Automation hype and anxiety is everywhere today. In fact, haven’t you been amazed by the emergence of all these “automation experts” that have suddenly appeared on your LinkedIn recently? It’s as if these people went to school 20 years ago with the sole purpose of becoming an automation expert…

However, I have good news for the paranoid – computers are still really bad at simulating social interaction. What’s more, team work is becoming more critical than ever, as we need to keep adapting to a changing work environment. Your personality and ability to excite, befriend, intellectually stimulate, or just have a laugh with the people around you, is now more critical than ever.

Welcome to the socially-intelligent workforce, where your reputation is everything

What’s more, there is nowhere to hide anymore – if you repeatedly behave badly, back-stab, lie, or are just an asshole to work with, your reputation will spread across the digital and social networks, like it never did in the past. When smart future employers check you out, it’s so easy to find former colleagues to conduct informal background checks. There is no hiding anymore, so prepare yourself for the socially intelligent workforce, or scramble for one of those fast-disappearing legacy jobs, where you can hide away for years, unnoticed by the world.

Your ability to interact with people, applying intelligence and creativity to your craft, is where you add value

People, increasingly, want to work with people they like and people who spark positive energy, first and foremost, as technology continually makes jobs more sophisticated and intelligent. I don’t need an accountant who can tell me my revenues this month, as I have software that can do this for me easily… I need an accountant who can talk me through the nuances of sunsetting a legacy product and its impact on my profit line. I don’t need a lawyer who can create employment contracts – I can pull these off Legal Zoom… I need one who can talk through the nuances of creating incentive plans to motivate my staff. I don’t need a web developper who can integrate a few databases – most of these new websites come with them already native to the package… I need a developper who can help design the sexiest website ever to embarrass my competitors. I don’t need content people who just check the boxes to fill content space – you can get content produced anywhere these days (and even automated)… I need content people who want to exchange ideas on creating content that gets noticed and read by our clients. I don’t need marketing people just to send out email-push campaigns – I need ones who can help me figure out which conferences to go to, how to associate my brand with the right partners, how to use social media more intelligently, how to create communities among my clients etc.

I can go on through each profession and business function in turn, but the underlying premise is the same – I need intelligent people I can work with, whether in my company, or in a partner organization. And they don’t need to be rocket-scientist intelligent, just smart enough to understand by business and engage with me to figure out how to do things better. But the value is in the ongoing interaction and team-work, not a wooden worker/manager reporting line model.

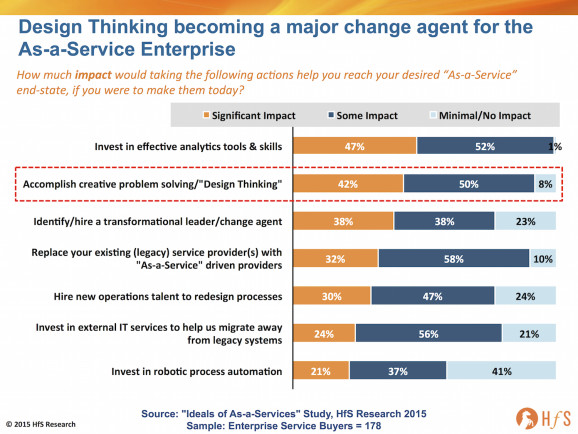

Design Thinking will increase in significance, as the need for socially-intelligent workplace interaction takes hold

This is what I love about Design Thinking – it’s based on the social focus to get us all working together to find problems and solutions together to improve our businesses. Hell, we might not always find much, but at least we’ll have some fun trying. Anything beats staring at a laptop all day going through the motions of the job, right?

When we talked to 178 major enterprise operations executives, the rise of Design Thinking and the cultivation of creative ideas, is second only to investments in analytics tools and skills, in terms of having an impact on their move to As-a-Service:

Click to Enlarge

But this isn’t something that’s coming down the pipe in a few years’ time, people, this is today. This is here now.

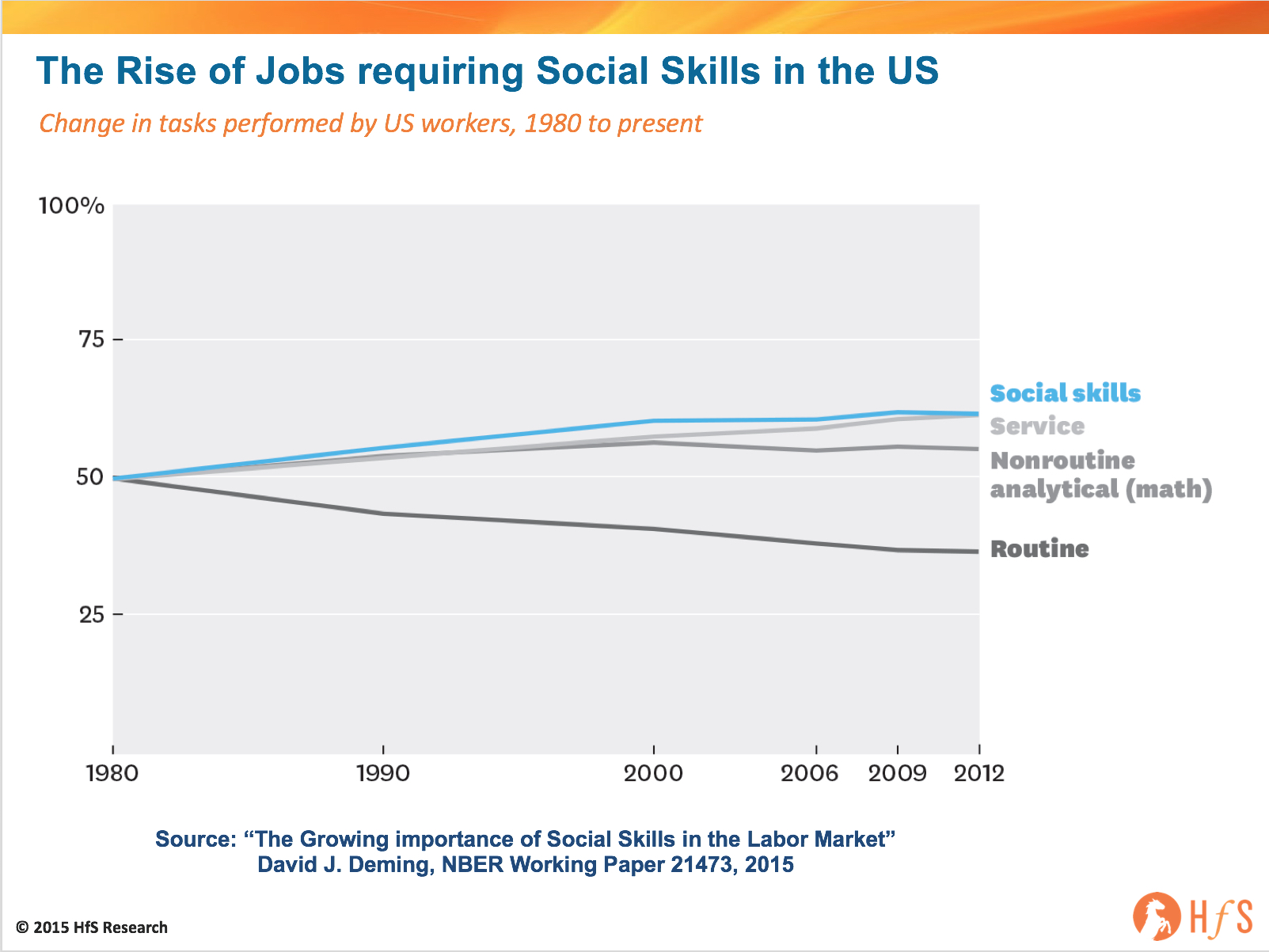

As Harvard University’s David J, Deming’s research shows, jobs aligned to maths tasks grew by only 10% between 1980 and 2012, while those requiring social skills increased by a quarter over the same time frame. And “routine” jobs are plummeting at an alarming clip:

Click to Enlarge

What’s occurring today, is the desire of most enterprises not to increase the people-quota to perform routine jobs – we are having conversations with clients who have plans to eliminate tens of thousands of operational positions in the next couple of years through smarter automation. True, this is a small percentage of the Global 2000 today, but as the case studies roll out, the focus on labor reduction will escalate – and this will be rapid. On the flip-side, the growing number of “Born in the Cloud” business are where most job/work creation is now happening – and it’s these environments where socially intelligent workers are most in demand. In these companies, it’s all about creating a collaborative, stimulating – and enjoyable work culture.

The Bottom-line: Successful socially-intelligent workers are those who can self-reflect and improve

I hate to say this, but it depresses me how many people I come across who simply cannot modify their work style in today’s environment. Social intelligence is being able to analyse your own behaviour and create definitive actions to improve it. It’s not simply messing about on LinkedIn and Twitter… those are tools that can help develop your collaborative personality, but the ultimate collaborator is YOU.

Here are six take-aways here we all need to think about for the good of our careers:

1) Stop the constant whining. Is it any coincidence that some people flit from employer to employer and always have something to whine about? They always know better than their bosses, love to complain about their mistakes, their poor management, how underpaid they are etc. Over the years, it’s always the same story, always the same whining. But recognize the common thread – smart people don’t really like working with the whiners. Negativity breeds negativity, which is the worst demotivator. So take a good look at yourself, truly figure out why you’re unhappy and do something about it. The chances are your whining is because there are elements outside of your work environment that need fixing, not within them.

2) Spend more time getting to know people. Don’t make it all about work. Find out more about your colleagues, clients and partners. Find the right ways to interact with them – some like using the phone, others like texting, others face to face sessions etc. We have so many social tools at our disposal – use them!

3) Collaborate with your colleagues and put your ego aside. I bet you also know several people who claim to to be really “collaborative” but really aren’t at all. Collaborating is about sharing work, sharing experiences, learning from each other. It’s not always about being the smartest person in the room and inviting them to that room. Sometimes is about creating the room for everyone to be smart in together.

4) Be transparent. Nothing irks people more than finding things out about their colleagues that were a complete surprise. Be more open, let people in a bit – and they will likely do the same with you. Everyone’s human – we all have stresses at home, at work etc. Share them a bit. If you have issues with your boss, then clear the air (over a drink even better…). Transparency is critical for your long term reputation and career. If a job is not working for whatever reason, address it and it may improve. No-one ever got fired for airing their issues and trying to fix them collaboratively with their colleagues.

5) Speak up! Management always appreciates staff voicing up in team calls to improve things / suggest new ideas. If you don’t do this, everyone’s wasting their time. It’s not as if you have nothing to add, you always do!

6) Be honest with yourself. Finally, if you’re not motivated by your work, then that’s your problem, not your company’s. True, they may suck, but if you aren’t inspired by the work or the people around you, find answers, and find them fast. If the work doesn’t motivate you, you’re in the wrong profession, if your colleagues don’t motivate you then try to motivate them by actioning the steps above. If that fails, then leave… go somewhere which appreciates you and motivates you.

Insurance is priming the pump for industry-centric As-a-Service solutions. The insurance space is one of those industries where it’s all in the sales, marketing and customer experience, so the more the delivery engine can he standardized and run efficiently, the more cost savings can be passed onto the customer and intelligent data to the service provider to set their policies, pricing and future strategies.

Insurance majors were among the first Western enterprises to open offshore captive centers in India and Philippines to process and adjudicate clients, support customer service etc. However, the main issue that has long-plagued the carriers has been finding value beyond the initial offshore cost-savings. I personally recall hosting a roundtable of eleven major insurance BPO clients five years’ ago, and the common consensus was “The only way to find incremental value is by tech-enabling our processes”.

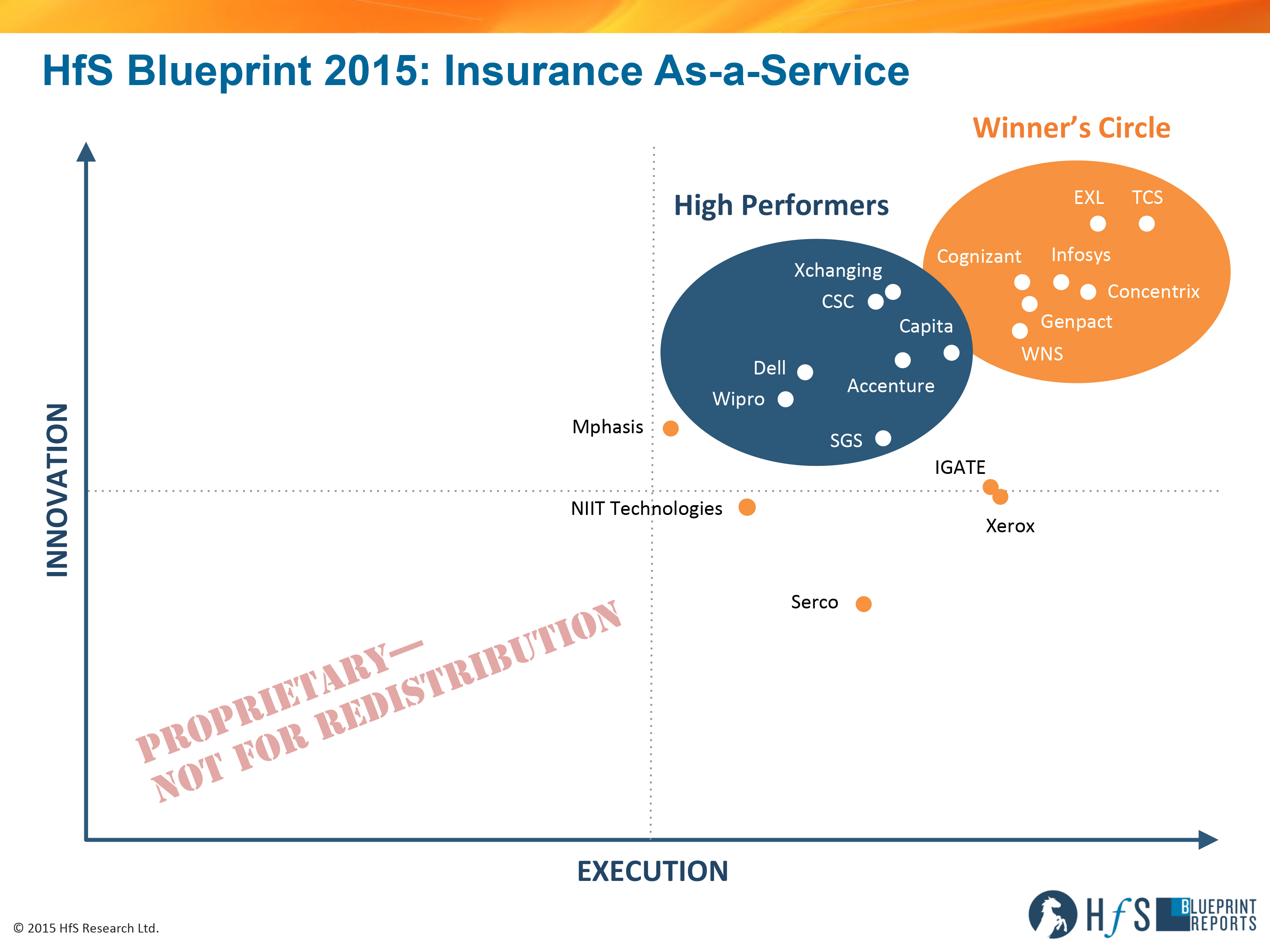

So has this industry been making genuine progress as we evolve to the As-a-Service model? So who better to ask than the one analyst who has been tracking this space intensely ever since she joined HfS four years ago, Reetika Joshi:

Click to Enlarge

What is “Insurance As-a-Service” and how is it different from insurance BPO?

Phil, insurance is a mature market for BPO – core insurance processes like claims processing have been outsourced for over a decade now. Our discussions with property & casualty (P&C) and life & annuities (L&A) carriers across client markets indicate that these services buyers seek value beyond the transactional back-office work of the past. Their expectations include more delivery of standardized processes on modern business platforms, an expanded scope of services and the incorporation of robotic process automation and operational analytics in core operations. We see increased investment and interest from services buyers along with service providers to modernize core processes across the outsourced/offshored/in-house/partner ecosystem to include these elements. For further reading, we published a report on this topic in May 2015 based on a buyer survey – Moving Insurance BPO into the As-a-Service Economy.

What are some of the changes you’ve seen in the market since the last Blueprint?

Industry forces are definitively impacting the nature of sourcing in insurance – be it more regulatory scrutiny and compliance requirements, aggressive competition, low margins or intensified market consolidation. To pull out a couple of examples:

Business models are changing in insurance, and service providers are in the midst of the storm: On one hand, carriers have ageing distribution networks with traditional agents and other intermediaries, while emerging ecommerce and direct sales channels continue to proliferate. Carriers are struggling to understand how to shift the sales paradigm with sales and interactions. Some of this requires new capability development in going direct to consumers for New Business—setting up outbound and inbound sales and marketing operations, ecommerce channels, etc. Service providers are reacting accordingly to facilitate this growth, with more focus on the New Business service area than in late 2013, early 2014.

Growth and focus on TPA model: More private equity investors and reinsurance companies are taking on blocks of business, with the need for strong execution arms that are pushing more responsibility to TPAs. Similarly, ramped up new product development is driving more blocks into run-off. As a result, service providers have scrambled to acquire TPA licenses to service end-to-end insurance processes. We see far more TPA plays emerging in the last 18 months.

We believe these industry forces, along with other equally relevant shifts in the global technology and services landscape, are gradually changing the nature of outsourcing in the insurance vertical towards more Insurance As-a-Service delivery. Our scoring methodology for this Blueprint has changed accordingly. Compared to the first Blueprint on Insurance BPO (Feb 2014), we increased the focus on innovation toward As-a-Service delivery, with 50% of the Blueprint scoring being tied to proven innovation capability and performance for these engagements, beyond the standardized insurance BPO processes.

How are winning service providers approaching this market differently, moving beyond basic operational services?

Service providers, after more than a decade of technology and business services expertise for insurance processes, are in a position to offer more consultative support to help design solutions and even operating models that are more modular, technology enabled and future-ready. Buyers are willing to act based on their internal culture, appetite for change and established relationships with service providers. Insurance As-a-Service is a reality for a growing subset of insurance BPO/BPaaS engagements today. With this new focus on As-a-Service, we saw TCS, Concentrix, Genpact and EXL hold their leadership positions, as well as the entry of Infosys, Cognizant and WNS into the Winner’s Circle.

Cognizant advanced due to the strong progress it has made in the last 18 months in integrating its insurance assets and partnerships, driving new business growth. Infosys has built a strong reputation based off its start with McCamish and made progress on its BPaaS strategy. WNS’ focus on outcome based models and embedded analytics coupled with its flexibility and insurance knowledge helped it advance in position.

TCS and EXL lead the market on Insurance As-a-Service, both on articulating their vision and executing at scale. They are the ones to beat in their respective client markets.

Genpact and Concentrix continue to hold onto their leadership position based on solid execution and articulation of their As-a-Service vision; they will need to make strong investments to execute in the changing competitive landscape for As-a-Service.

Interestingly, the service providers in the Winner’s Circle stood out for As-a-Service delivery for different reasons. Some like EXL have more BPaaS plays, some like WNS are in for focusing on outcomes. The common underlying factor however is their willingness to evolve, the success of their initial forays into including As-a-Service components and charting out progressive visions for insurance that is visible to their clients.

Reetika Joshi is HfS Research Director, Consumer-centric Operations and Analytics Strategies (click for bio)

What do you expect for the future of Insurance As-a-Service?

Insurance operating models will continue to evolve to a more hybrid approach with in-house decentralized, in-house centralized, Shared Service Centers, TPAs and IT-BPO service providers as insurers gradually “let go” with:

More complex functions along the value chain (e.g., claims adjudication, actuarial and underwriting support, CAT modeling)

More integrated technology and BPO solution and delivery models that resemble Insurance As-a-Service, although in point solutions initially

More collaboration and consultative support from service providers on modernizing core insurance operations, irrespective of delivery responsibility and geographic spread

Overall, HfS sees the insurance vertical as ripe for a rethink in design and execution for the As-a-Service Economy. The foundations are already present—mature processes, service providers’ domain experience, buyers’ appetites for platform-based delivery, and burning platforms for change in business models for both L&A and P&C. However, insurance carriers need to get on board to ensure success. Services buyers need to make concerted efforts to align stakeholders around the As-a-Service economy. From our discussions with clients, service providers and other influencers, we see a pronounced lack of synergy around core operations from insurance carriers in P&C and L&A – across lines of business, inherited assets, TPAs, BPO and IT relationships. We see service providers continue to make investments that will disrupt this mature market in the next two years. Winning service providers are leading the way and starting to help clients navigate through this disruption by offering scalable and adaptable technology-enabled solutions. At HfS, we’ll continue to report on these successes, failures and learnings on the long road to Insurance As-a-Service.

HfS readers can click here to view highlights of all our 23 HfS Blueprint reports.

HfS subscribers click here to access the new HfS Blueprint Report: Insurance As-a-Service 2015

During Part I, we discussed the gradual simplification of cumbersome people-centric outsourcing towards technology-centric “As-a-Service” solutions, driven by the need for enterprises to remove their excessive operations costs and anti-competitiveness burdens inflicted by legacy processes and obsolete technology.

Simply put, what worked last decade no longer works for ambitious enterprises striving to stay competitive, plus the emerging “Born in the Cloud” enterprises, many of which will comprise tomorrow’s FORTUNE 500, where As-a-Service is native to their operations, not retro-fitted in painful increments. Their mantra is to invest in outcome-centric services first, then hire talent to broker these capabilities and align them to the revenue-generating activities of the business.

Gone are the days when the only solutions were to reduce labor costs and hope for the best. Arriving are the days where investments in outcome-driven solutions, fueled by common standards and automation, ubiquitous cloud delivery, digital tools and apps, are being seen to have genuine long-term ROI. Enterprise leaders, in our discussions, are much more willing to make investments in permanent solutions, where the outcomes are tangible, as opposed to temporary solutions, where there is some short-term benefit, but the long term outcomes are still murky and unclear.

We know the future is moving towards a state of creative, motivated operators accessing available tools and intelligent platforms to help their enterprises achieve their desired outcomes. We know most viable enterprises, today, cannot afford to drag around these archaic, obsolete infrastructures and operations – and remain competitive in the long-term.

So what, pray tell, is really driving our enterprises to make decisions today, what will our world really look like in five years’ time as a result, and what are the implications for society and business? Oh the questions that need answering…

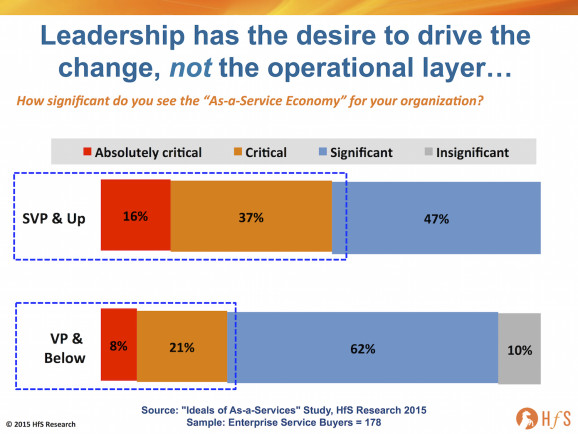

Two-thirds of enterprises are actively pursuing strategies to reduce reliance on human capital

“How much of this room will be replaced by bots in the next three years?” I asked, polling some peers and colleagues deep in client-side automation research attending a recent service provider conference.

“As many as 60%” was the collective response – 30% directly through improved automation capability and another 30% simply through better apps and efficient processes”. Just think about that for a minute… we’re really on an path away from people to technology. So why are so many services and operations professionals so blissfully unconcerned of what’s coming? Are we living in permanent state of denial that the business world around us is simply never going to change? It’s not as if the majority of senior operations leaders do not see As-a-Service as critical, according to our new Ideals of As-a-Service study:

Click to Enlarge

So, while the leadership layer is clearly bought in and ready to go, why aren’t the operational middle and junior layers following suit? Why aren’t these leadership ambitions being translated down through the ranks? Why does this desire to challenge ourselves and improve our capabilities dissipate when we reach the rank and file?

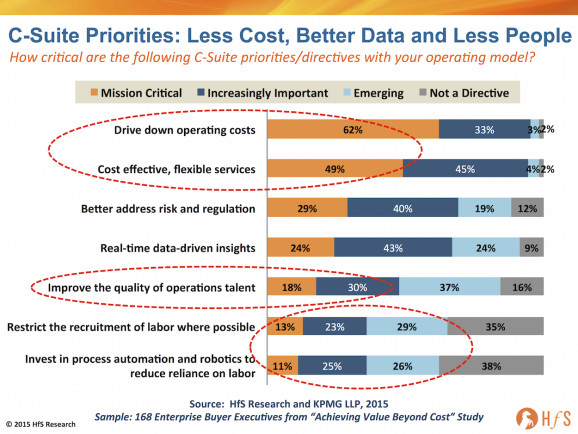

Maybe this is the reason why two thirds of operational C-Suites are actively pursuing policies to restrict labor investments and are evaluating automation strategies… they’ve accepted they can’t really change the people they have (only 48% see improving operations talent as important/critical), so need to focus on the overall model, the technology and tools, to make the real sweeping changes:

Click to Enlarge

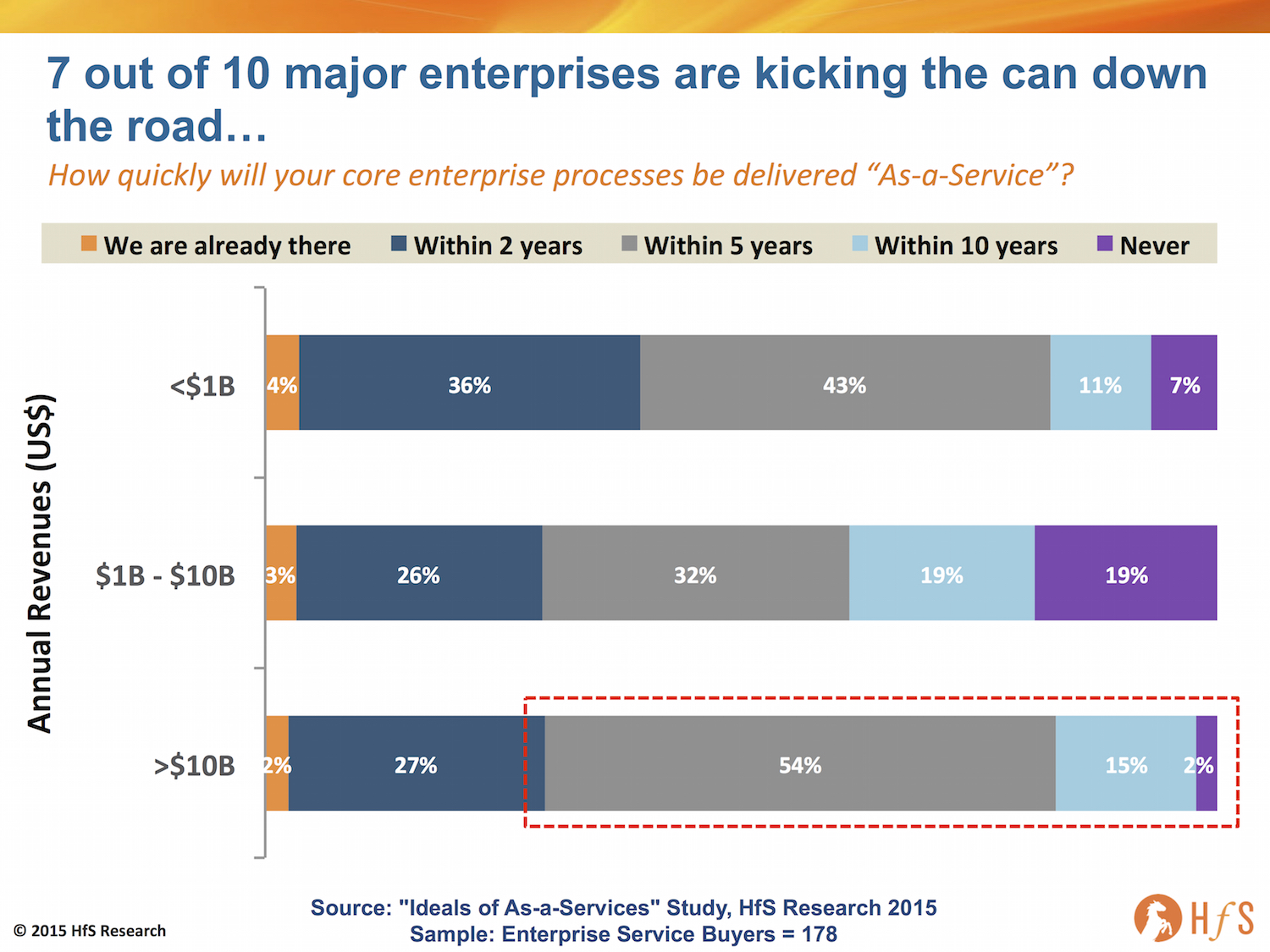

Lots of talk, not too much action, as seven-out-of-ten firms pass the real challenge of change onto others in the future…

When we asked the buyers in the As-a-Service study when their enterprises were going to have its core processes delivered “As-a-Service”, many answers to these nagging questions are revealed:

Click to Enlarge

Lets face facts here – anyone who predicts something for their business five years out is, is predicting science fiction. Noone can really see out more then two years, possibly three at most, with their organizational investments and intentions.

Simply put, most major enterprises still believe they have mileage in the traditional labor arbitrage model. There is clearly an absence of a burning platform—or capability—to drive change in the foreseeable future. Our research found two exceptions: healthcare and life sciences organizations that have exhausted this model, and enterprises under $1 bn. Small and mid-sized enterprises (SMEs) are often less resourced and with fewer opportunities with the labor arbitrage model, having less operational scale.

The Bottom-line: Enterprises must fix the disconnect between leadership ambition and operation lethargy …and go for more “big Bang” change

What is truly worrysome here, is the speed of change in today’s global environment and what could happen to many of the organization simply paying lip-service, when it comes to hauling their antiquated back offices out of the dark ages. And, heaven-forbid, we are struck by a renewed global downturn, with so many of our enterprises failing to adapt to the modern business environment. Last time I checked, worrying signs are emerging with the faltering Chinese currency and European basket-case economies seeking to go beyond being basket cases (a phase for which has yet to be coined).

One of the biggest obstacles to enterprises achieving progress towards achieving As-a-Service Ideals, is this huge delta between the desire of operations leadership to make the transition and the lethargy of the middle management layer. If this gap cannot be closed, there will eventually be ramifications for many enterprises which will see their competitiveness slip away due to an overly complex, expensive and inefficient operating model. People’s careers need to be aligned with where the industry is going – not where it has languished for many years.

What’s more, incremental fixes clearly do not work – for all stakeholders. We have entered an economy where writing off legacy investments needs to occur for so many. Just because an enterprise invested millions in a now-obsolete set of processes and technologies doesn’t mean that enterprises should been persisting with plowing further resources into them – there comes a point where money spent in maintaining the old is wasted, while investments in solutions that drive real outcomes have some ROI down the road.

We need to reach that pivot-point where business leaders make real, definition investment actions to change their operations, otherwise we’ll be forced into another recession-induced series of changes to many businesses, which are rarely driven by proactive decisions – but by reactive behaviors only designed to make quick fixes, not long term ones.

Ignore this at your peril… but we really are at the early stages of a “Digital Revolution”, which will ultimately have an impact as seismic as the Industrial Revolution of the 19th century, which left us with entire workforces untrained and unskilled for what was needed next. The same is happening today – and we need to get ahead of this by being unafraid to reorient our capabilities and career trajectories.

The last 30-40 years has merely been pre-amble as enterprises leveraged globalization and technology to lower costs, automate and standardize processes (ERP, apps, offshore-nearshore outsourcing) and consumers to improve their lives (PCs, mobile, social). However, these are only the baby steps, where we experimented on what we ultimately needed from technology. Today’s emerging generation has digital at the core of both their home and work lives, while the more mature generations are trying to retrofit digital into our (becoming) obsolete business processes and social lives. The big shifts are starting to emerge now and this is having a critical impact on our careers – and many of you may not even realize it yet. So… don’t become confined to the scrap heap of legacy workers whose skills are simply no longer relevant for the modern workforce.

Check out the Horses Job Board!

The perennial problem with our industry is the lack of career paths – and a lack of willingness for employers to go “outside of the box” to find that next set of skills that can take them into the Digital age.

I can’t count the number of times someone has stopped me at an event, called me, or dropped me an email to ask one question: “I’ve got a job opening. Do you know anyone who’d be a good fit?”. Or “I need to go work somewhere that isn’t dominated by passionless managers, politics and turgid review processes.”

The fact is, we know lots of people – in fact, well over over a hundred thousand subscribe to our research and blogs and we estimate we’ll surpass a million clicks on this blog alone this year . And, although most of you who read this blog are all pretty much gainfully (or ungainfully) employed, you might be interested in a change of scenery. And in our dynamic business, you all probably have an opening or twenty you’re having trouble filling – or simply want to try an avenue beyond LinkedIn and the next cardboard conference of perennial job seekers… who just aren’t very good.

So, it hit me: Let’s start a community service job board where the real talent can discretely shop around to escape their legacy purgatory…

And what we’re unleashing on our global HfS community is the Horses Job Board. You may have already noticed it lurking around on the right hand side of your screen.

Contact Bram Weerts to get your job ad featured here.

You can easily place a job listing on the board by clicking on “Jobs” in the nav bar above. We have a simple form that takes a few minutes to fill out.

All the applications will come directly to you—either to a URL or an email address. No middle man. Job seekers can easily browse the listings or search by keyword or location. It’s that simple. And interested applications don’t need to plaster their career attentions all over LinkedIn or some dodgy recruitment shop.

Best of all, the listings run for 10 days—free!

And if you have a really critical role you’d like to fill, we have a feature spot on the right side of the blog that is available. Do contact Bram Weerts to learn more about that.

If I had a dollar for every scuba-diving triathlete mom who specializes in the art of service buyer/provider relationship management and governance strategy for a big 4 management consultancy… I really wouldn’t be very rich.

Liz Evans is KPMG Managing Director for Governance (Shared Services & Outsourcing Advisory)

Liz Evans has been at this for several years now, from the early days of Equaterra, where she was marriage counseling for most of the broken outsourcing deals in the industry, through to KPMG where she has molded her craft into the GBS governance functions of many of the largest enterprises in the world.

Not bad for a nice lass from a town called Middlesbrough, somewhere up in the north of England, who’s firmly implanted herself as a governance therapist in many North American boardrooms (when she’s managed to yank herself away from her Lego-addicted kids).

So, after all these years since we last spoke, we thought high time to get reacquainted with Liz to find out just how much things have changed in the industry…

Phil Fersht, CEO, HfS Research: Liz, it’s great to talk with you again. I think it’s been five years since we last spoke to you on the blog. You’ve built quite the reputation at KPMG these days for leading a lot of the governance strategy and how clients are maturing post-transaction. I think our readers would like to hear a bit from you about your background and some of the early days in your career, and how you ended up becoming such a respected governance and relationship management practitioner in the industry.

Liz Evans, Managing Director Governance, KPMG: Thanks Phil – it’s great to speak to you. You know, I did a conference—a Governance roundtable last October—and one of the sessions was on talent management. The first question I asked the audience was, “Put your hands up if, when you left university, you wanted to be a governance professional.” Shockingly, no-one raised their hands. And I have to say I am in the same boat. So I think the route into governance and this industry is often an interesting one.

I started off doing outsourcing deals way back in the mid-‘90s. And I actually focused much more on service levels. And then was asked to look at the structure of how you manage those on an ongoing basis. It kind of led me down the road as well. Service levels and service credit really are not all there is to a relationship—it’s much broader. I think the rest, as they say, is history from there. When I joined EquaTerra in 2005, I had the opportunity to really spend my time focusing on governance as a true discipline and expand my opportunity to include not only IT, where my background is, but also the BPO space as well. And then looking at shared services, and now in the KPMG world, I get to really look at service delivery governance from a much broader perspective now that we are looking at global business services and what that means for organizations and how people focus on it.

Phil: Now let’s talk about GBS for a bit because I think we have sort of come off the initial buzz of “What is GBS?” and why it is a growth path for many organizations to take. From your perspective, coming from traditional outsourcing into shared services to where we are, how would you describe what GBS is today to a sourcing executive on the buy side and why is it something that they should be excited about?

Liz: That’s an interesting question. I have a firm belief that GBS is really about changing not only your organizational structure but also the mindset upon which you are delivering services. It is not only about the value and the knowledge and the talent within a given function—let’s just say IT or finance. It is also about how you get those traditional functions in your organizational structure to really work together effectively to deliver services or a complete end-to-end process to the business customers.

It’s a different way of looking at a work construct. And to do that you have to get different organizational groups, leadership, and delivery people, whether they are internal or external, to work together in a regular, common cadence that allows you to make sure things do not fall through a crack, the performance is delivered, where you understand where the performance is, and you’re able to make changes to the model. All of this requires governance. And so I think, fundamentally, it is a mind shift—changing from function to a wide- view of either service or process. You need to really understand what your customers want to purchase and design their experience, versus just delivering to them based on a collection of talented resources that you have in Finance, HR, IT, or whatever function it happens to be.

Phil: And you know, I think in sort of deconstructing some of the terminology, a lot of people think GBS is just something that the top 100 organizations in the world do. Do you agree with that, or do you think GBS is something much broader, which many organizations can get involved with?

Liz: Phil, I think many organizations can get involved with GBS. If you look at how you are delivering for your organization and start changing your mindset from function to service or function to process, the size of your organization does not matter. It gives you an ability to scale, to monitor costs, to monitor performance, to take advantage of the data that is available to you cross-functionally in a way that you have not done before. And I think that’s applicable to any organization. Everybody is looking for opportunities to do things better and faster. They are looking for opportunities to leverage their external partnerships that they have more effectively. We are all looking for ways to improve. And I do not think that’s restricted to large organizations. I think that’s pertinent to everybody.

Now, how fast they go up that maturity curve and how quickly they transition through that journey of GBS, I think that’s a different conversation. I think getting to Level 5 GBS in three years is unpalatable for some organizations. But I think it gives you a construct of how to understand the value that you can deliver to your business. And I think that’s the essence of the value and the benefit of a GBS mindset. It changes from “I can deliver, I can do accounts payable, or I can have my service provider do accounts payable” to “Where is the value of accounts payable in the wide-ranging process of supporting my business to deliver products or services to customers?”

I believe it changes your mindset.

Phil: So, Liz, how does this affect people’s career paths? I mean, this has been the perennial issue for the outsourcing industry for a long time… you know how people often call it the “accidental profession.” People sort of fell into it and ended up trying to work out how to do it as best as they could, to get through the day. How do you think the approach is changing regarding careers in GBS and managing capability? Do you think we are getting better at it? Do you think there are qualifications out there that are helpful? Is there a curriculum being defined at this point or are we still grasping at straws with how companies should best approach this?

Liz: That’s an interesting set of questions, Phil, and there are a couple of thoughts that come to mind. One is, from the conversations I have with a variety of clients in a variety of different sectors, talent management is very prominent in their thinking. They are asking, “Do I have the right people to affect this change?” Because it is a gigantic change for an organization to shift from the traditional structure and way of thinking on handling a function to delivering services. “Who can help me?” “Who can lead this change?” “What are my succession plans?” I feel like talent management as a topic is not an afterthought in GBS. It is a very prominent part of the dialogue. And the other thing that is a part of that is there are a number of organizations out there seeking GBS talent. It is quite astonishing.

A lot of organizations are going externally because they recognize that they want people with experience in those leadership roles who can drive the change in the organizations with the speed and the success rate that they are seeking. So I think that’s actually a good signal in terms of finding that talent. I think that some of the recruiting agencies are struggling to really be able to articulate and quantify what GBS experience in leadership means. But that’s something I think the industry will catch up with.

The other point I would make is—and it kind of links the talent and the governance piece together—the experience that we all have in the outsourcing industry traditionally, where there was a very strong rigor around governance, helped establish talent management as a prominent feature in the GBS conversation. So I do think the industry is evolving and learning lessons of the past. You know, “We put the wrong people in the positions and we struggled, so with this change, which is even bigger than a single shared service or a single outsourcing agreement, we need to have the right talent.”

I am actually encouraged by the way in which talent is discussed and understood in the GBS dialogue. I still do not think there is a plethora of folks who have the experience, but I think there are an increasing number of folks who have the experience. And they are becoming more and more marketable in the industry.

Phil: That’s a good point, Liz! And why are they becoming more marketable? Is it because they are basically figuring themselves out a bit and realizing that they have to take their career in this direction to be successful? Because, all I hear every day from people is they can’t get talent, there is “nothing out there”. However, over the last five years, I’ve seen many of the same people really changing their approach.

Liz: Yes. I think that’s right, Phil. I think GBS has introduced a new language to the industry. And I think there are a number of very experienced leaders who have adopted that very quickly in their own marketing approach to their own careers, and who have aligned their experience with what GBS is trying to achieve. I think those are the folks who are really market leaders, who are rising to the top and being phenomenally successful, which is fantastic to see. We have a number of prominent lights in the industry that have been successful in the GBS role.

I think it is helpful that we are codifying that language. I feel like it took us a while to do it in shared service and outsourcing. We kept those languages very distinct for quite a while. But I do feel like people are proactively looking at opportunities and aligning their experience better so they are marketing themselves better. And they are being more proactive in how they are directing their own career in a GBS environment. I think there are a lot of opportunities for folks.

Phil: You have come through various situations in the industry—from lift and shift outsourcing to more transformational BPO/ ITO to GBS. So, what do you think the world is going to look like in another five years?

Liz: That’s an interesting question. Robotic Process Automation (RPA), which is a big buzzword at the moment, will become increasingly prominent in the marketplace. And I think commercial arrangements are going to look and feel very different. I have every expectation the service provider landscape will change considerably. Just as we saw with the growth of the offshore service providers and changes in traditional domestic companies engaging with offshore, and we saw lots of mergers and acquisitions and consolidations, etc., I think we will see a lot of new entrants in the marketplace in the RPA space. I suspect that that will shake out over time.

So whether it is the big players that we have today, who knows? But I think we will see some new names and I think we will see more branding around these new innovative services. And I actually think with robotics, we will have the opportunity to realize the dream of innovation within supplier relationship. So, you know, Phil, because you have looked at it for many years, one of the struggles we have already in traditional outsourcing relationships is innovation. What does innovation mean? Does it mean continuous improvement? Does it mean redoing my SLAs every year? Or does it mean really doing things differently? It is about actually labeling what innovation means and how you fund it. I think things like RPA can give us the opportunity to realize the dream of innovation within the construct of our external relationships as an industry.

I am actually quite excited about that. I am excited about the opportunity to really transform the way in which work is done and to change a lot of the commercial and relationship models. I think the next three to five years are actually going to be quite exciting as we see changes in the service provider landscape, companies’ adopting new services, and realizing the dream of innovation. I feel like that has eluded a lot of companies for a long time.

Phil: I have one final question. Do you think we are heading towards a path where companies are going to have a Chief Services Officer or a Chief Governance Officer? Or do you think it is going to become more of a capability rather than an actual specified job, as we evolve?

Liz: Wow! That’s a good one to noodle. I feel like governance is becoming increasingly prominent. I feel a lot of organizations are instituting enterprise-wide centers for excellence governance – you could argue that the leader of organizations is a Chief Governance Officer. That’s definitely a trend. I do not see that label used. And I think there are some challenges with using Chief Governance Officer and then Corporate Governance and the two different functions would be interpreted. So I am not sure I see the label per se, but I definitely see different constructs within the organization. I see governance as a key responsibility within a new GBS structure. I see it as a discipline and I see it more prominently on the organization chart. But I do not predict there will be new labels around Chief Governance Officer.

Phil: That’s great! Well, Liz it’s been great to have you back on here and how have your views developed over the years.

Liz: Thank you very much for the opportunity to connect, Phil.

Liz Evans is KPMG Managing Director for Governance, Shared Services & Outsourcing Advisory. You can view her profile here.

When we coined the term “The As-a-Service Economy” a year ago (remember our famous Ten Tenets post), we never quite anticipated we were helping define the future model the services industry would adopt for business, technology and operational service delivery.

As-a-Service replaces Outsourcing

We’ve perennially debated the (toxic) term “outsourcing”, long vilified as the substitution of onshore jobs with cheaper offshore people. The outsourcing community has continually struggled to find new defining terminology, as NASSCOM replaced “BPO” with “BPM” and the IAOP has refused to shift from the past, staying true to the O word as its core identity.

The reason why we struggled with our identity was because outsourcing, by and large, has really always been about people. It’s hard to change processes, drive common standards across clients, build a utility model that can be scaled and made cost-efficient, when you’re really just moving work around the world with the goal of getting it done cheaper. And that’s really been the story of outsourcing to-date – service providers battling it out, at varying levels of effectiveness, to deliver people-based services more productively, promising delights of delivery beyond merely doing the existing stuff significantly cheaper and (hopefully) a bit better.

But outsourcing hasn’t failed. Only 13% of service buyers in our new Ideals of As-a-Service study believe there is no more value to be found in the current outsourcing model. Outsourcing is the starting point towards driving out bloated labor costs, centralizing the delivery staff within a service provider, and creating some basic common standards across processes. However, it’s not the end-solution for ambitious firms, it’s merely the start of the journey towards this future vision of “As-a-Service”.

We also hear a lot of hype about Robotic Process Automation, which is another accelerator towards As-a-Service, but like outsourcing, RPA isn’t necessarily the end-solution either – many applications have a lifecycle and are replaced over time, and many of today’s processes become obsolete as businesses evolve. RPA merely acts as a further conduit, coupled with outsourcing, to smooth the ultimate journey towards destination As-a-Service.

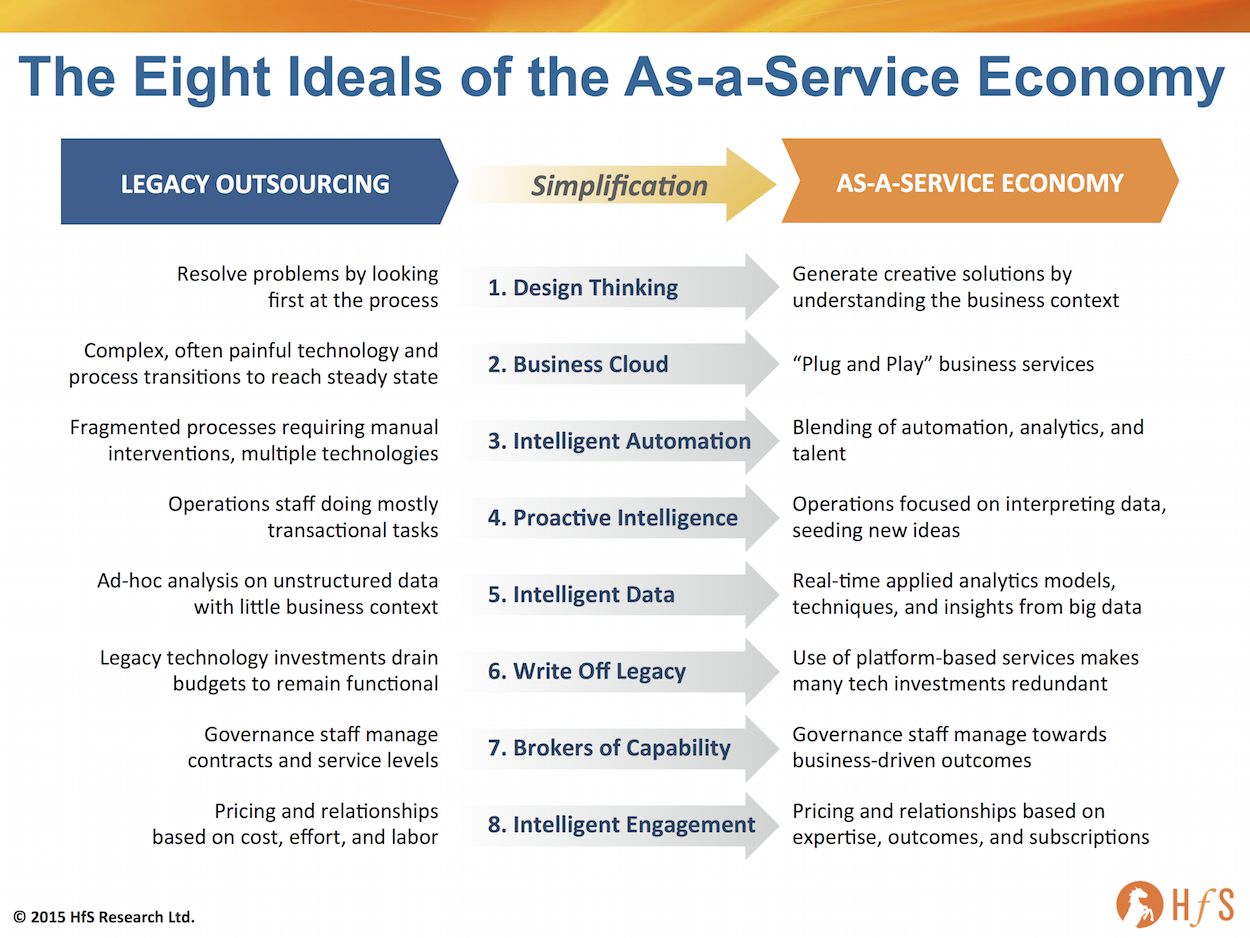

Defining the evolution to the As-a-Service Economy with Eight Ideals

The game-changer is centered on today’s services work gradually becoming a genuine blending of people-plus-technology that helps us inch towards an ultimate destination of services value, accessible on-tap, empowering service buyers to focus on proactive value-identification with help from their service partners through meaningful and secure data, enabled by intelligent automation and digital tools… all made possible by smart people working together.

So let’s examine the Eight Ideals of As-a-Service, into which we delve in-depth in our new defining report, “Beware of the Smoke: Your Platform is Burning“, that canvasses the views, dynamics, aspirations and intended actions of 716 service industry stakeholders:

Click to Enlarge

The journey to As-a-Service is all about simplification

Business services, today, are one of speed to business impact. They are about simplification. They are about removing the blockages and obstacles diluting this business impact. Anything less is not taking advantage of the experience and capability that has been developed in the global services market, over the past three decades. In this time, enabling technologies, talent, sourcing operating models, and macro-economic trends, such as globalization of labor, high growth emerging markets, new business models and consumerization, enable service buyers, advisors, and service providers to engage increasingly in a more flexible and collaborative manner. The ambition is to achieve renewed business results with speed, quality, and effectiveness. When we get there, we will be in the As-a-Service Economy.

The transition to As-a-Service is all about simplification — removing unnecessary complexity, poor processes, and manual intervention to make way for a more nimble way of running a business. It is also about prioritizing where to focus investments to achieve maximum benefit and impact for the business from its operations.

The emerging As-a-Service Economy will be more agile and dynamic, featuring on-demand plug-and-play services in a one-to-many fashion targeted to impact what matters to consumers as well as businesses. The two are increasingly intertwined as consumer insights, decisions, and loyalty carry increasing weight on the success or failure of an enterprise in any industry.

The Bottom-line: The As-a-Service Economy is a vision for the future, building on today’s achievements

It’s easy to deplore how poorly our business are run, how dysfunctional are our processes, how badly integrated are our technologies, how reactively and transactionally our staff perform. But this is the evolution of business, this is how we got here today. When you talk to service buyers, they are unlikely to tell you their businesses are running worse every year. In fact, most have improved immensely over the last five years with improvements in global scale delivery, cloud computing etc.

Survival in today’s global business environment, for most, is a marathon, not a sprint. Not every industry has been Uberized over-night – most are being disrupted with technology-driven business models that we can learn from, adapt, adjust and try to get ahead of. Most enterprises suffer from the same woes and face similar challenges to clear their path towards their desired As-a-Service Ideals.

The new challenge is to prioritize which Ideals really matter and how to work with the smart people and partners around us to get there. In subsequent posts to this theme, we will analyze our study findings further to understand the priorities, obstacles, expectations and anticipated dynamics to unravel how we will eventually arrive at the As-a-Service Economy, and what we can do as an industry to get there and prosper.

Please download a copy of our new Industry Report “Beware of the Smoke: Your Platform is Burning”, authored by analysts Phil Fersht and Barbra McGann, that analyzes findings from 716 service industry stakeholders in our new Industry study that defines the future of services and the emergence of As-a-Service Economy.

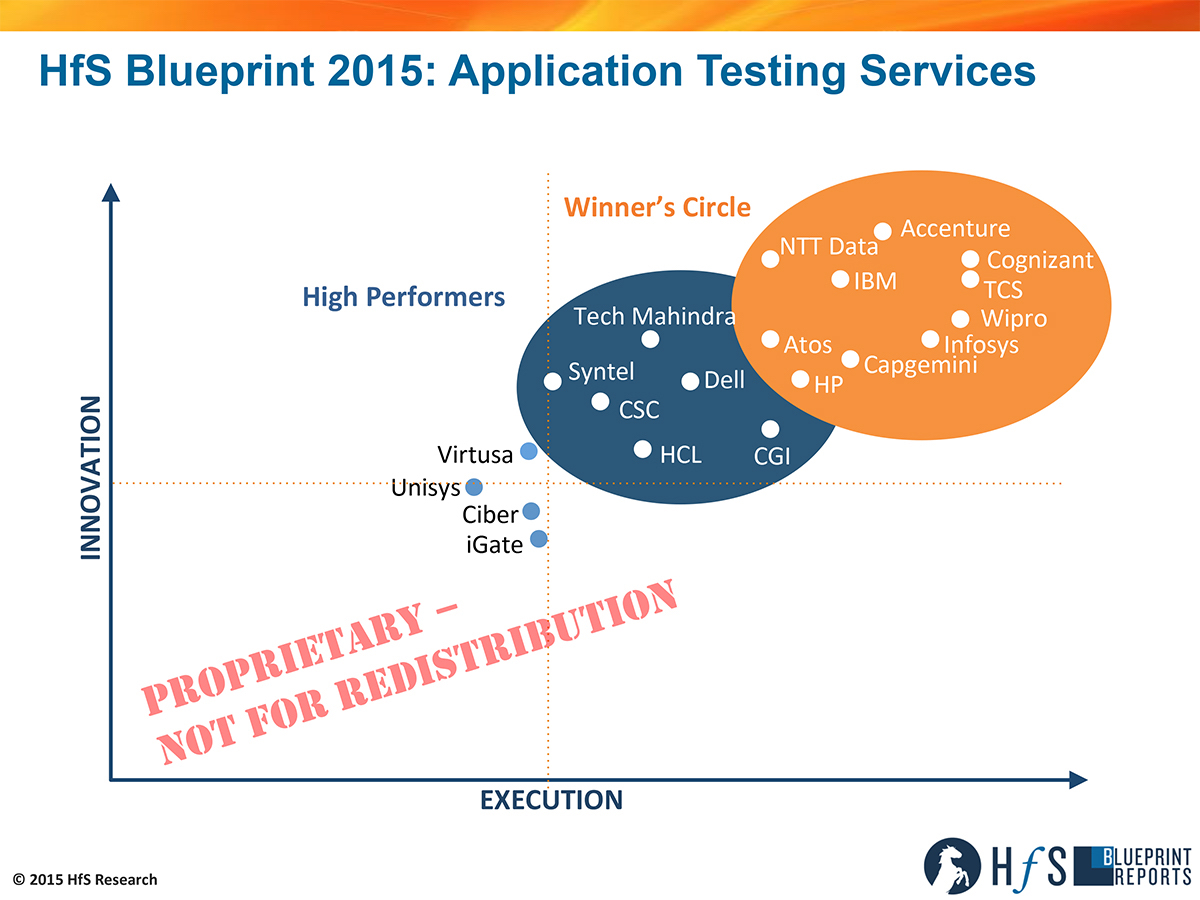

The lifeblood of the IT outsourcing industry has always been application testing – it’s not sexy, but it’s a huge portion of ITO spending – and massively important to the revenues of the major ITOs.

And while much of the traditional app testing market is commoditizing, with advances in remote management and automation, the proliferation of digital apps (social, mobile, analytics) and related technologies are creating renewed growth and market demand for testing. Here at HfS, we have watched this development closely. And, with Tom Reuner on board as Managing Director for IT Outsourcing Research, we thought it high time to take our Blueprint microscope and have a close look at application testing services. Tom worked feverishly over the past couple of months to prepare the Blueprint, along with HfS Executive Vice President, Research Charles Sutherland. The result is a groundbreaking Blueprint report:

Click to Enlarge

So let’s get an up-close view of the report from the man himself, Tom Reuner:

So what’s new in App testing these days, Tom?

Thanks Phil, in order to answer your question, I have to start by going one step back and outline where the industry is, as there is little reference material from analysts and third-party advisors. The notion of independent testing is evolving where services are not just bundled as part of an IT outsourcing contract but are delivered as a stand-alone offering. But, broadly speaking, testing services lag most IT service lines in terms of mindshare and broader visibility. A lack of investment, immaturity of organizational models, a highly fragmented supply-side, and inadequate marketing top the list of reasons behind this. Or, to put it in simpler terms, it is rare to see testing as part of broader sourcing discussions or conversations on how testing is helping organizations on their journey into the As-a-Service Economy.

But things are starting to change and the maturation is tangible. Increasingly, we see standalone testing outsourcing deals in the hundreds of millions of dollars. Organizational models are evolving with mature approaches, often blending centralized and decentralized concepts. Furthermore, the leading providers are progressively embedding testing into the delivery of business processes, in the process moving up the value chain beyond a narrow focus on tools and technology. And lastly, capabilities around cognitive computing and artificial intelligence are being built out and are increasingly underpinning mature approaches to test automation However, what is still woefully inadequate is the marketing around testing services. In order to get a seat at the table for the big IT decisions, the testing community has to move beyond an emphasis on tools and technologies by building out narratives that resonate with process owners, namely around business case, transfer of assets and people as well as mitigating risks.

You’re considered a real guru in automation these days. Surely, automation is having a huge impact on the app testing space? Or is this simply driving up the quality of the labor component? What’s your view and experience here?

As I tried to explain in my introductory remarks, testing is at a different maturity level than most IT disciplines. So automation is largely discussed as a means to get to higher levels of industrialization by augmenting labor. But it’s not included as much as a means to replace FTEs – as we have seen for instance in the discussions around RPA. Fundamentally, we haven’t had a discussion on disruption in the testing community as yet – and it would be a difficult one because most professionals chose testing as a career and it wouldn’t be easy to retrain or rebadge them.

However, it is striking that there are some strong innovations in test automation that haven’t been leveraged in the broader market. The testing community should be more vociferous about its achievements. Furthermore, leading providers should demonstrate the increasing maturity with capabilities around cognitive computing and artificial intelligence – all with a view to move toward more predictive models. However, the flip side of this argument is that you can’t confine automation to testing. It needs to be part of a holistic approach to delivering services. And the acceleration of the journey into the As-a-Service Economy will exacerbate these issues significantly.

How are the winning service providers approaching app testing services today? What are they doing beyond the bread-and-butter basic operational services?

To differentiate your offerings is, by no means, easy. Much of the technology is based on standardized third-party tools. But the providers we have positioned in the Winners Circle stood out in a crowded marketplace for different reasons. Starting with some highlights in the context of execution: For TCS, testing is a standalone business unit and testing is a door opener for new logos. At the same time, Cognizant is the leading provider for comprehensive outsourcing with strong traction in the banking sector. IBM demonstrated solid traction in complex global deals, including its strong capabilities in the Japanese market. Finally, Capgemini deserves credit for educating the market on comprehensive outsourcing. Looking more closely at innovations, Accenture added a strong narrative on evolving toward predictive testing, underpinned by expansive analytics capabilities, plus the provider has built out strong industrialized vertical capabilities. NTT Data stood out through its innovations around mobile testing. In addition, Wipro embedded testing automation within its overall approach to automation, leveraging tools such as Fixomatic to provide predictive analytics and cognitive systems. These are just some examples and I could have added more providers with similar approaches. But the common denominator of the companies in the Winners Circle is that they stand out due to their vision to increasingly embed testing into business processes and encourage its evolution into a much more strategic proposition.

Tom Reuner, HfS Research (click for bio)

Many of the Indian-heritage service providers built their businesses over the years from app testing support for major Western enterprises. Is this still the case for many? Isn’t it still a major component of their revenue base?

There are various ways of looking at it, Phil. Fundamentally, testing services are high-margin business. As such, they have a high strategic importance for every provider. Suffice it to say the leading Indian-heritage providers are constantly evolving and building out capabilities across the board, including consulting, infrastructure, BPO – you name it. This way they have much more balanced portfolios and can move up the value chain to become strategic providers for their clients. On the other hand, the market for testing services is highly fragmented. There are still many pure plays with a focus on specialist services or specific verticals. So consolidation is unavoidable, as IT services are all about global reach and scale.

With the maturity of global labor delivery at scale, and with these advances in intelligent automation and cognitive computing, how to you see the app testing market unfolding in the next 2-3 years? Is the advent of digital, mobile, RPA, and so forth, driving the need for more testing?

Good question – but not easy to answer briefly. My gut feel tells me that the leading providers will accelerate building out more business-centric approaches. As a result, they’ll provide a much stronger demarcation to the many pure plays. The reference points here are embedding testing into business processes, embracing comprehensive outsourcing and supporting clients in their journey into the As-a-Service Economy.

While the direction of travel is easy to depict, the road ahead will be a bumpy one. For instance, how can providers ring-fence their high margins in view of the rise of Intelligent Automation? Flipping it to the more positive side, the testing community should provide a much more proactive approach in guiding clients on how to test innovative products and offerings that can be As-a-Service propositions. Take RPA and Autonomics as an example: Testing these highly industrialized offerings is paramount, but I have yet to hear how the testing community will rise to this challenge or grab the opportunity. Similarly, in the context of “digital transformation,” the community should switch from reactively stating that it supports mobility, cloud, social and analytics to outlining how it will support business transformation. Much of this is about cultural change. And we are looking forward to engage with the community around exactly these challenges.

HfS readers can click here to view highlights of all our 22 HfS Blueprint reports.

HfS subscribers click here to access the new HfS Blueprint Report: Application Testing Services 2015

Yes, I have been trying hard – and failing miserably – to avoid using the term “Uberization”, but it’s everywhere! Even in the analyst business, where the sharing platform is the Internet and any old whackjob can get in on the act. All you need is a computer and an ability to write remedial English.

The technology and services industry today is awash with individuals whose only professional activity is flitting from vendor conference to vendor conference, with the sole purpose of writing completely non-objective puff pieces praising their vendor hosts in exchange for money (or in the hope said vendors will pony up some dough in gratitude). Vendors are only too willing to pay these people’s travel expenses, in return for such a willing and compliant audience.

Now, there is nothing wrong with this, in today’s free-for-all economy, as long as these individuals stop masquerading as analysts. I can’t proclaim I am a professional accountant, lawyer or hip-replacement specialist, without proving to the world I am trained and can deliver those services adequately, so why should we allow these people to call themselves analysts, when they are not. Do these vendors hire these fake analysts to do real strategic work for them? Of course they don’t – they use them as marketing advocates, and pay them as such. So let’s call them what they are: Vendor advocates.

We need to settle on this correct term for these fake analysts

Once we can all settle on that term, then we can all stop complaining about their tactics, crying foul when we see their blatant pay-for-play. Once they are officially branded as vendor advocates, then they can rent themselves out as much as they like to marketeers willing to buy their services, without having to masquerade as something they are not.

I know several of these individuals (and I am sure most of you do too). They never produce any real research (most simply do not bother doing any and hope noone notices), they usually have limited knowledge (because they do no research) and love the sound of their own voice. Some even plagiarize, make up data and fake surveys (but let’s not go there right now…). However, there is a role for these individuals in the world, but let’s just stop pretending they are analysts.

These vendor advocates play an important role supporting the industry – as long as they are correctly branded as such

But it’s not all bad – these vendor advocates really do have a purpose – they are helping marketing execs in technology and services vendors validate their offerings. They are helping out those frustrated marketeers who do not want to pay the exorbitant prices of the traditional research shops, and simply want to pay someone posing as an industry “expert” to express how wonderful they are.

And there is nothing wrong with this – companies have to pay to advertise to sell product – it’s been going on for centuries. If you are selling technology, you need to hire people with writing skills to communicate to the world that your products and services matter. So why not outsource to someone outside your firm who is at least pretending to have an objective viewpoint?

Bottom-line: You can be a great Vendor Advocate and be loved by industry. So be proud of it, but don’t expect analyst credibility

Anyone who appears in a TV commercial, or writes an advertorial column in a magazine, is an advocate for the brand paying them. It’s credible – for example, you see pro golfers advertising all sorts of products and services on their shirts and visors, but we aren’t offended. Noone cares whether Phil Mickelson uses KPMG to audit his accounts, or whether Shaq O’Neill really does use Gold Bond, or whether Roger from Madmen drives a Lincoln MDX… we love these personalities and our attention is drawn to the products and services they are marketing. It’s the same for marketing advocates – many of these individuals are great people with lovely personalities… there’s nothing wrong with marketing someone’s products or services, just don’t pretend you’re an analyst when you do it!

Sangita Singh is Chief Executive, Healthcare & Life Sciences, Wipro (Click for Bio)

I recall when I founded HfS Research nearly six years’ ago, one of the first people to visit our offices was the calm, but tenacious Sangita Singh – one of the most recognizable and popular faces of Wipro over the last decade.

Since then, Sangita has made a regular habit of visiting us at HfS during her analyst rounds in the Massachusetts area – a location right at the heart of many of her life sciences and healthcare clients. And what amazes me about Sangita is the fact she manages to (somehow) live simultaneously in both Manhattan and Bangalore at the same time, in the midst of all this merger-mania in healthcare.

While Wipro has built a reputation for helping to drive cost savings and provide IT and business process support and capability, Sangita is on a mission to take her firm’s healthcare solutions to the next level, by working with clients and partners to build connections between the many silos in today’s US healthcare system. At the heart of it is how to better serve the patients with the right combination of services and technologies in a more simplified and accessible way. It requires a different way of working both within Wipro, and with clients. It’s a big, bold dream, but that’s what gets her excited.

So when we convinced Barbra McGann to join us to lead our analyst coverage of healthcare and life sciences, I couldn’t resist introducing her to Sangita… and lo and behold the two of them cooked up a little interview for our reading pleasure…

Barbra McGann (Managing Director, Research at HfS): Sangita, your career has lately been a smorgasbord of specialized leadership roles, from an education in engineering, to most recently at Wipro as Chief Marketing Officer, then Head of Enterprise Application Services (EAS), and now, Chief Executive of Healthcare and Life Sciences. What is your approach to tackling each of these very different areas of expertise as a leader?

Sangita Singh (Chief Executive, Healthcare Life Sciences & Services at Wipro): Hi Barbra – it is to be open to listening and learning—from the team, from peers, from management, from the external environment, and to be inclusive. One thing that defines me is my curiosity—my willingness to not take myself too seriously and be willing to learn from anybody and everybody. That provides the input. Then I do three things: First, I carve out a really audacious big bold dream that can be called strategic vision, that I remain consumed by. Then I try to spend hours and hours getting my entire team inspired and on the same page with respect to that dream. Therefore, the second aspect is gathering, garnering and building a team that lives that dream and I think is better than me to be able to execute on that dream. Thirdly, I focus on execution or whatever we have committed to make it happen for my customers, and for my people as well, within Wipro.

Barbra: It sounds like you’ve created an ideal triangle—vision, team, and energy for execution—to apply to healthcare, where there is such an opportunity for change. In general, people have a poor view of healthcare, often describing it with terms like “confusing,” “red tape,” and “expensive.” What’s your vision for the future of healthcare?

Sangita: Fundamentally, Barbra, healthcare is about enriching people’s lives. Clearly, the industry is going through a huge disruption and a lot of transformation in the way healthcare will be delivered, the way it is accessed and how affordable it can be. There are three mega trends that we think are shaping the direction. One is clearly patient empowerment, which includes how patients access and use information through digital technologies. The second is the pay for performance revolution that we are seeing in accountable care organizations, and with population health management to drive the accessibility, affordability, and quality of care. Finally, the third important piece is digitalization, the rapid adoption of which will allow a patient-centric platform to give new access to customers through mobile, cloud, and 3D printing.

Barbra: Technology can be a great enabler, as you know, Sangita. How do you seeing it playing a more effective role in changing the way healthcare is perceived to be more about enriching people’s lives?

Sangita: 32 million new people are coming under the coverage driven by Obamacare. A lot of that is Medicare. In Medicare we have a Software as a Service platform that allows access to people, that allows eligibility, enrollment, and revenue reconciliation to be done through that one platform. Secondly, we are able to build analytics to drive population health management through patient engagement. Finally, in the Medicaid space, we are working with modern platforms that can drive all the business objectives that are relevant for the new Medicaid priorities such as dual eligible. Therefore, we are helping our customers in two ways. One is around changing their business models—how do I digitalize them better? And the other one is as far as the run is concerned—how do I drive automation and application and infrastructure support to run organizations more efficiently?

Barbra: How would you sum up your vision for the role of Wipro as a business process outsourcing services provider in the emerging As-a-Service Economy?

Sangita: Our vision is to build a patient-centric interconnected health ecosystem through solutions and platforms at the intersection of payers, providers, life sciences, and medical devices. I think the big role that we can play is to be able to create the interconnections in the healthcare ecosystem. This used to be fairly siloed. So medical devices would operate in isolation with the patients or largely with the providers. But today with the patient at the center of everything there is a need for the data to get connected, there is a need for interactions to get connected, there is a need for engagements to get connected. We can provide systems, services, and IT that can enable this. To build a very patient-centric interconnected health ecosystem is really our big dream.

Barbra McGann is MD Research, Healthcare and Life Sciences, HfS

Barbra: Sangita, this is some significant change we are talking about with interconnections and digitalization. It’s going to take another many-syllable word: re-imagination—stepping outside of what is it that we are doing day to day, reminding ourselves that this is really all about the patient and considering how create the right process to get them to the health and care they need at the time they need it in way that they can afford to pay for it, or get help to pay for it.

Sangita: And the word that you used, the reimagining, is the most powerful part. Across every process thanks to digital technology at the front and automation at the backend, really every process that touches the patient can be reimagined. And that’s really in essence the huge opportunity that lies before us.

If you see the number of startups that are there that are leveraging cloud in the form of digital technologies and disruptive traditional business models, it’s just astounding. I was just reading about a startup (Theranos) started by Elizabeth Holmes, which could disrupt the diagnostics business, using a drop instead of a vial of blood for tests and taking lab reports on line. So cloud and digital is reality.

I think is very exciting for new age providers like ourselves because of the opportunities it provides and therefore levels the playing field for all. Because it’s new it would be the same for IBM, it would be the same for Accenture and the same for us. So that’s what’s exciting. I think cloud is the best disruption to have happened for any new age service provider.

Barbra: Earlier, you mentioned analytics. Will you tell us a little bit about how Opera plays a role in analytics for Wipro and its clients? It was a big announcement and a very strategic move for Wipro to invest in Opera. How this is playing out in the healthcare industry? What role do they take in helping to realize the vision?

Sangita: Opera has been an interesting partnership. What Opera was known for was building algorithms used in the payer and provider space: in the provider space for revenue leakage, utilization of hospitals, and in the payer space for fraud and abuse detection. They had a number of use cases for payer and provider. Now we are working with them to build use cases for life sciences, largely in the R&D and clinical trial space.

We have also used Opera on the backend for all the service desks supporting business process outsourcing. We leveraged Opera to drive analytics that can help us drive better user experience and a quantum jump in productivity.

Barbra: It sounds like there’s quite a bit going on with clients directly, as well as internally, on Wipro’s own processes and activities around outsourcing services.

Sangita: They have data scientists who can build algorithms that can detect patterns, remove false positives, so on and so forth… really almost any business problem. The constraint that we have if any, Barbra, is Wipro having access to customers where they call us in assuming that we can help them with their business problem. Our brand is more synonymous with cost takeout. And so that’s a big constraint. But once we have worked with a customer and have gained their trust and confidence, then we move forward and proactively propose value added propositions like what we can do with Opera – this is how we define success.

Barbra: Certainly a key change we have seen as the sourcing industry has matured, Sangita, is that partnerships between service buyers and providers bring more long term value to both parties where trust has been established. You have said that personal interaction and networking is incredibly critical. What would you recommend being effective this way in networking?

Sangita: It’s important to learn from anybody and everybody, Barbra. Thanks to the digital world we are no longer as siloed as we were before when you could network only by meeting people physically. Now all of that has been disrupted and you can meet anyone, anytime virtually. In addition, you know there is so much access and information that you can have about who to connect with and how to connect through social media.

Each one of us is unique and we hear and have read this a dozen times but yet we do so little about it. Each one of us is passionate about something, and we have the opportunity to be a thought leader in that area. And I think one should always go out there and network and be known for something. I am still not there 100 percent but it is definitely in one my strategic to dos. And I am learning hard from the millennials on how to get really active and relevant and sort of cool in the digital world as well.

Barbra: You have inspired me to do that, too, Sangita! Thank you so much for sharing your passion for patient centricity and Wipro’s role in helping healthcare and life sciences companies achieve it. We will be watching for more of it online @sangitasingh101 and @wiprohealthcare.

The As-a-Service Economy is all about achieving the outcomes we most want with a great service experience. So let’s look at how to avoid that not happening and becoming legacy businesses that failed to stay ahead of the demand curve.

The perfect anti-example is Subway. Back in 2001, the release of Fast Food nation shocked much of the Western world into realizing we were slowly killing ourselves on pink-slime infused fast food. It was great for Subway as it sold sandwiches that – for all intents and purposed at the time – we thought were a far healthier option than Burger King. And it seemed to taste OK too…

Fast forward to today – people are increasingly aware that chemically-preserved fake colored bread, cheap antibiotic-induced meats and pesticide-flavored vegetables aren’t much worse for you than a greasy concoction of pink slime, protein and french fries.

Coupled with this is the service experience – I accidentally ventured into a Subway the other day (one of those once-in-every-five yearly visits, where you are just so damn hungry and want to avoid the golden arches). The only desired outcome is to subdue hunger – in the vain hope it may be a somewhat enjoyable experience in the process. To cut the the chase, the restaurant was filthy – every single table was covered in food remnants, the toilet stank, the staff were curious life forms from some distant planet… and the sandwich was just lame. Net-net, I had just about achieved the outcome I was looking for, but the service experience was horrible. I will not venture back for at least another five years. Hopefully never.

On the flip side, if my desired outcome was to have a tasty fast-food burger – and to hell with the consequences – I would just have had one. I know exactly what to expect and the experience and outcome is clear – unhealthy tasty food that is enjoyable and fills the hunger hole. So contrast the two outcomes – a nasty sandwich versus and tasty enjoyable burger, that is probably only 10% more unhealthy (source HfS, 2015).

The Bottom-line: Once you lose touch with your customers’ desired outcomes, do something fast to find them again, or resign yourself to a slow extinction

Yum

I don’t want to spend hours reviewing Subway’s income and profitability, as I am sure they have their quarterly accounting revenue model down-pat – they sell cheap(ish) food to people who probably don’t care that much about food, and don’t have much understanding of what bad food chemicals can do to your insides.

But I am sure that even many of their loyal customers are slowly wisening up to the experience, and the brand will eventually need to do something radically different to continue its existence – their stuff just doesn’t taste as good at their nemesis alternatives and it’s not even good for you.

The answer is quite simple – how can they produce a healthier, better tasting product with a less crappy service experience. Oh wait – Starbucks has already figured that out and you can even get a better meal in a Dunkin Donuts or Tim Hortons these days (and that’s saying something). Sorry Subway – you’re legacy and probably confined to the once-great corporate successes that failed to evolve its services experience to meet changing customer desired outcomes.

Automation hype and anxiety is everywhere today. In fact, haven’t you been amazed by the emergence of all these “automation experts” that have suddenly appeared on your LinkedIn recently? It’s as if these people went to school 20 years ago with the sole purpose of becoming an automation expert…

Automation hype and anxiety is everywhere today. In fact, haven’t you been amazed by the emergence of all these “automation experts” that have suddenly appeared on your LinkedIn recently? It’s as if these people went to school 20 years ago with the sole purpose of becoming an automation expert…

When we coined the term “The As-a-Service Economy” a year ago (remember our famous

When we coined the term “The As-a-Service Economy” a year ago (remember our famous