A raft of luminaries ranging from Stephen Hawking and Steve Wozniak to the figureheads of Artificial Intelligence (AI) at Facebook and Google, Yann LeCun and Demis Hassabis, have signed a petition warning of a “military artificial intelligence arms race” and calling for a ban on “offensive autonomous weapons.”

Meanwhile, among the developer community, the discussion on the ethics and ramifications of AI has been as intense as it has been far reaching. Yet in the discussions around the notions of RPA and process automation, the issue of ethics and the impact on the future of work are (still) largely absent.

A dichotomy of ethics is in play: Outsourcing is viewed as somewhat evil, while labor elimination via technology is barely an afterthought

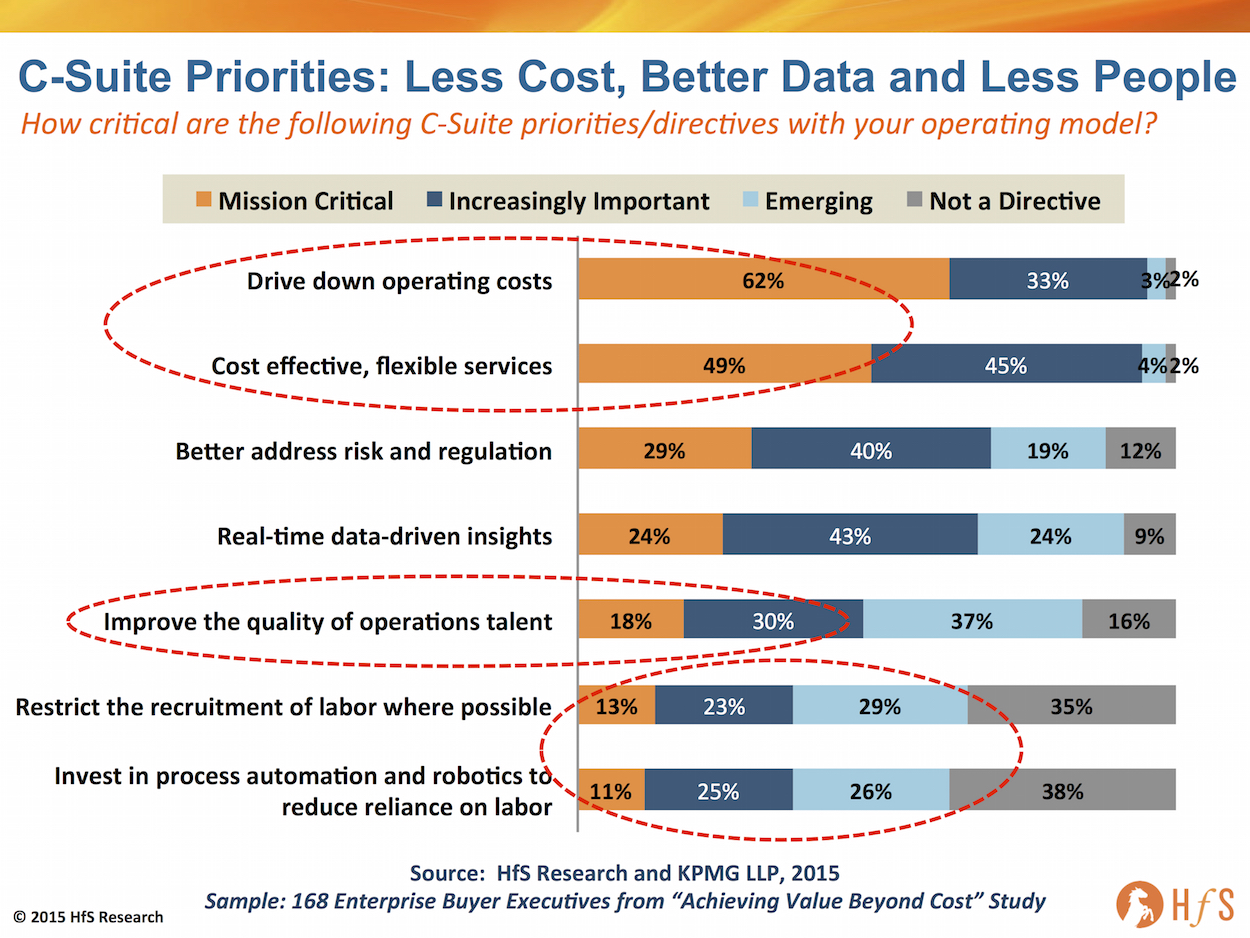

One main observation we, at HfS, are beginning to notice is that many enterprise clients are showing an increasing willingness to invest in technology-based (rather than people-based) solutions. You only have to revisit our Value Beyond Cost study, which we ran with KPMG earlier this year, where we asked 168 senior executives about the priorities of their C-Suites with their operations:

Click to Enlarge

What is startlingly apparent here, beyond the fact that well over 90% of C-Suite directives are obsessed with cost and flexible services as operational priorities, is that less than half (48%) view improving their operational talent as important, 65% are exploring efforts to restrict the recruitment of labor where possible, and 62% are looking, with varying levels of interest, at automation and robotics with the specific purpose of reducing their reliance on labor. The bottom line here is very clear—C-Suites are caring less and less about their people, and more and more about their services.

The big question many enterprises are facing now is not whether to invest heavily in their people. Rather, it is whether to invest in technology to replace staff or use outsourcing partners to reduce the burden of inhouse staffing cost, while improving their access to flexible services. Many enterprises are exploring a combination of the two, or merely leveraging an outsourcer which is using robotics on itself and is willing to pass on the benefits to its clients desperate to move from a legacy labor-centric operational infrastructure.

Suffice it to say, within the context of process automation, the arguments are contingent on the points of view as to the validity of the various approaches and on the assessment on timelines for reaching maturity. Ananth Krishnan, CTO of TCS, offered food for thought at a recent conference where he outlined that in 5 to 10 years’ time we need HR policies for (software) robots. Despite the mainstream narrative that—through the implementation of RPA robots will replace FTEs—Krishnan’s argument was decidedly more thoughtful. In the medium term, future software robots will be a blended reality in the back-office. Therefore, HR policies among other issues need to proactively deal with this development. And crucially, he has started to engage with this stakeholders around these challenges.

While in the context of RPA and Autonomics, the narrative is maturing and we appear to be moving toward emphasizing transformation over simplistic arguments of replacing FTEs, we urgently need to follow the broader developer community and discuss the implications of these approaches. Whether we call it “ethics” or something else is largely semantics. What is completely lacking is how these approaches will impact the future of work.

The Bottom-line: We need to talk more openly about the future governance of artificially intelligent environments

Robotics vendors and service providers need to engage with clients around how all these disruptive approaches will affect talent management as well as organizational structures. Even without apocalyptic scenarios, many job functions are likely to either disappear or be significantly diminished. Equally, we need to talk about governance of these new environments, touching upon ethical but also practical issues. This is not only a necessity for the broader adoption, but also offers high value opportunities.

You can download the POV on this topic, authored by HfS analysts Tom Reuner and Phil Fersht, here.

John Haworth is Chairman of the HfS Sourcing Executive Council (Click for bio)

So what do you do after a rollercoaster career working in ERP software, HR services, sourcing advisory and finally the BPO lead for one of the largest healthcare insurers?

Where do you next take a career, which was centered on traditional services and outsourcing, when all you want to do is challenge the old model and bludgeon a path towards the new?

Of course, you already knew the answer… come to HfS and make some serious trouble.

John has been intimately involved with the HfS community for several year as a service buyer and has long talked to me about his desire to “saw off the legacy”. So when we reached the size and need to have a dedicated leader of the buyer rebels, armed and ready to hive off the turgid, valueless detritus of yesteryear’s transaction-dom, there was noone better to ask to fill the spot. And he loves it so much he’s already written more research pieces than the analyst team in his first month on the job.

So let’s find out a bit more about John’s plans for the HfS buyers council and a little about himself too…

Phil Fersht (CEO, HfS): Good afternoon John! You took the decision recently to join us at HfS Research and we’ll talk about that in a minute, but first could you could give us a bit of your own background?

John Haworth,Chairman of the HfS Sourcing Executive Council: Like a lot of people I think I’m in this industry somewhat by accident. The reason it wasn’t by design is because to some degree the industry as we know it didn’t exist, so there wasn’t anything for anyone to aspire to become part of. I think if you go back twenty years you’ll find strong BPO examples starting to show up. But the seeds had been planted in this industry before that, largely by ITO players and “service bureaus” like ADP or the Sabre reservation system, for example. There has been time sharing in the IT world for a long time, but moving business processes outside of the walls of companies became a rather noble ideal; and I happened to be around when I think some of the very first examples of that were playing out. When I was the co-founder of the HR outsourcing business at Fidelity, there was not a lot of company in the market, and we were essentially inventing a category, including broad HRO—payroll, benefits, HRMS, talent, etc. There was not a lot of company in the market at that time in the other BPO categories, Accenture being the most developed.

We actually co-branded an offering that we put in the market that was one part business process from Accenture and one part Fidelity’s capabilities in HR systems for defined benefit and defined contribution plans. We were ahead of the market in that, but I think we both took away from each other what could be learned at that phase of the industry’s development. As I said, this was about 20 years ago by now, so, by now, we all have lots of experience. We could not have imagined how broad and deep this model has become.

I’ve had the good fortune of being in a position where all of the aspects of the business become a career for me, because I’ve kept it interesting by moving from the sell-side to the buy-side and then as an advisor in-between. I’ll tell you, this is one way to continually learn and also develop a much deeper appreciation for what the realities are on the other side of the table, which I think is incredibly important to the industry in order to advance its overall success. It is, after all, a model of trust and faith in the other party to live up to commitments. Until you have sat in the other seat I don’t think you truly appreciate what can and cannot be moved in any given deal, or in any given business model.

Phil: So what made you decide to join a company like HfS at this point in your career?

John: I’d say two things. One, it’s the right time in my career to take a step back and reflect about not only where the industry has been, and two, to participate in a positive way with where this blossoming industry is going.

I think it’s an exciting time right now, as we’re seeing the rise of truly global markets in labor, in intellectual property and in the supply chain of services, sort of broadly defined. If you combine that trend toward the ubiquity of connectivity and computing power, with the ability to add value at the individual and small organization level, you see that we may be on the verge of something quite big. This could be a very great opportunity area for companies around the globe to be born and prosper in a very short time. So it’s a very interesting time to step back and be more of an advisor, to address this latest and largest wave with the insights born of the experiences that I gained over time.

To help anticipate where the challenges might arise and what we can do about them is a service that those of us that serve as researchers and advisors can continue to do in favor of this industry. It’s always fun to be involved on the leading edge things, and that’s why HfS was attractive to me. Because I’ve identified with the mission of HfS since it was born on the web and as blog, and I’ve seen the impact of community on both understanding the market more completely, and now even helping to shape its next phases. Why? Because 100,000 people thinking generally around the same subjects are a lot smarter than any one person or any group of people usually are. No one has a monopoly on this kind of knowledge—but to be able to participate and guide this explosion at the source, where a lot of people are thinking original thoughts and having similar insights, is something that HfS is accomplishing. And I believe this is the way that we are really going to propel knowledge forward, in the world of the future. Crowd-sourced genius, if you will.

Phil: John, you’ve taken on the role of Chairman of the Sourcing Executive Council at HfS, representing the service buyers in our global community. With the big event coming up in Harvard Square at the end of the year, can you give us some flavor about the theme and what we can expect?

John: I’d say that one of the biggest things we’d like to do right now is establish the buy-side of the HFS community, as a more far-sighted, collaborative, and motivated group. We want to bring out and respond to buy-side leaders who have largely kept to themselves, lacking a forum and the trust factor that our community has been able to develop. I think a lot of corporate people have had private thoughts about this industry, but if HfS can convene these people and help to draw out what’s really on their minds, what’s working, what isn’t, what’s troubling, what the future needs to look like—this would be of great value to service providers and industry innovators.

In our events, we usually succeed in focusing our buy- and sell-side leaders—also advisors—on a very important topic area that really hasn’t been developed very deeply elsewhere. So the December event (Defining and Realizing Business Outcomes: HfS Working Summit for Service Buyers) is meant to crystallize our current concern (as-a-service and its broad implications) before a room filled with some of the smartest people that we can assemble—and the nicest people as well, I would add—who are community-minded and would really like to take this industry to the next step. We will all be focused on this question: How do we deliver business outcomes to the corporate buyers, in a way that keeps the industry healthy and evolving? In this time of rapid change—and even radical change—how do we fairly balance out the views that we get from sell-side, buy-side, and the concerned intermediaries? HfS events have proven to be a unique and valuable forum for sincere participants who are full of ideas and full of valuable experience. We intend to build on that tradition with more events, and more challenging topics. Harvard Square from December 1 -2, 2015 is the kick-off for this new emphasis.

We will be about outcomes. This will come from coupling the real world experience on the buy-side, with what it’s like to actually operationalize some of the available leading edge technologies and innovations. We will explore how to fairly price some of these things. It is all part of creating workable outcomes—I think that buy-side people really need to have a rallying point to come up with a kind of jointly articulated set of agreed upon norms, and agreed-upon beliefs, at least for the near term, about what’s really needed versus what might be on offer from the sell-side. It’s all about market efficiency at the end of the day, and that’s to the degree this market becomes efficient it will continue to prosper. These are the outcomes that we aspire to and that can only occur in the atmosphere of trust and collaboration that characterize HfS events.

Phil: How would you, John, compare the dialogue that we’re having today to when we started doing these buyer summits four years’ ago?

John: Phil, I think outwardly some of the questions look the same, and perhaps they always will. How do we deliver value? How do we develop trust? What are the mechanisms that we use to advance the aspirations of both sides? Those are, let’s say, contracting norms, contracting approaches. Some of that looks the same and some of the ideas look the same. What’s changed, what’s new and different I think is this technology explosion we are living through, and the continual rise of social, mobile, and cloud-based apps and services. The sophistication of the technical environment that everybody lives in, is just sweeping through everything and it’s changing everything. It’s turned the outsourcing model into something that is forced to change, but in ways that I think that HfS has characterized as the emerging As-a-Service economy. We have been leading the way in understanding implications of the merger of new technology with the old-line outsourcing service ethos.

Today, what was formerly called outsourcing is largely migrating to the As-a-Service model, which combines social, mobile, cloud, intelligent applications with processing and support workforces that enable the new outsourcing model. That’s where outsourcing has gone and that’s where outsourcing is going to continue to go. This is a shift that I think we all recognize, and while some of topics we address outwardly look the similar to those in prior years, the context in which these things are happening has changed drastically. Our expectations of outsourcing have to change as well. So I think this is very exciting time to be convening the buy and sell-side in a way that, to my knowledge, nobody else is doing in the market.

Phil: Tell us a bit about some of the exciting presentations we got to look forward too, particularly the Keynote that you’ve arranged for us, John.

John: Because we’re having an event in Harvard Square, where HfS is headquartered, and a lot of us have been associated with the Harvard and MIT environments over the years, we thought it would be a good idea to try to ground some of what we’re doing at least with a smattering of an orientation coming from the Harvard Business School! We’re delighted to have Dr. Francesca Gino as our Keynote speaker. Dr. Gino is of special interest to us because her specialty is negotiation, especially in the psychology of negotiation. If you break down what I said earlier about where we are as an industry, and how we need to collaborate in order to create satisfactory business outcomes in an environment that is radically changing on both sides, it is clear that progress will demand evolved negotiations between buyers and sellers. These will probably look different than the relationships that existed in the past and the negotiations that existed in the past.

So bringing our conference attendees into the presence of someone who’s thought deeply about the psychology on both sides of the table, and what it takes to really understand each other and make progress, something that seems very apt to us. We’re delighted to have Dr. Gino open our event and establish the tone for what we hope will be the new era and the sort of crowning glory of the HfS “insight machine.”

Phil: The crowning glory! Absolutely love it! Good. So, any final thoughts from you, John, as we hurtle towards the end of the year, and some of the things we can expect to from some of the thought leadership that you’re going to be providing?

John: I think, Phil, one of the things that I’d really like to do is, as I was suggesting earlier, give voice to the buy-side in a way that isn’t my voice, but it is a collective voice that starts to be actionable and useful to the sell-side. So that we’re not wasting cycles, wasting each other’s time. I think what emerges as the sine qua non of the world of the future, if you will, is that change happens and it happens very quickly. So there is an opportunity for us to make the market more efficient. We can make sure that that the sell-side isn’t making errors with their offerings and that the buy-side isn’t buying things that aren’t real, or that don’t matter or that will lead them down the wrong path.

We’re doing a real service to the industry to the degree that we can inform the industry and help them make smarter decisions faster in this dynamic environment. The entire industry—both buy- and sell-side—has to deal with the doubling time, if you will, of change in the environment. We will deliver the real service to the market, which has always been the goal of HfS, if we can help the industry as a whole make better choices, faster. I think we really want to rise to the occasion here and be the one research and analysis firm that is aspiring to do this and it is actually able to do this because of the methodology that we perfected, our strong community, and our collaborative events. I think that is going to be where the better answers are coming from.

Phil: Good stuff. We’re excited to have you on board John, and I think as the excitement grows towards the event at the end of the year and the ones beyond that. Will be hearing a lot more from you. So thanks very much for your time today.

Infosys CEO Vishal Sikka talks to HfS on his first year in charge

So… one year into the new job and Infosys’ Vishal Sikka has managed to perform a task noone thought possible. He’s dragged a once-famous Indian-heritage IT services firm – kicking and screaming – out of a maddening tailspin into that dark sinkhole of legacy-ness that is scaring the life out of today’s services industry.

The reason for this is quite simple – he never brought with him a baggage of legacy services culture, where the common practice is to:

1) Copy what all your competitors are saying and try to out-bullsh*t them;

2) Hire cheaper, younger staff and gut the middle layer;

3) Sugar-coat every ADM, Infra and BPO renewal with terms like “digital”, “transformation”, “automation” and “outcomes” etc., when none of these things were really included in the actual contract, but made nice additions to the press release.

Vishal just gets to the point with a refreshing and honest perspective about what his firm needs to do – and is already making shrewd investments in critical areas, such as Panaya (automation) and Skava (digital). He’s also been growing the traditional business, with Infosys just reporting its best quarterly revenue growth for 15 months (4.5% year-on-year), and overseeing several new $2Bn+ sized engagement wins in the last 12 months, with the likes of Allied Irish Bank, Deutsche Bank, NSW State Government and ICA Gruppen in the last 12 months).

The business is stable, growing well again in an industry where many competitors are scrambling all

over the place trying to find renewed direction and focus. What’s more, the management bleeding has stopped and there is a distinct new energy and passion around the place from everyone you meet.

However, where Vishal is really impacting the culture of Infosys is by driving a renewed culture, based on his Design Thinking principles, that is exciting his staff. Design Thinking is real – it’s something delivery staff, account managers and senior executives can all relate to, understand and embrace. Rather than confuse the living daylights out of people, he talks about real business challenges and how they need to be addressed. And this coming from a guy who has a Phd in Artificial Intelligence… talking real business issues to real people is quite the achievement. So we caught up with Vishal is his Silicon Valley start up-esque collaboration offices in Palo Also to hear first-hand his year one Infosys experience, and where he wants to take things next…

Phil Fersht (CEO, HfS): Vishal, it’s good to be with you here at Infosys. You’ve been CEO now for about a year, so I thought it would be a good time to check in. HfS has done a considerable amount of research into Design Thinking and how it aligns with services outcomes. Can you bring me up to speed on how Infosys is faring, with your own brand of Design Thinking?

Vishal Sikka, CEO and MD, Infosys: Thanks, Phil. It’s great having you here. We started teaching Design Thinking at Infosys back in October of last year. We brought some of our trainers here to the Institute of Design at Stanford—the d.school. Then members of the d.school faculty went to our corporate university in Mysore and started training our people.

When I say training—this is not like some guy watching a video on Design Thinking. These are one or two-day immersive sessions, where people are hands-on and actually build things. As much as possible we try to get the d.school faculty directly involved. This class has now been taken by 36,000 employees. I’m told this is by far the largest rollout of Design Thinking education in history. The d.school said this is like many times the total number of students that have taken the course at Stanford. I don’t know what the exact number, but 36,000 is just insane.

So it is not a center of excellence, where you have three, four people who understand Design Thinking. This is 36,000 employees of the company who understand what it is and practice it.

We are now creating customized training for project managers in our delivery organization. 22,000 of our 36,000 people are in delivery, and 3,000 are project managers in delivery. So we’re creating a special program for project managers to be able to bring Design Thinking into the ongoing work that they do. So in my view we are by far the biggest adopter.

Design Thinking is happening with clients, too. This morning before you came in here, we were doing some Design Thinking work with the German utility. We’ve had about 36 or 37 customers for workshops here in our Palo Alto office in the last nine months, and of course others around the world. In fact, I would have liked for you to meet Sanjay Rajagopalan who heads up our Design and Research team, but he is doing Design Thinking workshops with clients in Australia this week. We have a pipeline of 100 clients interested to do this.

These workshops are not focused on best practices. When we think about “best practices,” hidden behind that phrase is the reality that this stuff is already known. Known problems are really yesterday’s.

But then there are things in life that are unknown. So how do you go after the unknown?

We had a very, very large consumer products company here, which among other things is very famous for chocolate, and we talked about how to deal with the demonization of sugar. There isn’t a demonization of sugar package available for SAP or from Salesforce.com. There isn’t a best practice sitting there somewhere. You have to think about this.

All our lives our education system teaches to do problem solving. Nobody teaches us problem finding.

And Design Thinking is a methodology for problem finding. So that is how we see it.

Phil: So you’ve done this all in a year?

Vishal: Nine months, actually!

This space (pointing to the colorful Palo Alto office which sports writable walls and modular works spaces) and all the new spaces that we are building, they are all designed like this. These are design spaces. These are flexible. In the Bay Area, we have 3,000 people working at various clients. And we had a long conference call about Zero Distance on Monday night. This whole area was opened up and all those tables were moved here, people were working from this corner and there were a 100 people in that area. We had a giant video conference in there.

Phil: Can you talk a little about “Zero Distance”, Vishal?

Vishal: Zero Distance is about innovation. Innovators aim to maximize their relevance by reducing the distance to the user, to code, to value. I have asked everyone at Infosys to focus on getting to Zero Distance, and bring innovation to every ongoing project.

For example, Abdul Razack has a team that is doing IIP, the Infosys Information platform, which is based on Hadoop. Abdul shared with me yesterday some incredible things that they have achieved on open source technology, solving some extreme analytical problems. We have the Infosys Edge team doing new product development. And we have many teams that are doing innovative things. And they will continue to do their thing and bring breakthroughs to life.

But if innovation is done in these small pockets—like in Abdul’s team, Sanjay’s team or Sudip’s team—we’ve missed the point of innovation. Innovation has to come from everybody. It has to come everywhere. And this is why I say, “The Innovation Department in Infosys is Infosys.”

Right now we have 8,500 master projects that are going on in the company. This is the lifeblood of the company. Infosys at the end is a project company. So these 8,500 projects represent the work that we do. And we started this program to basically bring innovation to all 8,500 projects. The 8,500 projects break down into 35,000 sub-projects.

I made a straightforward five-point template about how to bring innovation to every project. And it has just taken off virally. And we do these sessions with teams where we share some amazing thing that our team did. And customers are already starting to see that.

Phil: So when you look at everything you’ve achieved in Design Thinking so far, what would you say is the critical ingredient to finding what’s not there?

Vishal: First of all, you have to have the desire—the instinct—to look for it.

I did a survey when we crossed 25,000 Design Thinking-trained members of the Infosys team. I knew at that point that this was a big moment. When we hit 25,000, roughly 12,500 were freshers—young minds just out of college. And 12,500 were the senior folks.

It was astonishing to see the spreadsheet. I was reading this thing and I was just moved. Of course one thing that was shocking was they had put this in two tabs, the freshers and non-freshers. And the older folks, their responses were always three or four lines long. And the one’s from the freshers were terse—less than one line long. Like text messages.

But the sentiment is exactly the same. There were only three questions. How do you bring Design Thinking to your work now? What has it changed, etc.? The answers from the senior folks, said it had opened up their creativity: “It is like I have seen the light, it is like I can think again. I forgot that I had a brain,” stuff like that. Amazing responses.

One fresher wrote that he went and fixed his mother’s sofa because he had done Design Thinking and because the sofa was broken. And he said, “Let me think about how can I fix the sofa.” I was reading that thing and I said, My God! It was astonishing: this is actually changing not just how people work, but how they live.

Of course it is too early to know what all this means. In the last two months, we met a few clients who tell me that there is something going on. One of the huge banks on the East Coast told me that suddenly because of the Zero Distance thing, innovation is inserted into every project. They said that it appears that the quality of work has just gone up.

We are also by the way bringing Design Thinking to our RFP process. Every response that goes to an RFP of more than $50 million now goes through this team.

Our HR team works like this. They redesigned our performance process. We just finished our promotions and they went through this thing. So it is everywhere.

It is very early, but the result of all this will be quite fundamental I believe.

Phil: So clearly, Vishal, this is having an impact on Infosys. Do you think this will have a ripple effect on a lot of the other Indian-heritage service providers?

Vishal: It will have to, it will have to. I think it is inevitable, because this thing about problem finding and problem solving, I personally went through this when I first came to Stanford.

Even though I had gone to Syracuse for my Bachelor’s degree, I still had grown up in India and was trained to do what I was told. So when I came to Stanford and I went to my advisor, and I asked him, “What do you want me to work on?” And he said, “I have no idea.” And it was a shock to me, so I said, “What do you mean? What will my PhD be on?” He said, “You figure it out.” And I told him, “No, you are supposed to tell me what problem I work on and I am supposed to work on that.” He said, “No, if this is what you thought then this is not the right place for you. You are supposed to find your own problem, we are supposed to tell if the problem is good enough or not. Then you solve that problem and then we tell you if the solution is good enough or not. This is how it works and if this is not what you thought, then you are in the wrong place.” He said this to me bluntly within one month of coming to Stanford.

And I thought they had a catalog of open problems and I would work on one of these. So that really put me into a tailspin.

Narinder Singh was a research associate there and he told me, “Yeah, people spend years looking for a problem.” He said, “Remember that guy Andrew?” Andrew was in the seventh year at the time. He said, “He still doesn’t know what his topic is going to be.” I said, “What the hell has he done for seven years?” Turns out this happens all the time. Either you luck into it and you find one right way or sometimes you spend years finding it.

So then I saw a talk by John McCarthy, the father of AI. And in that talk he made a very interesting statement. He said, “Articulating problem is half the solution.” So I talked to him after his lecture. I said, “What did you mean by that?”

He explained. He said, “Look, you know, most of the time we don’t articulate the problem right. And he was talking about it in the context of AI search. He said that when you frame the problem right, you have basically an idea of how the solution is going to work. I though this was very interesting.

And I talked to Bob Floyd who was another professor in Computer Science, also an A.M. Turing Award winner. He wrote the Floyd algorithm for graph traversal. So Bob Floyd told me that, “Oh, that is not enough.” I said, “This is what McCarthy just said—that articulating a problem is not the solution.” He said, “Of course, he’s absolutely right but it is not enough. I articulate the problem, I solve it, then I go back to see if I can rephrase the problem now that I have solved it. Then I re-solve it. And then I go back and rephrase it until I can no longer improve the solution. That is when I know that I have found a beautiful solution.”

I realized that there is so much to this problem finding, problem solving thing that I never thought about. In those days I read the books by George Polya, called How To Solve It. And actually Floyd’s algorithm that Bob Floyd wrote, was his seventh attempt of solving the same problem.

As an Indian kid, who grew up dutifully doing what I was told, this was my introduction to opening up your mind to see.

And here’s how I found my problem. I found it within a year.

Somebody told me to look at what interests you, what excites you. And I was reading many PhD theses that I found interesting. I quickly realized that at the end of the PhD thesis, people will write about the things that they left unfinished. I was reading Karen Myers’ PhD thesis and she wrote three things that her approach could not do. And I thought that this was something interesting. I was very excited by her area anyway, which is why I had read her whole thesis. When I saw those three problems, I went and I talked to my advisor and I said, “I want to solve these, I want to find an approach that doesn’t have this three problems.” He thought it was a good idea. That is how I came to my PhD thesis, based on the weakness of Karen’s approach. And one of the projects that was a part of my PhD work was Center For Design Research in Stanford.—the precursor to the d.school.

It was a part of the mechanical engineering program, and Mark Cutkosky was the professor there. He used to collaborate with my PhD advisor, and we did a bunch of projects. One of the projects we worked on in 1992 was called Design World, which was about how do you design things. So that is how I got into this whole thing. And I brought into wherever I could.

So you see I had been through this experience of problem finding and its importance myself. As important as it is to see what is there, it is as much or more important to see what is not there. This is why we’re doing what we are doing.

Phil: Vishal, thanks for sharing your current views with our readers – am sure many will appreciate them!

If I have to read another article about Uber’s disruptive business model, I think I am going to defect to a Trappist monastery and brew very strong beer for the rest of my life…

However, iet’s be honest here – who really cares about these taxi drivers being forced to improve their services, clean their cabs, clean themselves, start using credit card machines and even (on occasion) help you with your bags? The fact is, unless you are a legacy taxi driver, or related to one, you’re most likely delighted they are being forced to get competitive and improve their services.

It’s the same with Spotify / Google music – unless you are in the business of selling music, most people are ecstatic they can now get all the music they desire for $10 a month or less, without having to spend a fortune on CDs, with the hope that there’s the odd good tune. And there’s Amazon versus Best Buy, there’s Airbnb versus Marriott, there’s Netflix versus Comcast, and so on. Moving to our industry, there’s Onesource Virtual versus NGA, there’s ZenPayroll versus ADP, Workday versus SAP, there’s software versus people, there’s offshore people versus onshore people, there are robotically automated solutions versus people, there are self-learning machines versus people, in fact, every advancement in services we look at today is all centered on less people… and delivered As-a-Service.

And like the happy world of taxi customers now getting a better and cheaper service for their money, there are many business leaders who are only too happy to get cheaper and better business operations, because they can reduce their reliance on people. If you’re not an employee who is being replaced by a piece of software (although it’s widely assumed we will be someday), the chances are you’re happy your firm is becoming more profitable and doesn’t need to rely on so many bodies to keep the lights on. Just revisit our Value Beyond Cost study we ran with KPMG earlier this year, where we asked 168 senior executives about the priorities of their C-Suites with their operations:

Click to Enlarge

What is startlingly apparent here, beyond the fact that well over 90% of C-Suite directives are obsessed with cost and flexible services as operational priorities, is that less than half (48%) view improving their operational talent as important, 65% are exploring efforts to restrict the recruitment of labor where possible, and 62% are looking, with varying levels of interest, at automation and robotics with the specific purpose of reducing their reliance on labor. The bottom line here is very clear – C-Suites are caring less and less about their people, and more and more about their services.

The big question many are facing now isn’t whether to invest heavily in their people – it’s whether to invest in technology to replace staff, or use outsourcing partners to reduce the burden of inhouse staffing cost, while improving their access to flexible services. Or use a combination of the two… or use an outsourcer which is using robotics on itself and is willing to pass on the benefits to its clients desperate to move from a legacy labor-centric operational infrastructure.

The Bottom-line: In the The As-a-Service Economy, we only care about achieving our desired outcomes

Here’s the nub of the argument, while people like Hillary Clinton want to turn back the clock and protect the legacy job-for-life, the vast majority of people really do not care that labor forces are being disrupted, along with legacy business models and obsolete practices. Today’s world is all about faster, cheaper, more accessible services – and to hell with any obsolete process, system or person which gets in the way of convenient and affordable As-a-Service models.

People care most about enjoying the outcomes of what they pay for, not the efforts made to achieve those outcomes. Expenditure on services is increasingly related directly to outcomes, not a fixed tax we have to pay for a standard service. Personally, I always pay a limo driver $10 over the norm to drive me to the airport. He picks me up in a Cadillac, hangs up my suit, gives me a bottle of water and a newspaper – and only makes conversation if I want to. My desired outcome is a relaxing journey and the extra cost is worth it – and he wins my business everytime and I refer him to all my friends and colleagues. Now that’s one way to win over the Ubers of this world – people will pay when the outcome is what they want. Welcome to the uncaring economy where is all about the outcome…

And this isn’t some traditional HRO play, it’s KPMG making a serious investment in Workday delivery across both HR and Finance & Accounting. KPMG already claims to be the transformative partner for 45% of the world’s Workday financials rollouts… now it is playing with the leaders in Workday based HR delivery, namely OneSource Virtual, Deloitte, Accenture, Collaborative Solutions and Meteorix.

Does this mean KPMG is now an HR-as-a-Service Provider?

Yes it does. The firm has realized it has to be in the managed services business to support the emerging SaaS offerings across technology implementation, post go-live support, transaction business processing and higher value services, such as organizational change management, workforce analytics and ad hoc strategy needs… in an on-demand model. It also knows it needs to be in the position to provide these on-demand capabilities around several core HR SaaS product suites, notably Workday, Oracle HCM and, ultimately, SAP Successfactors.

So can KPMG lead the HR-as-a-Service market?

KPMG can certainly compete against the consultative global leaders in HR, most notably Deloitte, Accenture, IBM and Mercer, while also having serious capabilities to spar with the emerging niche service providers, especially where clients have global requirements at scale. With this Towers Watson deal, HfS estimates an additional 150 Workday specialists are being added across United States, United Kingdom, China/Hong Kong, Canada, Singapore, and the Philippines to add to KPMG’s current HR practice of ~600 practitioners across 18 major global countries. This is now a serious global player, which can pivot impressively across both finance and HR domains around the leading SaaS platforms. With this deal, KPMG also assumes ownership of both the famous Towers Watson HR Service Delivery and Technology Survey and Forum, which it can quickly absorb to enhance its own brand credentials and domain leadership in HR-as-a-Service.

The Bottom-line: The ambitious consultants are moving into As-a-Service, so what are the next moves we can expect?

Accenture never veered from being a service provider, in addition to a consultant, and now reaps the rewards for dovetailing the best of both worlds – managed services, global scale and scalable skill. Deloitte, KPMG and PwC have claimed, for the last two decades, to be consultants and audit firms – and not managed services providers (even though Deloitte has always had a few discrete offerings that smell a lot like managed services).

Now, KPMG is moving into As-a-Service delivery, with a particular Workday flavor that is clearly the best starting place with the level of global demand for this offering. The next move will surely be it continuing to build a Finance-as-a-Service capability around the emerging Workday financials management suite that is attracting major interest from CIOs and CFOs.

Accenture and Deloitte will be nervously watching this move, not to mention several traditional HR service providers, such as AONHewitt and NGA, which are trying to figure out where (or whether) they truly belong in this As-a-Service business. Accenture has done an impressive job honing its HR-as-a-Service delivery around Workday and SAP Successfactors (among other SaaS offerings), while Deloitte is still clearly stalling on whether or not it is in the As-a-Service HR business, versus merely being a consultant – and may now be thinking that KPMG is stealing its thunder in the space. Meanwhile, we have a whole host of feisty new-generation As-a-Service providers, such as Aason, OneSource Virtual, Meteorix and Appirio, which are unraveling their gameplans to stay ahead of this evolving space.

Consolidation is going to be the next step for many of these service providers – the brave will stave it off, some will take the exit money while they can, while there will be some legacy players who panic and make a move to stay in the race (remember those awful acquisitions during the HRO 1.0 era?). As-a-Service has arrived, and HR provides the early battleground… so sit back and enjoy the show, as this one could get messy 😉

Like many of you out there, I was floored last night to see Presidential candidate Hillary Clinton openly attack the Sharing Economy in a speech outlining her economic theory.

Clearly taking a swipe at the likes of Uber and Airbnb Mrs Clinton states, “This on-demand or so-called gig economy is creating exciting opportunities and unleashing innovation. But it’s also raising hard questions about workplace protections and what a good job will look like in the future”. Clinton “Vows to crack down on employers who misclassify workers as independent contractors”, which she says is “wage theft”. Along with globalization and automation, Clinton describes the “Sharing Economy” as “conspiring against sustainable wage growth”. The report says “she will argue that policy choices have contributed to the problem, and that she can fix it.”

So why does added protectionism of US workers help offshore and nearshore outsourcing?

While the open attack on innovative business models is in itself mind-boggling, the less obvious impact of her focus here is to discourage service providers and enterprises from hiring US talent to provide business support services. As service delivery becomes increasingly focused on higher value needs, such as organizational design, analytics modeling and supporting complex apps development across multiple environments, the opportunity for local US talent to be leveraged is huge.

In addition, the way in which new generation As-a-Service providers want to engage with talent needs to be more “As-a-Service” to be competitive. Virtual support models are becoming critical for BPaaS support functions where clients need quick, on-tap support, and – in many cases – the new generation of service provider isn’t simply looking to stock up hoards of full time employees in a call center somewhere in the Midwest – they are also seeking to engage talent which prefer a flexi-model and do not demand entitlements such as healthcare, 401K etc. Isn’t that what things like ObamaCare are for? Just look at how the new class of Workday service providers, such as Collaborative Solutions, Meterorix, and OneSource Virtual, all of whom are upending the old guard of “Was-a-Service” providers, clinging to costly legacy models that have already been disrupted. These firms are all employers of local US talent in support of innovative As-a-Service delivery. Does Hillary really want to discourage these firms from flexing up with more staff locally as they grow, or would she prefer them to invest more in India, South America etc where talent is more fungible and flexible to manage? Because that is what will happen if more protectionist employment laws are put through.

Why not make it easy and fluid to hire local talent to scale up – as and when needed? Why not support our service-driven businesses to be more agile and cost-effective with their delivery? Because if services firms and enterprises are being strong-armed into hiring fulltime employees (many of whom don’t even want to be fulltime employees), they are going to evaluate alternative talent models to deliver their services, such as hiring more local people part-time, or outsourcing to service providers which can provide talent from across the globe.

Bottom-line: The US is an increasingly unattractive place to do business. Let’s not make it even worse

For starters, the US has stayed at the lead of the global economy ever since Winston Churchill stuck two fingers in the air because their leadership has embraced innovation in technology and life sciences – and supported their leading firms and academia in the process. Now, rather than staying ahead of the curve and realizing the future of work doesn’t look anything like the past, we are seeing the leading Presidential candidate come down heavily in support of protectionism in order to win a few cheap votes from taxi drivers who overcharge us. Aren’t our wage costs, payroll taxes, healthcare contributions etc already off the scale? Why not give our innovative employers a chance to be successful so they can create new jobs for the future, as opposed to discouraging them from hiring in this country at all? It’s not as if there is a huge unemployment problem in the US these days…

Uber is an easy target for Hillary as it has to rely on local contract workers to be effective and the government can step in to interfere. However, what about all the tech start-ups, As-a-Service providers, major enterprises which can leverage fungible labor from anywhere across the globe to fulfil their needs? Don’t bite off your nose to spite your face Mrs Clinton – protecting a few taxi drivers who overcharge us would have much broader impacts on the attractiveness of US talent at large. Let’s just hope this is a minor aberration as she realizes the consequences of this bewildering campaigning and quickly corrects course to avoid being seen as a dated, legacy politician.

Two CEOs clearly up to no good… Genpact’s Tiger Tyagarajan (left) and Infosys’ Vishal Sikka (right)

One of the great things about HfS is the fact we never partake in gossip or idle speculation. So let’s change “never” to “rarely”…

I was happening to be Uber-ing myself aimlessly around the streets of San Francisco last week when I happened to drop in on Infosys’ sexy new Design Thinking center (I think that’s what they call it) in Palo Alto, where I caught two of the industry’s finest minds having a sneaky cup of coffee.

Now, before you all jump to conclusions that Vishal Sikka and Tiger Tyagarajan are about to join forces, they are actually old friends and neighbors, and this was purely a social call… but it did get me thinking about what if Infosys and Genpact got a little more intimate with each other…

Pros:

Challenging the old way of thinking. Infosys’ fresh Design Thinking approach and Genpact’s re-imagination of business processes are very well aligned. Both firms have jumped on the importance of challenging current thinking and instilling that across their organizations (and not a CoE approach).

IT services meet BPO… on steroids. A great IT services firm meets a great BPO/operations process management firm. This would be a real powerhouse. What’s more, Genpact is the largest “process pureplay” breaking new ground in terms of its sheer scale and size – where it takes the business next, there is no written rule book available.

BPaaS at a global scale? Infosys EdgeVerve + Genpact’s emerging process consulting capability would be very interesting. Scalable BPaaS solutions that could be industrialized at a global level… the mind boggles at the possibilities to realize a long-held industry vision.

Cross-client synergies. Great upsell opportunities across major clients, especially in horizontal process areas where Genpact is market leading, such as finance and accounting solutions or procurement where this combination would create an even stronger challenger to Accenture than they are individually today.

IT autonomics + RPA + AI potential. Interesting combination of automation capability across IT autonomics (Infosys) and robotic process automation (Genpact). Would also be a nice playground for Vishal to put his Ph.D. in artificial intelligence into practice. These two could certainly build a cognitive+autonomics+analytics computing platform that differentiates itself in the market alongside the likes of Watson, Holmes, ignio, Amelia etc.

Digital meets Process. Digital strategies need to bring together real process acumen and technology enablement skills – at scale – in areas such as mobility, analytics and social media/collaboration. The ability to design “digitally-native” end-to-end business processes is core to the future of services and these guys may just be able to pull off something quite special together.

Adds real vertical strength and depth. They would nail insurance and banking in spades, have really strong presence across manufacturing/consumer/retail and Genpact’s life science’s presence would be a fantastic opening for Infosys.

Geographically and culturally. Very interesting spread across India, UK, Central Europe, ANZ and the US. However, still trying to visualize (or is that Vishal-ize) the whole Palo Alto/New York/Gurgaon/Bangalore cultural thing they’d have going on.

Timing. This market is ripe for some aggressive moves to change old habits and shake up the apple cart. This one would certainly set the big cat out loose among the pigeons, when investors are hungry for new ideas, bold moves and aggressive plans. With Vishal enjoying a healthy dose of momentum as he reaches his first anniversary at the helm of Infy, there are worse moves he could make… surely? And this would likely be at a similar size to Capgemini / IGATE…

Fashion. Tiger could clearly show Vishal a thing or two about designer New York business attire, while Vishal could certainly help Tiger get with the West coast tech-nerdy thing.

Cons:

Who would run the show? These are two fiercely proud firms with very strong cultures and very dynamic leaders. Could you really fuse these together?

What methodology would they follow? Would Smart Enterprise Operations win out or would the Process Progression Model lead the way? Come to think of it does that even matter.

Limited time to integrate. In this market, no-one can afford to take their eye off the ball. Prices are at an all-time competitive low, several ambitious providers are eager to “buy” their way into strategic deals to develop out their offerings and maintain market share and there are emerging As-a-Service contenders willing to disrupt the old model with new disruptive approaches.

Doesn’t wholly address the consulting gap. While there is some excellent talent across both firms, this is nothing near the scale of an Accenture, Deloitte, PwC or KPMG on the strategy/consulting side. We would like to see both firms up their consulting talent pools – at scale – as the As-a-Service Economy continues to unravel. While the expertise-as-a-service model emerges, there does need to be the right blend of managed services and consulting acumen to really get ahead in this market.

Big isn’t as beautiful these days. Just looking at the efforts the likes of IBM, HP and CSC have made to make their business more manageable with more clearly defined business units, getting to monster size for the sake of being just bloody huge (and this one would become one of the largest services firms on the planet) is not a reason to do this.

The old IT+BPO thing isn’t washing as well as it used to. Up until recently, the whole talk in the services business was always about IT services firms offering BPO as there were so many great synergies between developing and maintain apps and being able to deliver process solutions. Hey – you not only could you support a legacy ERP platform, but why not milk the dollars processing invoices and paychecks off the back of it? With As-a-Service, that isn’t so appealing. When you can get much of the IT you need in the cloud, the ambitious BPO these days is pushing “Finance-as-Service” or “Revenue-Cycle-as-a-Service, or “Insurance-operations-as-a-Service” as so on… The future isn’t about buying IT services, but more buying a business outcome delivered As-a-Service. If a credible BPO can enable and deliver business services in the cloud, who cares who is developing and supporting the underlying apps… especially when they are standardized?

The Bottom-line: This could be a match-made in Heaven, Palo Alto, Gurgaon or Hell…

It’s fun to speculate, and this one is especially interesting. When we looked at IBM+TCS, there were clear service line synergies, but the cultural gap between those firms is huge – and the sheer sizes involved make this too unappealing for so many stakeholders. However, in this case, Infy (we think) has just about enough cash if it really wanted to take a serious look at G, and there is clearly a closer set of synergies in terms of cultures and less overlap. These are also two ambitious firms who are clearly not ready to rest on their laurels and want to break new ground if they can. They are also led by two popular and visionary guys who are in tune with their people and the market. However, at the end of the day the bankers do the real talking and these may just be too many complexities to make something of these sheer scale and size pay off.

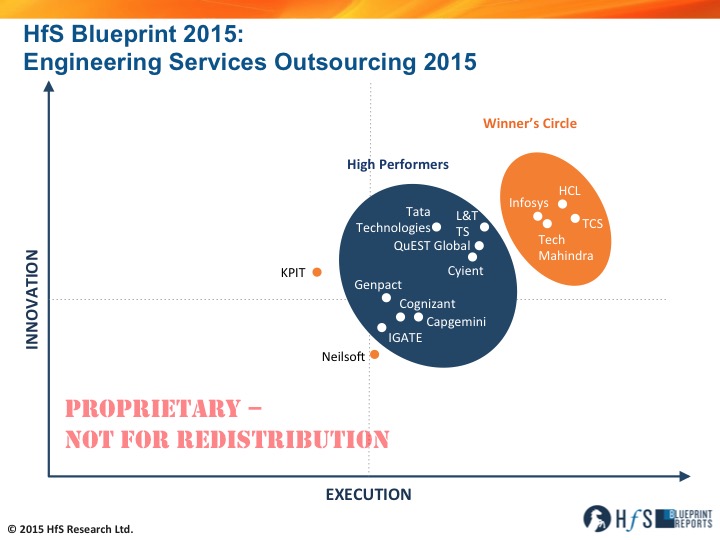

If there’s one market people have been raving about for the past decade – and still are – but has never quite taken off as quickly as many have predicted, it’s the world of engineering services outsourcing.

This market is all about using third parties in the design, analysis, manufacture and augmentation of products. And in today’s world of global labor, the global marketplace, emerging technologies, smarter global sourcing models and the Internet of Things, the potential to embrace outsourcing expertise to bring products to market smarter, faster and cheaper has never been so exciting.

Engineering services has a huge market potential, but – somehow – engineering service providers have had limited success in transforming this potential into the actual outsourcing engagements. Now things are changing, and we believe that engineering services is evolving from a niche offering to the mainstream. So without further ado, let’s hear from HfS Research Director, Pareekh Jain, on the excellent research he’s completed that delved deep this this market:

Click to Enlarge

Pareekh, how do you see this market evolving and what are the key drivers for engineering services?

Engineering services outsourcing, over the last decade, has evolved from simple drawing and drafting to complex end-to-end product design. Now an enterprise which wants to enter a new market segment can partner with some leading engineering service providers, that can not only deliver complete new product design but that can even collaborate with manufacturing partners for additional benefits. Some engineering service providers are also collaborating on high-end R&D projects with the world’s leading research institutions and filing patents both on behalf of their customers and the service provider.

We have observed six key demand-side drivers transforming the engineering services outsourcing market. First, product life cycles are getting shorter which means more product design work and faster time-to-market requirements for enterprises. Second, enterprises are looking to adjacent markets for growth but rather than do it all themselves they are partnering with engineering service providers. Third, enterprises are entering emerging markets and leveraging engineering service providers to do value engineering and to develop frugal versions of the enterprises’ products that can compete at the different price points in these markets. Fourth, the long tail of products created when technology companies merge (and they wish to maintain all existing revenue streams) is increasing the demand for the external help to manage the lifecycle management requirements of legacy or low growth products. Fifth, demand for smart products with the combination of software and hardware is driving enterprises to leverage engineering service providers which have developed expertise over the years across software, hardware and embedded solutions. Sixth, availability of composites and lightweight material is enabling enterprises to rethink the design of their products with the help of engineering service providers.

What was the scope of this Blueprint?

This Blueprint is focused on the product engineering segment of engineering services. The other two segments of engineering services i.e. software engineering and product lifecycle management (PLM) package implementation were excluded, and we will look to cover them in future Blueprints.

How did the Blueprint turn out?

Engineering services is a diverse market spanning across many different verticals and industries. While the value chain element of product development is common across this diversity the skills for designing a car are very different than the skills for designing medical equipment. We analyzed key engineering services outsourcing market dynamics and evaluated the capabilities of 14 service providers at the organizational level, the vertical level, and the service level. We evaluated both specialist service providers as well as broad-based service providers which also offer engineering services. All 14 service providers are leaders in at least one of the verticals.

Our analysis shows four clusters. The first cluster includes leading broad-based IT service providers which also have scale in engineering services. The second cluster consists of leading specialist service providers with strong expertise in few verticals. The third cluster includes broad-based IT services firms that are relatively late entrants in engineering services and building their scale and capabilities. The final cluster consists of specialist firms which have strong expertise in one or two verticals.

There are four service providers in our Winner’s Circle – HCL, Infosys, TCS and Tech Mahindra that have four things in common: scale, scope, investment in future capabilities and strong customer references.

The eight High Performers in our study are Capgemini, Cognizant, Cyient, Genpact, IGATE, L&T Technology Services, QuEST Global, and Tata Technologies. They are on the right path and building their capabilities.

In this Blueprint, we also focused on benchmarking and operations improvement. This is first of its kind of engineering services study where we tried to collect important operating data from engineering service providers and arrived at the aggregate or the average engineering services industry metrics. This should help each engineering service provider and captive to benchmark their operations and identify their strengths as well as areas or levers of improvement.

Pareekh Jain is Research Director, HfS (Click for Bio)

So what are your key takeaways from this study and what should we be watching for in the next few years?

There are three key takeaways.

First, engineering services is a huge untapped market. Currently, it is dominated by captives but we believe that is rapidly changing as outsourcing to service providers becomes more significant.

Second, scale is becoming very important in this market as it enables service providers to make investments in labs, capability development, additional services and market access which are critical to developing this market further. Finally, the scope and complexity of work being outsourced is continuously expanding.

This year the revenues from engineering services for Indian services providers has grown faster than the IT services according to NASSCOM data, and it is fast becoming a growth driver for the global outsourcing market.

We will be watching three key trends in coming month and years.

First, we believe engineering service providers will witness high growth and eventually service provider outsourcing will overtake the captive outsourcing. Second, we will be watching for mergers and acquisitions among engineering service providers. Finally, we will keep track of how service providers augment their capabilities and service offerings. We believe IoT/M2M and engineering analytics will become mature service offerings in next few years.

HfS readers can click here to view highlights of all our 21 HfS Blueprint reports.

HfS subscribers click here to access the new HfS Blueprint Report, “HfS Blueprint Report: Engineering Services Outsourcing 2015“

Most of the outsourcing industry is still trying to figure out what’s possible beyond doing labor arbitrage really well – because that’s what we do. Sorry, but there I said it – we officially have an identity crisis.

We’re trying to forge a new identity for ourselves and re-imagine what our careers, our services and our platforms could be like if we only figured out how we can define, prioritize and realize business outcomes that are valuable, as opposed to merely keeping the same old factory ticking over at the lowest possible cost.

Sexy robotics software, analytics tools, BPaaS platforms and artificial intelligence can only be effective and impactful once enterprises have re-designed their processes in a way that drives them towards their desired business outcomes. This has always been the case with (now legacy) ERP implementations, where thousands of clients have blown billions of dollars on enterprise software they simply never could mold effectively to their businesses. They weren’t finding problems to solve, they were creating new ones they didn’t need in the first place.

It’s the same with the next wave of As-a-Service solutions – they will fail without the right approach to designing processes that produce the desired results. Without Design Thinking, enterprises are really just retrofitting expensive solutions into legacy processes and likely wasting a whole load of time, resources and money. It all starts with Design Thinking.

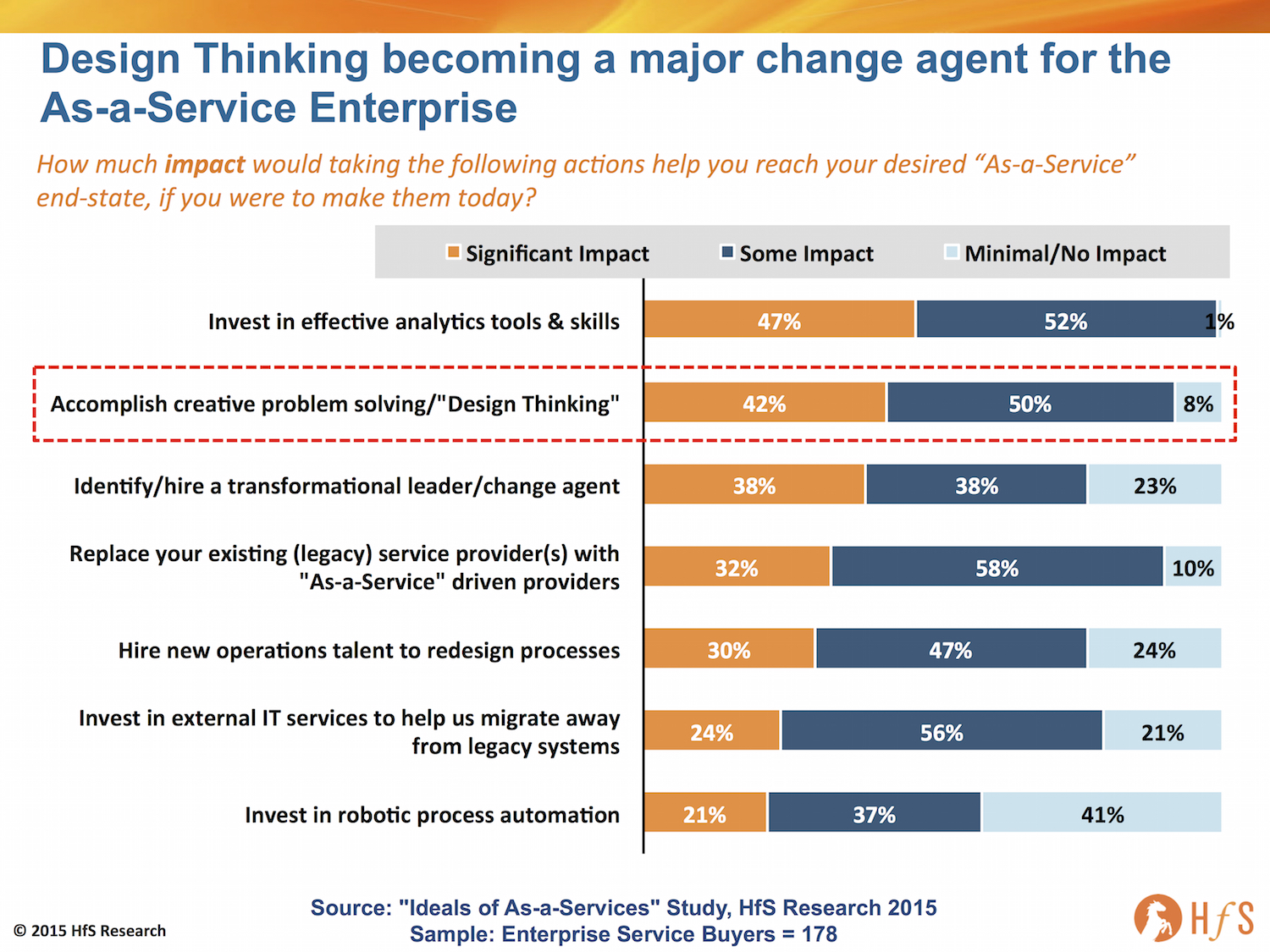

New HfS research into the Ideals of As-a-Service, which canvassed the viewpoints of 178 major enterprise operations executives, points to the rise of Design Thinking and the cultivation of creative ideas, as critical to more than four-out-of- ten enterprises today, in terms of having immediate impact in their quest to reach an As-a-Service end-state, second only the investments in analytics tools and skills:

Click to Enlarge

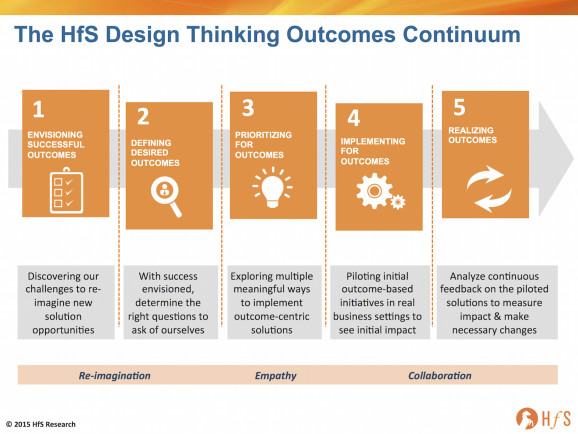

HfS’ Design Thinking Outcomes Continuum aligns traditional concepts with the realities of today’s services industry

In today’s whirl of constant information and social media, it is much easier to visualize how effective enterprises will be running their operations in another five-to-ten years. However, developing a realistic strategy to get there is an immense challenge – and threat – for most enterprises mired in decades of legacy processes and systems.

We all know we need to get smarter with digitizing and automating legacy processes in order to access meaningful data to grow the business and be less reliant on inefficient labor. Plus, an increasing majority of us know we need to explore the possibilities capabilities of self-learning and artificial intelligence, to augment our existing knowledge labor. Today’s challenge isn’t only identifying what the future of operations should look like, it’s developing and adhering to a collaborative and entirely new way of re-imagining processes in order to explore what’s possible and execute against that.

Being successful in the As-a-Service Economy requires ambitious service providers to make fundamental changes to their whole approach to service design and delivery. At the heart of this evolution is a shift to service solutions being designed with real business context, as opposed to simply “looking at a process”. This involves a genuine focus on approaching and interpreting a client’s challenges, identifying and experimenting with opportunities, and ultimately evolving these approaches into the service delivery.

HfS believes that traditional capabilities, such as Six Sigma-based process design and execution, while essential to delivering the efficiency benefits of the traditional sourcing, are today standard, commodity-based capabilities embedded into any standard service model move to an As-a-Service delivery environment.

We believe that a new methodology must be front and center that imbues the full spectrum of human-centric design ethos. This methodology, commonly dubbed “Design Thinking” by several industry stakeholders, is based upon a more responsive relationship between the service buyer and the provider, one that is open, empathetic, experimental and yet efficient. We have seen Design Thinking come to organizational prominence in recent months at IBM, Infosys and Wipro, to name a few service providers, and at the offering or project level in many others. This makes sense to us, because without this more open and innovative approach, it will be difficult to build solutions to meet the challenges and opportunities of the “As-a-Service Economy” such as increasing consumerization of technology and a more virtualized workforce.

As our new survey data illustrates above, we firmly believe 2015 to be the year in which Design Thinking comes to the forefront of the sourcing and services market. It will be the time during which service provider leadership teams are sent to design camps, and a whole new set of conferences and workshops feature Design Thinking as their theme of the moment. Some of that may be hype or even unnecessary, but at the root of it, the arrival of Design Thinking into the mainstream of IT and BPO services makes sense to us as a way to re-imagine more effective process-based solutions for this increasingly digitized As-a-Service world.

There is no one best way to apply Design Thinking, but there are useful starting points, and we believe the HfS Design Thinking for Outcomes Continuum to be a valuable and meaningful way to think about how to solve problems in designing services for the As-a-Service Economy.

Click to Enlarge

The Bottom-line: Design Thinking for outcomes is a real methodology that enterprises can understand and embrace today, not in five years’ time

While we believe Design Thinking will take root in IT and business services in 2015 as a methodology to enable further innovation, at the end of the day it is still just another tool. What you make of it depends on the intent and practices of its users, whether individuals or organizations.

This approach will not be easy for some legacy service providers who cannot yet see how the world is changing. For those service providers and their enterprise clients who can see that thriving in the As-a-Service Economy requires new approaches and capabilities, we see a real potential to use Design Thinking in the move from the present into the future.

Getting new digital processes and services right from the perspective of their end users is critical. Design Thinking, which is about context and empathy for the user, can facilitate this focus. It will be an integral part of the emerging As-a-Service provider offerings, many of whom are already rapidly emerging to redefine the market.

You can read the full POV on HfS’ approach to Design Thinking by Phil Fersht, Hema Santosh and Charles Sutherland by clicking here.

The d.school said this is like many times the total number of students that have taken the course at Stanford. I don’t know what the exact number, but 36,000 is just insane.

The d.school said this is like many times the total number of students that have taken the course at Stanford. I don’t know what the exact number, but 36,000 is just insane. If I have to read another article about Uber’s disruptive business model, I think I am going to defect to a Trappist monastery and brew very strong beer for the rest of my life…

If I have to read another article about Uber’s disruptive business model, I think I am going to defect to a Trappist monastery and brew very strong beer for the rest of my life… Right on cue, after we

Right on cue, after we  Like many of you out there, I was floored last night to see Presidential candidate Hillary Clinton

Like many of you out there, I was floored last night to see Presidential candidate Hillary Clinton