your skills to say “I’m great at Salesforce.com”, or “I have 20 years experience doing FP&A, ABAP programming, deal negotiation, HR policy etc”. You need to focus more on business outcome capabilities where you can clearly demonstrate how you identify problems and solve them in creative ways that add real value and future growth potential for enterprises. For example, you need to prove you can “Re-orient a firm’s whole go to market focus to open up new growth opportunities that might now have been obvious previously”; or “Re-define and simplify what data a firm needs to be effective in an industry”; or “Evaluate an automation strategy investment by identifying which processes would provide a genuine business advantage being automated, versus those which would cause more headaches than they are worth”.

Bottom-line: We mustn’t settle for easy, we need to keep pushing ourselves in today’s work environment

I will be the first to hold my hands up and admit I am not perfect – am sure I have many enemies and resentful individuals out there I managed to somehow rub the wrong way – and I am sure I could have been more successful than I currently am today if I had not made many mistakes with my career choices and business decisions. But I do passionately believe we need to constantly challenge ourselves to stay ahead of our careers in today’s environment. Simply settling for the fact we have already reached the ceiling of our capabilities and career potential, could likely take us on a downward spiral faster than we realize as we increasingly compete with a broader spectrum of people for our jobs and our clients.

One of the most scintillating sagas of the year has been the unravelling of the great Alsbridge European mystery, with their previous UK entity being reincarnated under the name Aecus (the son of Zeus) and Alsbridge US preferring to grow its own European business, as opposed to persisting with a franchise strategy.

Clearly, CEO Chip Wagner and his cohorts had grander ideas than merely hiring a few local boffins – and their recent acquisition of Source accelerates the firm up the value chain of sourcing advisors. Source has developed a growing reputation for itself under the leadership of its founders Barry Matthews and Eleanor Winn, adds 20 staff schooled in ITO/BPO, vendor management, governance and SIAM skills, as well as demonstrated robotic process automation/autonomics insight, expertise and hands-on experience. Geographically, they have a track record in the Nordic market, a hotspot in the industry, and will bring credibility, should Alsbridge choose to focus on that area in the future.

So we recently caught up with the affable Barry Matthews to learn a bit more about what Source brings to the Alsbridge mothership…

Barry Matthews is a Managing Director for Alsbridge in the UK (Click for Bio)

Phil Fersht (CEO, HfS): Good afternoon, Barry – thank you for joining us on HfS, it’s a pleasure to have you with us. Your company, Source, recently got acquired by Alsbridge. But before we go into that, maybe you can just give us a very quick high-level bio and how you ended up in the advisory world.

Barry Matthews: Okay, no problem. It’s a pleasure to be with you. My background is in the service provider supplier side of things—predominantly in the IT world.

I was at GE Capital selling and delivering big infrastructure deals for a number of years. And then at Sapient, back in the day when we it called “globally distributed delivery.” It seems to have become offshoring. So I have a lot of expertise in delivering offshore deals. I then was an independent consultant in the outsourcing space before I joined Alsbridge plc (now known as Aecus) in the UK back in, I think, 2005. I setup their IT sourcing practice and had a very enjoyable time with those guys before I left at the end of 2009 to set up Source. We had five very enjoyable years before Alsbridge approached us six months ago to rejoin the Alsbridge family. I’m now one of the managing directors for Alsbridge in the UK. So, yeah, it’s been an interesting journey. I now have the same email address I had six years ago.

Phil: So all your old spam is coming back to haunt you…

Barry: Exactly!

It’s the same Alsbridge brand, but it’s a very different organization from my earlier tenure. It’s very fast paced and rapidly expanding. There was a real meeting of minds when we had the discussion about whether or not it made sense for us to merge. It is very exciting. It’s more like a startup in the UK. And we now have got a number of service lines we didn’t have before and are able to offer the CIOs and CFOs we work with completely different services. So we are excited about the next 12 months or so.

Phil: So – in a nutshell – what was it that attracted you most to the Alsbridge business? I’m sure there were probably a few other bigger advisory shops that would have loved to absorb you. What was it about Alsbridge which made you choose them?

Barry: I am sure it sounds trite but culturally I think we were really well matched. When I first met Chip Wagner it was a real meeting of minds. And they painted a vision of what they wanted to achieve in Europe—which was what we wanted to achieve—and where they were trying to give outsourcing a much more positive brand and shift the focus to positive outcomes. They felt that we were doing a good job with the one service line we had, which was outsource advisory. They were able to bring another five service lines and really expand our offering. And so with them we saw that we’d be able to make much more of an impact for the industry. So we agreed with that and went ahead with it.

And so there was that fundamental meeting of minds. And the other area that we were talking a lot about these days is automation—whether it’s RPA, IPA or artificial intelligence. Alsbridge really falls into our vision for that and what we have been doing. And we have some exciting plans. Then there’s the investment opportunity of really building that practice in the UK and in Europe. So we are excited about that as well.

Phil: Alsbridge has been making quite a lot of noise about the RPA space. But, getting past the hype, what are you generally seeing from the client side? Are you seeing some real traction here or are we still early days and it’s a few people just dabbling?

Barry: It’s interesting really. I have been thinking about robots and RPA for the last three years or so. And it’s only recently that it’s been talked about a lot really, if I am honest. We were the first advisors to set up an RPA practice, which we did 12 months ago. And until about 6 months ago it really was still a lot of talk and not a lot of action. But in the last six months we are now really starting to see some traction in the industry.

Interestingly, on Tuesday we had a service provider summit in London at the Oval. We had all of the major service providers there. There were about 130 people in the room and I asked for a show of hands around a panel on RPA as to which service providers were really taking it seriously now and putting in place—you know, big programs around RPA as a strategic differentiator for them or something they were taking seriously. And 80 percent of them put their hands up. You know that wouldn’t have been the case 12 months ago. We have been running a RFI in the RPA market for the last three years and are seeing big changes in terms of service providers taking it seriously now.

So we have seen a big difference in the last six months. We now have 10 proper RPA engagements where we are not just talking about it but are doing actual billable work with customers to advise them on business cases, processes that they should start with, software vendors they should work with and change management around it. And that wasn’t the case six months ago. It is now. We have got some really interesting customer engagements on the go and a big pipeline of opportunity too.

I think we have reached the turning point. I think people have stopped talking about it and have started doing stuff now.

Phil: And where are you seeing most interest and traction on the process side? Is it in F&A or is it just a broad spectrum?

Barry: It’s a really broad spectrum of stuff. Brands are hesitant to allow us to go into details, for obvious reasons. But we have a range of customers and it depends on the industry. We are working with a utility provider and have looked at 15 different processes that are very, very specific to the service they provide to their customers. We also are working with a big car manufacturer.

And we are looking at all of their non-operational processes to identify automation opportunities. We work with an insurance broker—and that’s very specific to underwriting processes. We are working with a water company and that process is related to customer billing. So it really varies. It’s not just in F&A or in HR. It’s more industry-specific processes.

Phil: Barry, maybe you can clarify something for our readership. We have seen some confusion around what people generally term as “automation.” You know, what is legacy automation and what is RPA? Can you explain to our readership what the real differences are?

Is it a bird, a plane? Nope. It’s just Sourcing Superman, Barry Matthews! Oh dear…

Barry: Yeah, sure. I think there is a lot of confusion. I’ll talk to customers and they’ll tell me, “We’ve been automating. We have been implementing Oracle or SAP, and we are going to implement business process management systems.”

And isn’t that automation? Absolutely, of course it is. It is automation.

What we are talking about is replacing manually intensive processes—processes that don’t lend themselves to the large-scale BPM programs, things which are sort of swivel-chair processes that have been carried out by business process outsourcing or offshore for a long time.

And the way I describe it to customers is sort of like the software we talk about is macros on steroids. It’s simple stuff. It really is simple stuff. And you don’t have to automate an entire process. You can automate parts of a process incredibly quickly using the new software tools which typically they don’t know about. And so it’s really the long tail of the specific processes, which typically you would use a person to do, that can be automated pretty rapidly. So it’s mapping what people have been doing manually for quite a long period of time and monitoring them. It’s rule-based. Setting up a process to automate what they were doing previously rather than having to rely on a big IT program.

Phil: One final question I have to ask is this, Barry: If you were crowned king of RPA for one week, what would be the one task you’d try to achieve for the industry?

Barry: A good question. I would try and free people up from doing boring stuff I think to be honest. There is so much in our industry whether it’s in IT or in business process where there are people doing incredibly low level quite frankly boring tasks again and again and again. And if you can free them up to do more interesting and more value adding stuff by replacing that boring stuff with technology then I that would say that would be a good thing to do in my brief role as king. So I would rid the world of boring mundane tasks.

Phil: That is brilliant. Thank you very much, Barry!

Barry Matthews will be speeding to your sourcing rescue if you email him right here…

In Part 1 of our Four Foundations, we discussed the challenges and opportunities facing enterprises which are not taking better advantage of outsourcing relationships to help plug their talent and capability shortcomings.

However, while it’s one thing to talk about the delights that await ambitious enterprises when they make definitive plans go down this path, it’s another to assess whether they truly recognize the burning platform to take themselves through this period of pain and complexity to get there.

Foundation III. A Burning Platform for Change: As operational efficiency becomes a commodity, operations professionals need to strive for that next threshold of value, or find themselves rendered irrelevant

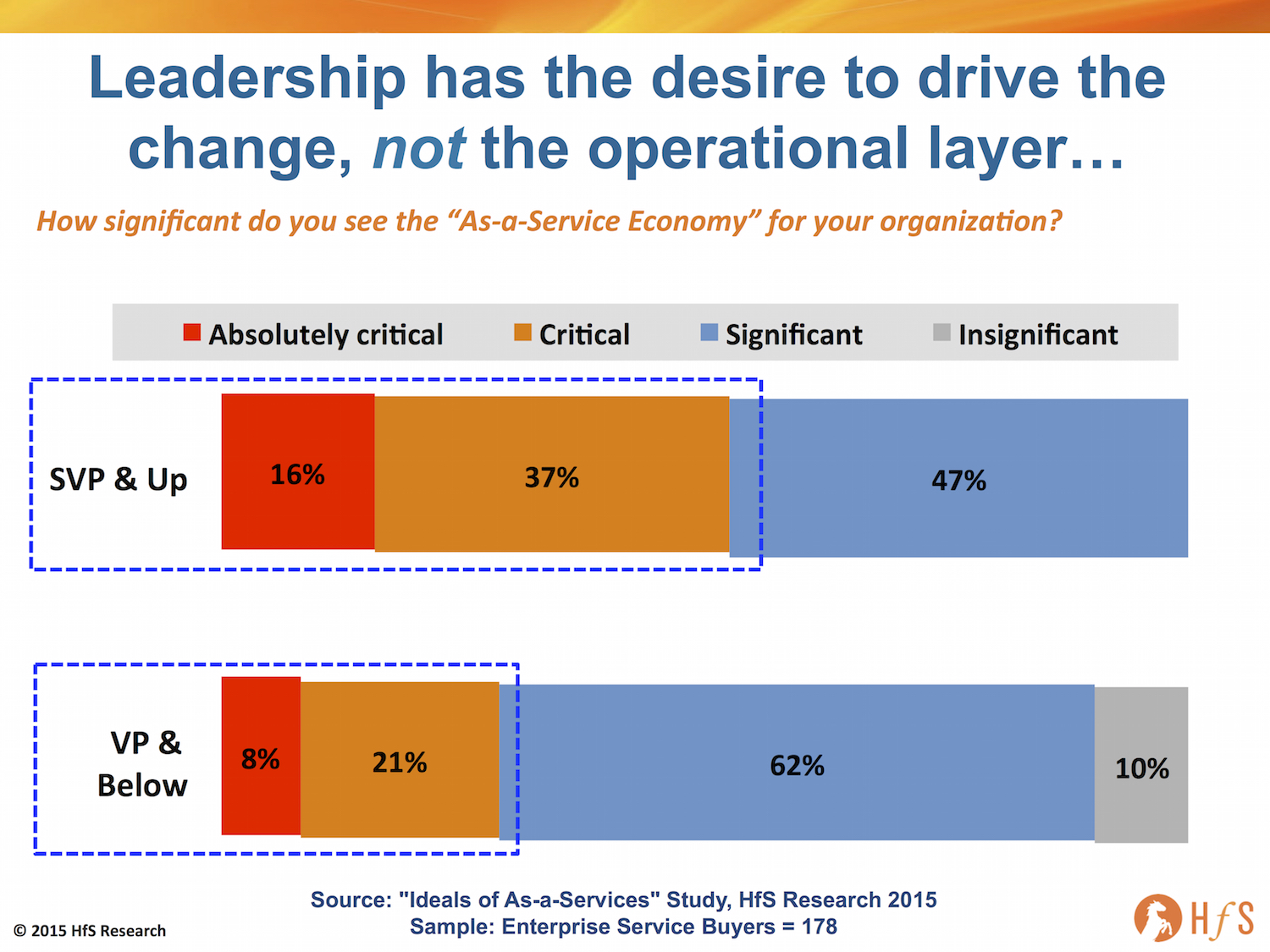

Our brand new study that delves into the Ideals of As-a-Service (stay tuned for the full release very soon) reveals some startling home truths as to what’s likely coming next. My biggest fear in our the industry is for those people just sitting around literally waiting for change, as opposed to squaring up to the commoditization and automation of legacy processes to provide their firms with new ideas, new ways of doing things and adding value, beyond simply keeping the operational lights on.

One alarming trend coming out of this new study, which covers the dynamics and viewpoints of more than 700 industry stakeholders, is the delta between the desire to change the model from business leaders (SVPs and above) and their middle-managers and below:

Click to Enlarge

The middle layers and down need to step up – or step out – of the picture

Why is it that over half of senior managers view As-a-Service dynamics as critical, while only 29% of their teams under then feel the same? Answer – most people are comfortable with their daily grind – they stare at metrics on spreadsheets, ensure exceptions are handled and the corporate engine keeps running. They turn up at meetings and say all the right things, avoid challenging the status quo (while acknowledging there can always be improvement), but deep down have settled for adequacy and a steady treadmill drumbeat of efficiency without too many fireworks or drama.

Why would they want to learn how to collect and interpret data more intelligently? Why would they want to find problems, as opposed to solving them when they crop up? Why would they want to mimic manual processes into scripts to have them run robotically, when they can patch over these inefficiencies with cheap offshore labor? Why would they want to explore the potential of artificial intelligence and self-learning computing capability when they can just do these things themselves (or at least pretend to do them). Answer – they have no burning platform to change the way their do their jobs.

But there is one significant burning platform that will burn them, if they are not willing to adapt to the As-a-Service world: they will be irrlevent in tomorrow’s corporation. Yes, they may be lucky and survive in legacy organizations that can get away without changing, or they may be in their late 50’s and only care about lasting a few more years until retirement, but – for most – if they cannot adapt to As-a-Service, their bosses will shift them on and either replace them with a service provider staffer, or just simply phase out their legacy job, as it was not really needed anymore.

The As-a-Service Economy is forcing a shift from Efficiency to Capability

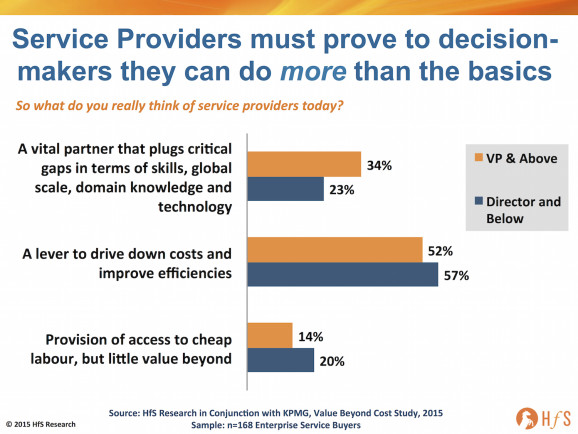

It’s true, in many cases, that service providers are not providing much more than basic operational offshore-centric delivery, however, that’s usually because that is all these clients intended to receive, when they ventured into using external services to drive out cost – and the reason why they selected service providers to provide operational efficiency, as opposed to plugging critical capability gaps.

We all know the initial benefits behind outsourcing quickly become forgotten as the C-Suite turns to its operational leaders to demand continual productivity gains and value, however, the motivations from leadership are not changing, more the means by which to satisfy the C-Suite’s insatiable thirst for running the enterprise as cost-effectively as possible. And this is the very essence of the As-a-Service Economy; finding new ways and means to run businesses as efficiently, intelligently and flexibly as possible.

However, while a company’s leadership is always biting at the heels of its operational leadership to keep driving out the cost, the resistance coming from the middle layers and down is clearly becoming a pressure point as enterprises realize they have to go through a more radical, painful period of transition as the As-a-Service Economy slowly becomes a reality.

As research we conducted earlier this year clearly demonstrates, well over half of enterprises, today, only view providers as brokers of Efficiency as opposed to Capability:

Click to Enlarge

The good news for service providers, is a very small proportion today views them negatively as low cost body shops (this would have been a lot higher just a few short years ago), however, most are stuck in this middle ground, where their clients only want and – expect – a service designed to scale their operations and help them be more cost efficient. However, a third of the more senior managers (VPs and above) do view service providers as genuine capability partners – and that’s actually pretty good, provided the right providers can figure out how to work more with these senior people to explore value-driven relationships.

So… two things need to happen to move the needle away from stagnation:

1) Service providers seeking to deliver genuine value beyond cost need to have a more intense dialog with that growing proportion of senior service buyers who view them that way;

2) Service buyers need to recognize this genuine burning platform to shift gears from Efficiency to Capability.

The Bottom-line: We owe it to our delivery staff to give them the hard truths – the platform is already smoldering, even if they can’t yet smell the smoke

The changes coming to our world are significant – and not dissimilar to when coal mines were displaced by nuclear power plants, when car plants which used to employ 5000 people now only need 300 etc. Operations are becoming standardized, cloudified and robotized – and if we can’t reorient our staff to accept this reality and expand their capability horizons, many will be waiting tables, driving ubers or cutting hair before we know it. We don’t need a burning platform to drive this change as it’s already on fire – many of us simply haven’t yet realized it…

Stay tuned for our final part where we discuss the impact of technology on knowledge-workers…

We’ve been talking about the great divide between consulting and outsourcing models for decades, but – finally – it’s time for the two to get much closer together as the forces of the As-a-Service Economy combine to weld the two models into a new services mongrel which combines simplicity, efficiency and capability for enterprises finally attempting to drag themselves away from their perpetual treadmill of obsolete technologies and valueless process flows.

We’ve been talking about the great divide between consulting and outsourcing models for decades, but – finally – it’s time for the two to get much closer together as the forces of the As-a-Service Economy combine to weld the two models into a new services mongrel which combines simplicity, efficiency and capability for enterprises finally attempting to drag themselves away from their perpetual treadmill of obsolete technologies and valueless process flows.