How many times do you have to scream at people to make them realize that they will never be successful tinkering with shiny new automation tech tools if that cannot design end-to-end processes that achieve their desired outcomes? Automation tools can truly help make processes work effectively across disparate systems, once you have got rid of the awful process debt weighing down your organization.

So what, exactly, is “process debt”?

When you are head to head with competitors, you must have your business processes designed on solid ground to accelerate the delivery of value – using technology and integrated automation to connect the dots.

Tech entrepreneur Ben Horowitz quoting Shaka Senghor, who he considers the CEO of a prison gang, in What You Do Is Who You Are, sums it all up perfectly… “Imagine you’re a developer and someone says, ‘Here’s some land, and here’s a million dollars. Could you build me a house on this land?’ So you build this guy’s dream home. And he moves in and then his family starts getting sick. Because what they didn’t tell you is that the land is toxic and it was a f***ing dump site …Nobody was digging into the dumpsite itself.”

Net-net, technology isn’t necessarily the heart of making the connections from front to back – it’s making good choices about what you automate and having the business process in place to back it up.

You can read more about our recent HFS Leadership Roundtable here, where we got deep into the weeds of process debt issues.

Of course! Ginni was driven out because she failed to get the Blue Prism deal over the line, and Arvind is now in the hotseat to make damned sure they don’t miss out on UiPath…

Of course! All this “hypercloud” nonsense and the $34bn of loose change they dropped on Red Hat was just a diversion from their real intention… to make IBM the Big Blue RPA monster!

In all seriousness, we were speculating about IBM and Blue Prism during RPA’s infancy in 2016 (see blog)… and while it made sense back then (and at a far cheaper price tag), it sure doesn’t make any sense now. SAP, Microsoft, Pega, IPSoft and Appian have all made modeinvestments to have their own RPA capability, and all of them chose either very small scale acquisitions or developed it themselves (in Microsoft’s case). I also fully expect Salesforce and Oracle to tick the RPA box at some stage, but it is highly unlikely to be with one of the big three with a nine-figure price tag.

Now there is a small chance I could be wrong and IBM has suddenly decided to take the plunge several years too late, but it really makes no sense at this point.

Gini Rometty, the queen of Big Blue is stepping down after a turbulent few years at the helm, where her “imminent” retirement has been one of the industry’s most discussed topics since the failure of Watson to reach its early potential. However, the rapid shift in direction towards hybrid cloud – with the Red Hat acquisition just over a year ago – has rapidly paved a new direction for Big Blue and, perhaps, leaves Gini with a lasting legacy that won’t be all about her supercomputer that found fame on Jeopardy!

The appointment of Arvind Krishna, the architect of IBM / Red Hat, signified its full-throttle scramble to take the Global 2000 into the hybrid cloud

And in here place steps up the head of the firm’s cloud business, with Jim Whitehurst, the CEO of Red Hat, moving in as president, but more significantly, Arvind Krishna, IBM’s architect behind the deal, being voted in as the new CEO. With Krishna being the brain behind the Red Hat double-down, he knows how to take the calculated risks which IBM must take if it’s going to turn the aircraft carrier around. Moreover, he can move fast, with the Red Hat play being barely more than a year old and the emerging IBM cloud business quickly becoming the most coherent and unified of all its business units that HFS has encountered.

This speed and clarity of direction speak to Krishna’s ability to pull what was a rapidly evolving team together with a clear mission and vision. Again, if he can replicate this at scale across IBM, it might be able to solve the firm’s biggest challenge – rationalising a sprawling estate that has been left to grow wild for almost a decade.

Hybrid Cloud is where IBM has made its bed, and the new IBM leadership team is determined to take full advantage

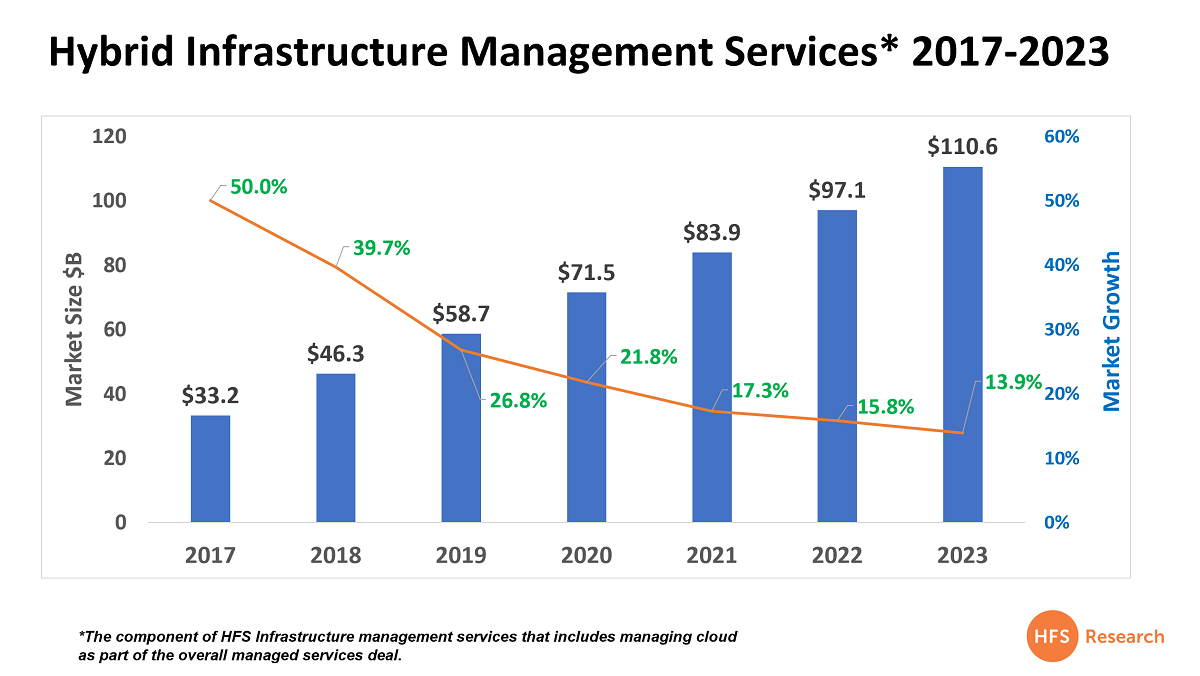

New HFS Research shows this market is expected to ratchet up by more than 20% this year to $72 billion as the market for hybrid private/public cloud becomes the most vital progression corporation need to make to scale and survive in today’s global digital business environment:

Source: HFS Research 2020, Click to Enlarge

While all the cloud talk has been about the rampant growth of the digital juggernauts Microsoft, Amazon, Alibaba and Google, no one has stepped up to support complex hybrid public/private cloud transitions better than IBM in recent times. It’s one thing providing the capacity, containerization and scalability, but another to layer on all the global support to tackle the complexity of integration with corporate legacy IT systems, along with all the ongoing support and security needed to manage this transition effectively.

The new leadership must unite the warring factions within IBM

IBM’s new leadership team has a wealth of experience and can reverse the fortunes of the firm – but they have their work cut out for them. It may have been the king of the services market a decade ago, but the firm has been too pre-occupied with siloed business units scrabbling around on their own initiatives trying to be the next big thing. Over the years, IBM has moved from a trusted dominating force to a whale gradually bleeding out as IBM Watson became somewhat less relevant in a world where business leaders were struggling to make RPA work, and newer faster rivals in the mid-tier started eroding their market share with competitive pricing and flexible delivery. Above all, IBM needed a clear vision, one that cuts through the digital drivel that pre-occupied buyer mindshare. And sadly, that just didn’t come under Rometty.

Battling the complexity of IBM is something clients of the firm tell us is a major inhibitor to contract growth. Disparate sales and delivery teams make it, at times, impossible for clients to expand engagements into new areas and as analysts, we’re often told ‘seriously? I didn’t even know they did that?’ when we talk about IBM’s broader capabilities. If the new leadership team are going to reverse the fortunes of the leaking oil tanker, they’ll need to address this first. And can do so by implementing the following:

Incentivizing sales teams to cross-sell across the whole of IBM’s services. Clients don’t care which business line recognizes the revenue or which sales team gets the commission.

Build a layer of consulting as the window to the rest of IBM. Simplifying a complex and sprawling empire will take time, and while important won’t change quick enough to match buyer expectations. Building genuine service-agnostic consulting capabilities to lead engagements across IBM will go along way to plastering over the cracks while the rest of the business is modernized.

Loosen the purse strings and be prepared for flexibility. The services ecosystem has changed rapidly, and IBM’s now competing with firms willing to take a gamble on client engagements and offer flexible pricing models. IBM can’t rely on its reputation alone to compete anymore, and must be willing to invest in clients and take risks – at least to a greater extent than it has in the past.

IBM has a powerful reputation – but this is no time to be complacent

The phrase ‘nobody got fired for bringing in IBM’ has been a boon for the firm and isn’t far from reality. The firm’s reputation for delivery and innovation proceeds it which means sourcing teams get off the hook, even for disastrous engagements. But over time even this lofty position has become hard to maintain as a new generation of buyers pours into senior positions and competitive pressure force enterprises to look for partners outside of the usual suspects.

The new IBM leadership team has a unique opportunity under Krishna, to re-position IBM in the market as a dynamic and modern services firm, leveraging its heritage brand and reputation to push a clear message. If you pulled a representative sample of the market and asked them what IBM’s strategy is, its vision for the future is, or even what their big bets are, you’d be met with stony silence. IBM must urgently figure out what its story is, and what it wants to be in the future if it’s to claw back its position as the IT Services firm of choice.Is the new leadership team a warning shot for the hyperscale cloud giants?

In cloud, however, IBM has always had a relatively consistent story, supported by an enviable track record of delivering complex infrastructure services to clients. While the emphasis on public cloud pushed IBM out of the limelight as executives piled into hyperscale, IBM has made a killing pulling together the full-stack enterprise infrastructure. The Red Hat acquisition showed IBM was ready to put its money where its mouth is and commit to targeting the hybrid cloud market – a rapidly growing segment as the lure of ‘cloud only’ and ‘all-in-with-AWS’ became recognized for the fantasy that it is for most enterprises.

The debate will no doubt rage on over whether IBM has a place amongst the hyperscale firms – AWS, Google, Microsoft, and more recently Alibaba Cloud. Whether born-in-the-cloud purists like it or not, IBM’s infrastructure and enterprise cloud business puts it firmly in with the biggest of the bunch on PaaS revenues alone. The Red Hat acquisition in 2018 bolstered this even further and fired a warning shot in an already punishingly competitive cloud war.

The new leadership team can bring a level of focus and commitment to cloud – with senior representation from IBMs Cloud Business in Arvind, and Jim from Red Hat as President. With this combined experience and a commitment to hybrid cloud, there’s every likelihood IBM is in a position to bite a huge chunk out of one of the fastest-growing enterprise services segments. And while it’s unlikely IBM will need to go to war with the major cloud giants to make its mark – the hyperscalers would be wise to watch the new strategy market out by IBM’s new leaders – this may be the most valuable partnership they ever have.

Bottom Line: The change in leadership will provide the jump-start IBM desperately needs to survive this punishing services market

Gini stepping down is a big moment for IBM – She has had her hand on the tiller for close to a decade. But IBM has continued to struggle to return to growth, even with a reputation and trust in the market that it’s peers envy. The new leadership must leverage this reputation, and return some meaning to the brand – by swiftly unifying disparate IBM functions and modernizing the structure of the sprawling business. IBM simply cannot survive another 8 years of tumbling revenues.

We can finally draw a line under the market that was RPA as we transition to the broader value of integrated automation, AI and analysts solutions (the “HFS Triple A Trifecta” – see definition below):

Our analyst team conducted the most exhaustive research process ever conducted in this space… here’s the overview:

RPA Customer Experience Survey. HFS fielded a detailed RPA satisfaction study with 255 super users of RPA (enterprise clients and product partners) that yielded 311 product ratings across 30+ CX dimensions

Detailed References. HFS conducted reference checks with 75 active clients of RPA product companies, including detailed interviews with ~20% of the sample

RFIs. Each participating vendor completed a detailed RFI

Vendor briefings. HFS conducted briefings with executives from each vendor

So without further ado, let’s hear from our lead analyst, Elena Christopher, for this Top 10 exercise:

Phil Fersht, CEO & Chief Analyst HFS Research: Elena… 7 years on, is the RPA bubble bursting or is something else happening?

Elena Christopher, SVP HFS Research: In 2012, HFS launched the concept of robotic process automation (RPA) to the world via a seminal report and blog. In the seven years since, the ugly truth is that we’ve simply succeeded in using RPA to move data around enterprises faster with less manual intervention rather than to rewire our business processes and create new thresholds of value. We are largely missing the opportunity to transform business operations. RPA gets loads of guff for creating technical debt. But the reality is that it has the potential to clear enterprise decks of years of process debt! Process transformation is the still unfulfilled mission. As we said last year, RPA is dead, long live integrated automation platforms. RPA alone is a great tool. But no singular tool can deliver broad transformation. As I’ve been saying of late, RPA needs friends. Sort of my own weird children’s show – RPA bot, cognitive capture, machine learning algorithms, APIs etc all work together to reinvent processes and create value. But honestly this is just another way of reflecting our Triple-A trifecta of automation plus analytics plus AI. Powerful alone, but better together.

With transformation on the brain, we focused our 2019 RPA Software Product Top 10 on how the RPA product companies are supporting and enabling their clients to scale their automation programs and drive real change. We looked at our normal mix of execution, innovation and voice of the customer criteria with special emphasis on factors such as customer scale, richness of ecosystem partners, product roadmap and R&D, embedded intelligence, and ability to drive business outcomes.

We expect that vendors can talk well and compellingly about their capabilities, thus we also conducted deep due diligence with their customers to get a straight story

What stood out during the Top 10 analysis? Who are winners and who needs more development, Elena?

Well before getting specific, the most important point to make is that no single RPA software vendor is truly leading compelling process transformation at scale. Those that are headed in the right direction have clear roadmaps and deliver enhanced product functionality that clients need to grow their automation programs, have strong ecosystems of well-trained implementation partners and technology partners that extend functionality, and they focus on driving success beyond the sale. Technology may be the enabler, but getting companies to change how people work and processes are executed is tough business.

Now for specifics – Overall, the big three (Automation Anywhere, Blue Prism, and UiPath) all had a strong showing. Automation Anywhere prevailed overall buoyed by a decent base of scaled, or perhaps more fairly, scaling customers. Of the big three, they offer the most native capabilities and have actively been working to address unstructured data for a few years. UiPath, who was the media darling of 2019, came in second overall. While they are doing many things right, its lower level of scaled customers and unrealized vision for the future of RPA set them back. Blue Prism took the three spot. While it exceled at execution, it fell behind in innovation criteria after a year of major announcements but limited actual impact on clients.

While we share overall rankings, the goodness is really in our subcategories where we showcase different facets of each provider’s strengths. This is our “choose your own adventure” approach to rankings. Consumers of this report can leverage the overall rankings or review the subcategories that are most important to their business needs. For example WorkFusion and AntWorks were recognized as leaders for their embedded intelligence. Kryon and Softomotive were recognized for their ease of use, NICE and Pega snared the top spots for delivering business outcomes, and EdgeVerve was a leader in security and governance.

So what’s your expectation for this market as it matures? Are we settled with the key players, or do you expect this market to turn upside down? What must these current firms need to do to survive?

RPA really is the gateway drug for AI and cognitive tech. As we move deeper into 2020, we expect to see more examples of Triple-A trifecta integrations emerge. Right now most enterprises are Frankensteining these, piecing together various tools and components to create the solutions they need – either directly or with service partners. We’ll see more integrated platforms come to fruition – some natively developed and some acquired a la Appian’s acquisition of Jidoka earlier this year. We’re also keeping a close eye on enterprise software vendors like Microsoft who announced Power Automate as its entry into RPA and let us not forget SAP bought Contextor in late 2018.

Meanwhile, enterprises can take a gander at our RPA Manifesto for Success for the Next Seven years. Among the recommendations, it reminds us that technology alone cannot drive business transformation.

Great insights Elena… Now have a stiff drink =)

Damn dry(ish) Jan!!!

Appendix

The Trifecta elements intersect with each other. While each element of the Trifecta has a distinct value proposition (RPA drives efficiency, Smart Analytics improves decision-making, and AI can solve business problems), there is increasing convergence between the three elements. For instance, smart analytics are increasingly reliant on AI tools such as NLP to conduct search-driven analytics, neural networks to do data exploration, and learning algorithms to build predictive models. In fact, the Holy Grail of service delivery transformation is at the intersection of automation, analytics, and AI

The Trifecta is nonlinear without a definite starting point. Transformation is not a linear progression. Enterprises can start anywhere across the Trifecta. It is not necessary to start with basic automation and then advance to AI-based automation. However, it is critical to understand the business problem that you are trying to solve and then apply the relevant value lever or a combination of value levers.

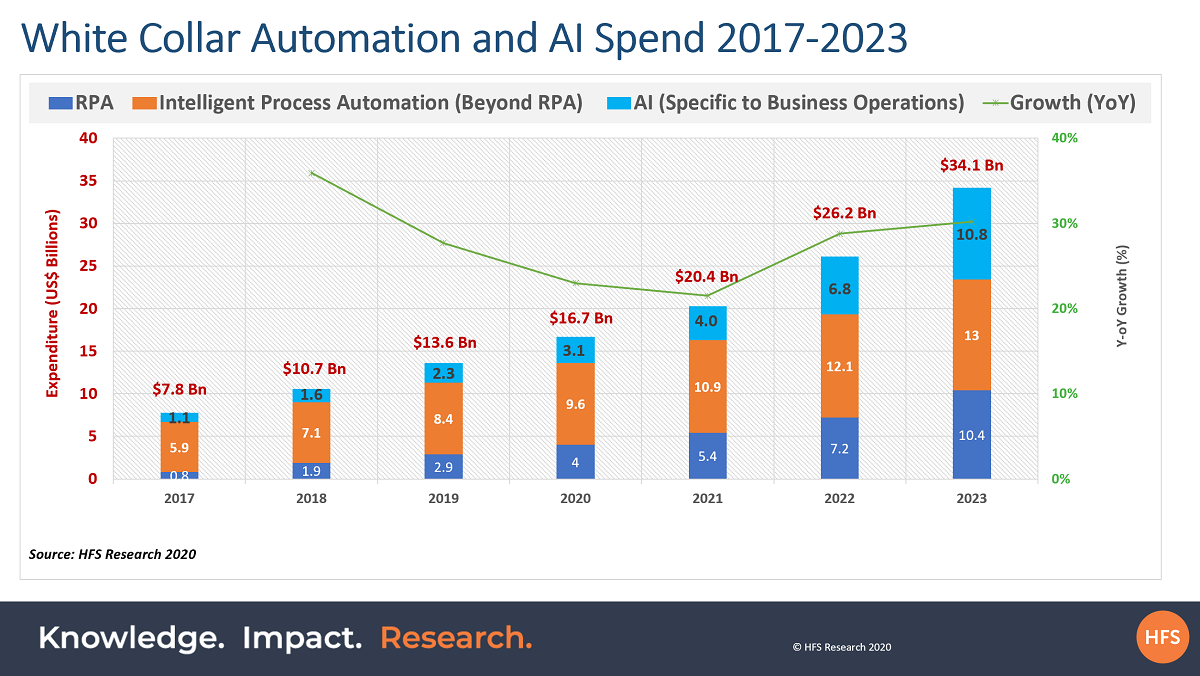

So it’s taken seven years since HFS introduced RPA to the world, lots of blown investor cash, many failed careers, so many great parties and declarations of death for the industry that is, in reality, White Collar Automation and AI, to find a rhythm and a real sense of purpose.

While we can argue the oddities and vagaries of what is essentially attended desktop automation (which isn’t really robotic as you need someone there to keep it functioning), plus the original concept that was real back office unattended robotic process automation, we can celebrate the fact that “RPA” is a $4bn industry today, that has helped drive a further $9.6bn in incremental internal and external expenditure on what we are terming “Intelligent Process Automation”. IPA caters for the process transformation, discovery, mining, data ingestion, computer vision, NLP etc that truly supports that broader automation and AI strategy across business silos:

Ultimately, what we are talking about here is the whole digitization, automation and self-learning data intelligence that is changing how white collar employees conduct their jobs. So how is this burgeoning white collar automation and AI market redefining itself?

Robotic Process Automation (RPA): RPA is inherently capable of recognizing and adapting to deviations in data or exceptions when confronted by large volumes of data. In effect, it can be intelligently trained to analyze large amounts of data from software processes and translate them to triggers for new actions, responses, and communication with other systems. RPA describes a software development toolkit that allows non-engineers to quickly create software robots (known commonly as “bots”) to automate rules-driven business processes. This includes Robotic Desktop Automation (RDA) which is essentially surface automation, where desktop screens (whether desktop-based, web-based, cloud-based) are “scraped”, scripted and re-programmed to create the automation of data across systems. A well-designed RDA solution can automate workflows on several levels, specifically: application layer; storage layer; OS layer and network layer.

Intelligent Process Automation: is the use of technology to allow a business function or part of the operation of a process workflow work automatically that is not enabled by RPA technology. It includes the use of process mining and discovery, BPM suites, data ingestion, machine reasoning, cognitive machine reading, automated chatbots, OCR, IVR, document process automation, and related technologies.

IPA comprises of two core elements:

i) External professional services: Relates to all external spending focused on developing business process automation strategies / roadmaps and the use/ implementation of automation with business functions.

ii) Internal operational spend: Includes internal and external spending on automation – change management, IT and operational teams focused on process automation and automation use as part of existing business process management initiatives.

Artificial Intelligence (AI): refers to the simulation of human thought processes across enterprise operations, where the system makes autonomous decisions, using high-level policies, constantly monitoring and optimizing its performance and automatically adapting itself to changing conditions and evolving business rules and dynamics. It involves self-learning systems that use data mining, pattern recognition and natural language processing to mimic the way the human brain works, without continuous manual intervention. It includes cognitive (digital) assistants, AI Watson-type reasoning apps, Natural Language Processing, Machine Learning and Computer Vision.

The Bottom-line: RPA has opened the gateway for augmenting White Collar roles, now we’re progressing far beyond that

C’mon folks, it’s time to quite the ‘bot for every desktop’ claptrap and focus on the real what next. With firms like Microsoft, SAP, Appian, and co now offering RPA and much cheaper prices, the value is shifting firmly to the broader automation driven transformation that is enterprise-grade, involves both business and IT leaders, scalable in the cloud, and truly capable of augmenting human workers. Yes, RPA provided a gateway to many new possibilities… and now the gate is firmly open, the horses are bolting! Now catch them, tame them and ride them to the AI promised land =)

The recent HFS predictions for 2020 boldly state that none of the big three RPA vendors will get acquired this year. By logical extension, this means smaller and less expensive RPA vendors have a higher chance of exiting to the comfort of bigger players with broad shoulders and deep pockets, especially where they fit a pressing market need and round out an existing integrated automation proposition. HFS also predicted the continuance of technology convergence as low-code / no-code platforms continue their surge.

Barely days into 2020, Appian, a low-code development platform vendor, announced the acquisition of Novayre Solutions SL, the developer of the Jidoka RPA platform. Appian recognized relatively early the complementary nature of BPM and RPA, establishing partnerships and agnostic no-code integrations with Blue Prism in 2017 and later with Automation Anywhere and UiPath. Now it has its own RPA and it’s talking about a compelling pricing strategy for its enterprise customers to boot. We’re curious to see how the dust will settle here with the “big three” RPA leaders.

Appian probably snagged a bargain here, in comparative RPA vendor purchase terms

Financials were not disclosed, but it’s likely this acquisition is at a very favorable price for Appian as compared to the astronomical valuations of some of its RPA brethren. Despite being on HFS’ radar in recent years, it was becoming increasingly hard to see noticeable progression in terms of Jidoka’s customer base and ecosystem development. So, it comes as little surprise that Jidoka was keen to sell. Appian is one of the low code players that actively embraced RPA as part of the overall conversations they have with customers about process automation. It describes Jidoka as the platform it would have built itself if it were building an RPA platform, citing its proven strength in unattended automation coupled with attended (albeit nascent) capabilities, along with its cloud-native development and java architecture.

Hailing from Seville Spain, with less than 20 employees, Jidoka’s customer are mostly small and midmarket firms spanning financial services, outsourcing, utilities, consumer products and other broad markets in Spain and Latin America (Jidoka robots operate in Spanish and English). A notable big logo client, Pepsico, uses Jidoka’s RPA in its finance department.

Appian RPA will come as an additionally priced feature of the Appian platform

Appian will rebrand Jidoka as Appian RPA once the acquisition dust settles. Much of rebranding effort has in fact been completed before this acquisition announcement in the months since the letter of intent was issued. There are no plans to launch it as a standalone feature or product, so don’t anticipate a pureplay RPA product coming from Appian. Existing Jidoka customers will be supported whether they are using Appian’s other products or not. One of its immediate integration priorities is with its recently launched Robotic Workforce Manager.

Appian RPA will be offered as an add feature for Appian Cloud platform customers for $5,000/month maxing out at $60,000 / year for unlimited use. This should be attractive at the enterprise level, especially to those looking to use RPA extensively. More importantly Appian can’t lose out with this pricing strategy as it is guaranteed the license revenues from the Appian platform itself, which are applied per user, per application.

The Bottom Line: Long live integrated automation. Appian’s acquisition of Jidoka is the latest example of the push towards full stack automation.

Low-code and RPA are a solid tool combination to tackle process automation, with each hitting their own sweet spots. Appian has born this out via partnerships over the past couple of years. We expect to see more examples of it in action as organizations progress their journeys beyond initial RPA-in-isolation piecemeal attempts into organization-wide impactful automation programs. While RPA has been dominating conversations around process automation for the past several years Appian is seizing the opportunity to bring low-code and RPA together. Its inherent process automation capabilities are complemented by RPA for hard to reach systems and as an alternative route instead of API development when speed is needed.

We see this acquisition as evidence of push towards what HFS terms the Triple-A trifecta of automation, AI and analytics into integrated automation. The BPM and low code players were super sane about embracing RPA rather than fighting it. And we see a lot that makes sense in this purchase if everyone can play nice and get along.

This acquisition has similarities with SAP’s acquisition of Contextor in 2018 as a technology tuck in and is closest in direct competitive terms to Pega’s Infinity platform encompassing RPA as a standard capability since Openspan opted to become part of something bigger in 2016. The essence of each is a holistic approach supplementing the rigor of low-code and APIs with the flexibility and speed of automation at the surface level as a tactical tool.

However, Appian will be bumping up against RPA vendors, and how this plays out remains to be seen. Appian says it does not intend to supplant its partners’ (e.g. Blue Prism) technology, but RPA vendor partners will have to make a call on how these relationships work moving forward with an all-important eye on avoiding customer disruption. Coopetition isn’t for everyone. Appian has been through this scenario before with Mulesoft before developing its native integration capability. The integration and shared standards live on but not the formal partnership.

Lord, do we hate predictions. But as analysts we get treated like robots sometimes and are expected to churn them out like some pre-defined analyst chatbot algorithms. So, in robotic fashion, here is a splurge of stuff we think could well happen from the HFS analyst team…

1) The consequences of taking out Soleimani may make all the following predictions moot

This really matters. Just as we were hoping for another year of investor money sloshing everywhere trying to find a meaningful home, the trigger we were dreading that sparks a dramatic finale to this unprecedented 11 years of economic growth may just have been pulled.

Iran’s regime there has little to lose, with its economy in tatters, being reliant on Russian and Chinese imports, it’s people close to desperation. But this is no Venezuela, North Korea or Iraq that can be pushed around at whim… this is a country with a 500,000 strong army now united in this act of war. Iranians for and against the current regime have now united in their desire NOT to have outsiders determine their fate. More dangerously, pro-Iranian and anti-Iranian factions in Iraq who were fighting each other are now bonded together in their one desire that America not decide their fate and get out. ISIS grew out of Iraq the last time we stepped away, and I fear what will grow this time. If intelligence exists that showed an attack was imminent, this needs to be shared now to break this blind unity the US move created. The main point is that the middle east, particularly Israel, Europe and the US are all less safe than they were 3 days ago. We need to learn from the messes we have created in Iraq, Syria, and Afghanistan that if there is not a viable option to form a government backed by the people and the military, then military conflict leads to a situation of less stability for the world – not more.

We must also not underestimate Iran’s cyber-terrorism capabilities – we know they’ve been throwing money at it. They also have good links with North Korea and Russia – both experts at using it (they are also looking to grow their empires in the region, so it’s possible they will lend a hand). Iran knows it couldn’t win a conventional conflict with the west – it will look to fight their war in a way that means it doesn’t risk invasion. We think they will follow in the footsteps of North Korea and look to inflict financial damage, with sophisticated attacks, which will likely further come in combination with the small raiding boats that will look to target shipping. Of course, this may well lead to a ground invasion in any case if the US (and any allies) decide to go for regime-change.

Net-net a major global downturn, which is a likely outcome from a messy widescale conflict where oil prices rocket, confidence tanks and our digital lives get violated, will have a huge impact on how enterprises decide technology and people investments. We’re not even sure many businesses will know how to handle a rapid downturn and simply fold. The global economy sits on the precipice right now as geopolitics and other political agendas dictate behaviours that could have a savage threat on the health of the world… let’s pray this all gets resolved quickly.

2) The Rise of Process Orchestration will fill the void RPA never really filled

2019 marked the year the 7 year RPA hype journey hit a major roadblock after UiPath’s $8m Vegas party culminated in half the firm getting canned the following week. What was left was the void of promise unfulfilled and a market that needed urgent redefinition and a new manifesto. Almost going unnoticed was the iconic process mining firm Celonis raising a colossal $290m series C finding round and Automation Anywhere raking in $290m as part of its series B, notably with Salesforce dabbling in the investment. “Why is this different?”, I hear you cry… well, the discussion noticeably switched to end-to-end process and workflow optimization rather than the whole “bot for every desktop” nonsense. RPA was even touted as “bridging the gap between front and back offices” by Automation Anywhere… clearly a message to excite its new romance with Salesforce and an effort to steer the conversation into more a meaningful, realistic place.

2020 will see a new narrative emerge as smart enterprises explore a broader tool box of process discovery, process mining, process automation and data ingestion to help them orchestrate true end-to-end processes that actually bring an enterprise’s customers, employees and suppliers closer together.

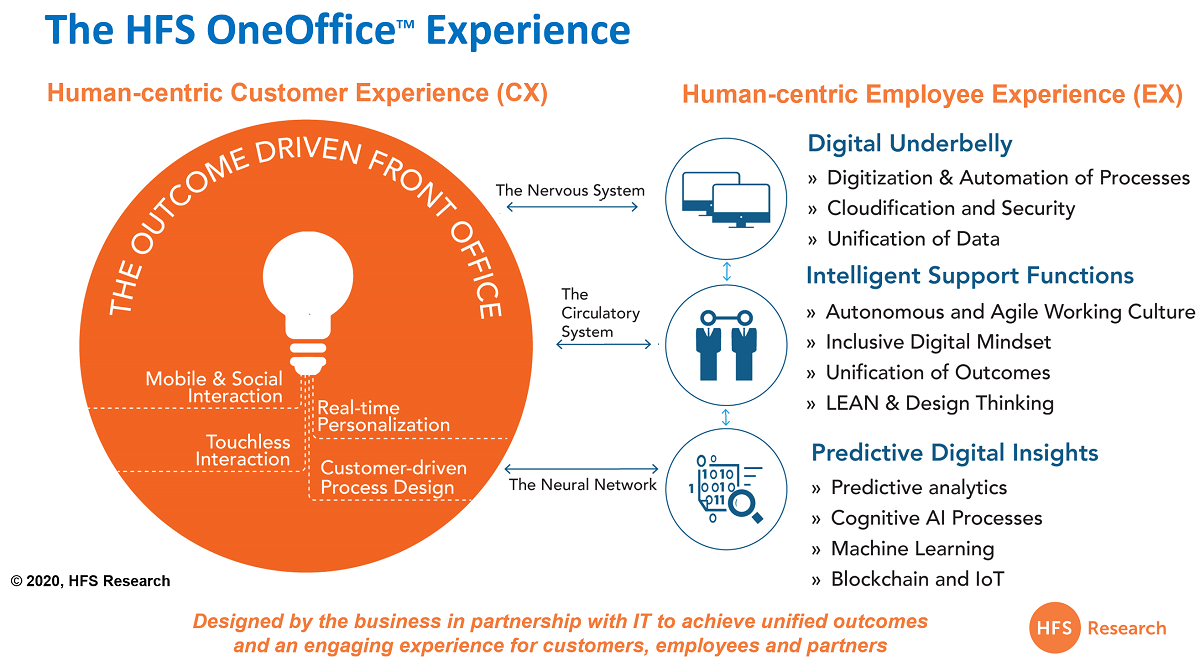

3) The OneOffice progression will bring customer and employee ‘human’ experiences much closer together

We’ve droned on for years now about “Bringing the front and back offices closer together”. 2020 will see this narrative move beyond nice graphics and a narrative that makes back-office people feel more customer-centric, with the focus shifting to enterprises driving an employee experience similar to that of their customers. This entails the use of digital associates for internal needs in addition to “humanizing” digital customer interactions. Customer Experience (CX) will increasingly be considered an umbrella term for the experience interacting with an entire organization, whether it’s the customer, partner, employee or any other entity:

An employee experience (EX) culture is one where people work together shifting from transactional interactions to deeper relationships. Organizations need to ensure they get the balance right; which includes optimizing the use of emerging technology with a robust business case to improve CX to the long-term benefit of the business, getting the right information flows in place, eliciting strategic advantage and ensuring exceptional CX. The HFS OneOffice Experience typifies how customer, partner and employee experience are coming together to drive a unified mindset, goals and business outcomes.

Rolling out technology and hoping “box ticked, job done” will suffice, is unlikely to end well. Only customers, employees and key partners can judge the success of an enterprise’s endeavors, and smart firms will start measuring what matters: sentiment, preferences, engagement levels, propensity to consume, customer lifetime value, employee satisfaction and experiences of key partners and suppliers.

4) Digital Associates become a real part of our work-life

We’ve become very comfortable with using digital assistants as consumers, and 2020 is the year that we’ll start to see them more actively in our work lives. Companies that are pioneering cognitive assistants in the workplace, like IPsoft, have been quietly implementing them to assist with IT tickets, HR queries, and as a whisper tools to help customer service agents resolve problems. Next year we’ll see these become more commonplace as an enabler of the OneOffice within our organizations, helping us do our jobs more efficiently and intelligently. What’s more, the conversation around cognitive assistants will start to mature, with less of a focus on how “human” the assistant can be, and more of a discussion about how it can accomplish tasks and understand people to help them rather than mimic them.

5) Technology convergence continues as low-code / no-code platforms continue their surge

While each element of the HFS Triple-A Trifecta (Automation, AI, and Smart Analytics) can be deployed individually, there is increasing convergence between the three elements to solve real business problems. For instance, smart analytics are increasingly reliant on AI tools such as NLP to conduct search-driven analytics, neural networks to do data exploration, and learning algorithms to build predictive models. Process mining and discovery is increasingly emerging as the front-end means to best assess automation potential and the post-automation means to track progress. Low-code platforms will allow enterprises to deploy the Triple-As to quickly and easily create modern enterprise apps. While the speed implication is massive, so too is the potential impact on business enablement. Low code technologies will enable greater participation from business operations constituents. However for this to work, as we have seen played out on the RPA stage, there has to be tight partnership between IT and business. We expect an increasing intersection of other emerging technologies like IoT and blockchain to this mix over time.

6) DXC and Cognizant will be the most acquisitive IT service providers as the market tightens

We predict DXC to be the most active in the market as it sheds some business and adds new ones into its portfolio. With Mike Salvino at the helm do not be surprised to see him looking at sharpening his firm’s business process teeth with an eye at Genpact. Cognizant could also spring a surprise or two after years of rampant growth and now shifting to a more disciplined focus under Brian Humphreys. Perhaps a foray into a high-growth banking-centric provider like Mphasis could be in the cards?

7) Most of the Indian-heritage providers will be dull as dishwater in the M&A market

As the big founder-driven firms seek to maintain margins in this flattening market, do not expect to see much at all of note from any of Infosys, TCS, Wipro, HCL or Tech Mahindra. The odd “tuck-in” service play may occur, but nothing that will raise eyebrows or drive the Times of India wild.

8) None of the big three RPA’s will get acquired

It just won’t happen – everyone’s looked and noone’s biting… the Salesforce interest in Automation Anywhere will be a big test as to whether one of the software big-runs make a major play. We thought Microsoft would make a play with UiPath, but clearly got sticker shock and dusted off some old tech to tick that itchy RPA box for a while.

9) Google and Amazon could make big plays into enterprise IT services

Yes, we could well see a Wholefoods style Amazon play into enterprise IT at looks at ingesting Big Blue – just think it completely solidifies cloud supremacy in one go (if it ever needed it) and has a household American name to go after the enterprise in a very big and ugly way.

Meanwhile, Google is trying to make a very enterprisey play adding the likes of Thomas Kurian and Robert Enslin to its expensively assembled enterprise catch-up team. If they take the plunge, expect them to move for the more affordable DXC or Cognizant to fill out their services portfolio.

10) Alibaba Cloud will leapfrog Google and Microsoft in PaaS and IaaS Revenues

We can expect to see the hyperscale applecart upset by Alibaba cloud. Alibaba Cloud will leapfrog Google and Microsoft in PaaS and IaaS Revenues. With Alibaba Cloud, Google and Microsoft all boasting limitless investment potential, it’s hard to call who’s winning the battle. But if we were to put on our more speculative 2020 prediction hats on, we’d turn our attention to Alibaba Cloud, which has been quietly gaining significant ground over the past two years, doubling revenues between 2017 and 2018. While Google has developed a compelling long-term strategy for substantial growth, in the short-term we can expect to see Alibaba come up through the ranks as it consolidates it’s control in APAC and significant 2019 investments start to pay off in 2020.

11) Quantum leaves the lab and moves into the modern enterprise

We believe the cloud giants will spend more time and money on the emerging technology, having already seen quantum offerings delivered via the cloud from IBM and Amazon. Given the current levels of investment from Google and Microsoft we expect them to have quantum capacity on their cloud platforms by the end of 2020.

HFS expects to see Quantum make waves more broadly as it leaves the lab and moves into the modern enterprise in 2020. 2019 was an amazing year of progress for Quantum computing. Googles claims of quantum supremacy, some success with commercial quantum experiments, VW’s battery development tests and the growing investments from enterprise organizations, particularly those with existing high-performance computing. Although we haven’t changed our long-term forecast for full quantum computing, we expect genuine business use cases to emerge over the next 12 months. As current experiments start to bear fruit.

12) 2020 will see more record GDPR breaches, IoT cyber-security investments and cyber-insurance products

All of these clouds and qubits will need protecting from those grinch-like hackers and regulatory killjoys desperate to harsh the Christmas buzz of CISO’s everywhere. We can expect a rise in nation state hacking – with naughty national bodies targeting private enterprises with euphoric abandon in 2020. HFS also warns that this new threat will come in lockstep with strengthened regulatory bodies, and we’ll see a record breaking fine for GDPR… you might have thought the British Airways £183.4 million fine was bad – but that won’t be the last mega-fine to be handed out by regulators. 2020 will also see an increase in ransomware and hackers targeting enterprises who have been quick to stump up cash to unlock data in the past.

The increased sprawl of IoT networks will see the provider community race to embed cybersecurity into offerings and open up the warchest to buy what they need and look out for massive purchases in this space, alongside startups and SMEs partnering with service providers.

As data breaches, hacking, and all-round cyber-nastiness continues we can expect cyber-insurance products to increase in value and prevalence – we suppose we’ll need someone to pay BadDog1998 the bitcoins he wants to hand back our world of warcraft accounts.

13) Close to half of Enterprise AI engagements will shift from pilot to production as investments in explainable and interpretable AI boom

we’ll see more AI engagements move out of pilot to production environments with 80% of enterprise AI projects sitting in POC stages, and barely 20% in production. We expect this to flip in 2020 with close to 50% now making it into production. The areas we can expect to see the most value come in will include autonomous invoice processing, legal document validation and extraction, fraud detection, and similar business and process areas.

HFS also predicts a significant increase in R&D spend on explainable and interpretable AI as enterprises push vendors control and transparency. Most SP’s and AI technology vendors will invest more than 50% of their AI related R&D and CTO funds into the areas of explainable & interpretable AI, and also in building frameworks and solutions for AI governance, audit, lifecycle management, security, ethics and maintenance.

14) Supply chain will overtake financial services in terms of blockchain adoption and we will also see more public initiatives

Global supply chains are becoming increasingly complex and opaque—and less trustworthy. The multi-fold increase in product variants and the drive for speed to market, a shift toward mass personalization, growing logistical complexities, and increasing globalization necessitate a more connected and nimbler, yet flexible, supply chain. Supply chain problems are not new, but solutions were not forthcoming until distributed ledgers and blockchain began making inroads into the world of supply chains. The financial services sector was the first mover in enterprise blockchain adoption, but supply chain initiatives leveraging blockchain (especially provenance tracking) are catching up quickly. Global giants (like Walmart, Maersk, AB Inbev, and Nestle) as well as smaller and emerging players across logistics, CPG, agriculture, pharmaceuticals, and retailers are more interested than ever in applying blockchain technology to solve supply chain issues. The TradeLens ecosystem started by Maersk and IBM today is comprised of over 100 diverse organizations including carriers, ports, terminal operators, 3PLs, and freight forwarders. The power at the intersection of blockchain with other emerging technologies (IoT, AI, and advanced analytics) is making supply chain aficionados salivate!

2020 will bring more public blockchain initiatives, however, as firms like EY continue their investment into ZKPs, announcing in the final month of 2019 that they could offer private transactions for $0.24 per transaction, it’s possible that public blockchains could see favor, as they offer the scalability required alongside the previous missing ingredient; privacy.

15) 3D Printing and Drones will really come of age to drive manufacturing 4.0

HFS also looks forward to other exciting technologies – particularly 3D Printing and Drones – which will move off of the faux industrial racking at the sides of every vendor ‘ideation lab’ and out into the real world. While both 3D printers and drones are still at the periphery now, we predict that leading service providers, vendors, and manufacturers will continue to innovate and partner to set the groundwork for a future when technology bugs and market barriers have been removed. Many will find it too late to catch up, while the pioneers will either leverage existing solutions or partner with vendors to co-develop the technology.

16) Sustainability will come back into vogue as our environment decomposes further – and the UK gears up to host a critical COP26

HFS anticipates growing demand for sustainability services. And while most of the market is chewed up by the major consultancies, by 2020 we’ll see a move as providers take leaning from internal initiatives to professionalized customer facing offerings. We advise everyone should watch the space for one big legacy provider making the jump – whether by partnership, acquisition, or leveraging their existing internal sustainability expertise.

Moving to 2020’s COP26 (the UN’s latest climate summit – to be held in Glasgow): a lot of key decisions from this year’s COP25 in Madrid were delayed to 2020, and a a result there’s going to be a lot of hype surrounding COP26. Keen sustainability providers like KPMG, Accenture, and friends – alongside consulting giants like McKinsey and sustainability boutiques – will ramp up their CSR and sustainability services/consulting activity… while many legacy providers who’ve not yet moved whole-heartedly into this space will have to struggle to cut through by only marketing CSR projects and a few LED lightbulbs.

The EU could also play a massive part if they can get some climate clause into the UK’s Brexit withdrawal agreement – and everyone’s eye’s will be peeled to see if Boris Johnson will decide to unveil some big commitment given the UK is hosting COP26… whether or not that is a tangible commitment that spurs action is another matter… be he might yet surprise us by going beyond an arbitrary net-zero deadline. Any businesses residing in or dealing with the EU should watch the space surrounding November’s COP26 with a great deal of interest and scrutiny!

17) The S4 HANA migration deadline will get postponed

Now this one’s a real risky bet – and given we have five years to see if we’re right it’s more for fun than anything else. The S/4 HANA migration date is set for 2025 in a bid to drive clients to bite the bullet and stump up for the new technology. But we’ve been doing some digging over the last year and it’s fair to say, sentiment from business leaders is lukewarm at best – and even some of the most bullish proponents of migration in the services market have cooled off. In part, we think the appetite isn’t there to make plans for something so far off – when there’s so much quantum and blockchain to pay for. But there are also real logistical issues around getting trained professionals in to help do the work. And an already dicey talent pool is keeping prices high, a rush as the deadline gets closer will only push costs higher. Making those all-important business cases much harder to get passed the board. Something business leaders are already telling us is like banging their heads against a wall as they justify an upgrade on a system they’ve only just finished implementing. Our bet is as the deadline approaches – SAP will acquiesce and offer clients a rope rather than risk lifelong clients heading off to Oracle or Microsoft

18) Transactional F&A will start to become “invisible” to elevate finance as a strategic business partner

Enterprises have always wanted far more for far less from their F&A function. But the old days of finding cheaper labor and some better packaged software have pretty much been exhausted. The new thinking is to change how finance is delivered, where the routine F&A work becomes invisible to focus completely on the strategic value finance brings to the organization. HFS defines “Invisible F&A” as the state of an F&A function where accounting transactions run like water and finance professionals focus on driving strategic objectives. Leading F&A service providers like Accenture and Genpact are starting to take their clients on a journey towards continuous accounting requiring no waiting to close books, effortless payables and receivables with near-zero cycles, and real-time analytics capabilities enabling proactive decisions. In 2020 we will start hearing more success stories about pioneering enterprises achieving a near “invisible” transactional F&A.

19) The boundaries between finance, procurement, and supply chain start to blur

Back-office operational transformation journey started nearly two decades ago with the rise of shared services and outsourcing around payables, receivables, and general ledger management. These mostly siloed tasks evolved into end-to-end processes as payables became procure-to-pay (P2P), receivables evolved to order-to-cash (O2C), and general ledger expanded into record-to-report (R2R). Finance was already expanding into procurement and sales organizations; however, it was still mostly back-office focused. The future calls for a boundary-free organization where silos around the front, middle, and back offices collapse to create a “OneOffice” — the office that caters to the customer. To create this Finance OneOffice, P2P needs to expand into source-to-pay (S2P), O2C needs to expand upstream into the CRM space (lead-to-order) and downstream into after-sales services, and R2R should extend into enterprise planning management (EPM).

20) 2020 will mark the start of a new decade where we focus on the “How”

A new year and a new decade is upon us. The last 10 years were dominated by digital everything! As we enter the next decade, the “why” is relatively well understood. Data explosion, digital disruption, and customer experience emerged as the three most important drivers impacting business operations. Clarity around the “what” is emerging. The promise of emerging technologies across the Triple-A Trifecta (Automation, Analytics, and Artificial Intelligence), cloud, IoT, and blockchain is unquestionable. But the “How” continues to be a black hole. The talent question needs to be resolved. Siloed and piecemeal technology solutions need to get more integrated. Stakeholder alignment across business and IT is crucial. Success needs to be defined by digital change management versus digital adoption. And transformation needs to increasingly be driven by better experiences – customer, employee, partner – not faster and cheaper. 2020s will be the decade of the “How.”

21) …. and finally the 2020s will see the start of a debate to understand the “New why”

The focus on business outcomes helps us do the same things better, faster, or cheaper (often in a ‘pick two’ mode) but is that sufficient to succeed in today’s world? Some of the most highly valued companies are not even profitable. Investors are replacing price to earnings ratios with price to sales ratio. This often creates “hyper-hype” because the reality is, we no longer know “why” we are doing digital! We are just doing it because others are and we are in the rat race for better, faster, cheaper – none of which actually means “transformation!” The new “why” will be based on a value algorithm that combines traditional definition of business impact (better, faster, cheaper) with:

The Social impact (values, sustainability, and diversity/inclusion)

The OneOffice impact where internal silos cease to exist and there is only One Office that matters which caters to the customer

The Hyperconnected Ecosystem Impact (can a car manufacturer even aspire to deliver ultimate customer experience without its ecosystem of insurers, government and other supply chain entities?)

Or will the “WeWork” debacle push us back to unfashionable but tried and tested methods of creating shareholder value?

We all know a few “do-nothing” employees, don’t we? Those lovely people who somehow slither around within their organizations and somehow retain employment… despite never really doing anything. But, in this new decade, surely this is the time they get found out, with all this AI available to out the scoundrels? Or maybe they can continue to hone their do-nothing craft in the cyber age to keep that do-thing ship sailing nowhere in particular…

Here are a few master ‘do-nothing’ tactics:

1. Insist on attending every meeting. If only to deflect actions on to people who didn’t attend.

2. Insist you ‘have some thoughts’ about other people’s projects. Make sure the thoughts never materialize, but you get credit for participating in the project.

3. ALWAYS insist your inbox is ‘hectic’ and you were ‘just about to get to it’ when called out for ignoring an urgent issue for two weeks.

4. If you’re asked a question you don’t know the answer to, insist you do know the answer but they’ll need to go through the proper channels to get to it. If you’re the proper channel, send them to marketing for ‘approval’ first.

5. Use the phrase ‘at capacity’, ‘snowed under’, ‘bandwidth-constrained’ and ‘keeping my head above water’ as often as possible. It’ll add credibility for when you want to shirk off work later. Pay it forward.

6. Occasionally drop in the ‘drinking from a fire hose’ line, but don’t overdo that one. Save it for an avoidance emergency.

7. Say thought-leadership. A lot.

8. Use the phrase ‘let’s not boil the ocean’ when scary workload is threatening to land on your plate.

9. Pay very close attention to what your job description is. Ambiguity is good – if it doesn’t explicitly say something, don’t do it.

10. If in doubt, cite ‘hostility’, ‘toxicity’ or whatever else Oleg on LinkedIn says. After all, the fact that you’d rather pretend to be on the phone than actually speak to someone isn’t your fault, it’s the lack of inspiring leadership.

11. Don’t be afraid to book extra meetings if it’s a quiet day and you might have to do some work. Pre-meeting meetings are a must. And don’t be afraid to schedule a wrap-up meeting after the initial meeting.

12. Oh, and don’t forget to pop a few fake meetings in there for good measure (mark some as ‘private’ to make you seem important).

13. Above all, find genuinely busy people to hang around. It’ll make it seem like you’re also a go-getter, when actually you’ve been trying to get passed stage 10 of angry birds since February.

14. Have your Out of Office on as much as possible citing ‘business travel’ and slap a load of names down to contact.

15. Only ever respond to any request to do ‘anything’ from your boss, or your boss’ boss. Otherwise, just ignore it. This is why you need your OOO on…

16. When you actually get cornered into DOING something, make sure the whole world knows you just split the atom.

So there you have it, can you help us get to twenty for 2020?

According to RAND’s website, “For seven decades, RAND has used rigorous, fact-based research and analysis to help individuals, families, and communities throughout the world be safer and more secure, healthier and more prosperous. Our research spans the issues that matter most, such as energy, education, health care, justice, the environment, international affairs, and national security.”

So let’s take a look at how our public money was being used to help their predictions back in 1964:

The Bottom-line: Today’s analysts aren’t that bad!

But why didn’t we think of breeding apes and other animals to perform menial work before wasting all this time and money on RPA?

Have you noticed how business process management (BPM) services has quietly risen in value in recent years as the need to redesign processes that can take full advantage of emerging technologies intensifies? As technology increasingly augments human-driven processes through digitization and automation, the need for business process management services at scale is increasing at a healthy clip. Just look at the double-digit(ish) growth enjoyed by Genpact, InfyBPM, EXL, WNS etc and you will quickly see that human-driven services are driving the next wave of the industry.

One man in the center of this trend is Ritesh Idnani, one of the founding brains behind InfosysBPM back in the day, who returned to the BPM industry to inspire Tech Mahindra’s BPM business in 2016. Since then, he’s created the highest growth division in the firm and worked tirelessly to bridge traditional BPM with automation technology by integrating front-to-back processes with contact center services and CX-related capabilities. To that end, he oversaw the recent acquisition of digital agency BORN, where he will seek to drive a full OneOffice offering experience for TechM clients. So let’s hear a bit more about where Ritesh is taking the firm…

Phil Fersht, CEO HFS Research: Hi Ritesh – welcome back! It’s been quite a few years since we heard from you since your days at InfyBPO… what are you up to these days? What’s getting you up in the morning?

Ritesh Idnani, President, Tech Mahindra: Good to be back, Phil! The last few years has been quite a journey for me personally both as an operator in private equity-backed portfolio companies and as an advisor to private companies and investments that private equity funds are looking at in technology and technology-enabled services. I’ve now been with Tech Mahindra (for the last 3 years), a $5 billion revenue company which is the only non-US company that is part of the Forbes Digital 100 list. I wear a few different hats at the firm ranging from driving the Business Process Services organization globally, a 60,000+ digital human workforce, our software products and platforms business as well as leading a number of strategic corporate initiatives.

I know we all like talking about technology, about the complicated strategy and technologies that will disrupt the BPS business, but my priorities are slightly different. Technology is moving crazy fast in so many different directions simultaneously. We’d be lucky if your prediction or mine about the future has a better probability of coming true than a toss of a coin. In that kind of environment, the biggest differentiator for any organization is speed, simplicity, quality and ease for everyone. Whatever technology we discover, and I promise we will be at the leading edge of discovering the applications of new technologies, we have to be agile to solve customer problems as quickly as possible. If we do that quicker than our competition, our customers do it better than their competition, they succeed, and so do we. That doesn’t mean we have to invent everything. We have to be fastest to market and fastest to creating value for our customers. If we do that consistently, we remain the partner of “relevance” to our clients. The interesting thing of the current technology shifts is that our clients don’t know what they don’t know and the service providers also don’t know what they don’t know because the pace of change is rapid. The opportunity to help our clients navigate through the shifts is what gets me excited everyday.

So my focus has been to build an organization that is entrepreneurial and cutting edge and solves problems for customers. It’s something that I think will be a big differentiator between success and failure in the 2020’s. Forget long term plans. Can you execute fast enough?

So we hear a little rumor that you were instrumental in acquiring the Digital agency BORN. This is quite the coup for Tech Mahindra… So how will this fit with your current businesses?

I did have a role to play along with our corporate development team to help acquire the BORN Group. I’ve known Dilip Keshu, CEO @ Born Group for a few years now and have been mighty impressed with what he was creating as an industry leading and differentiated organization. So when we got the opportunity to look at opportunities to collaborate more closely, we certainly jumped at the prospect of the combination.

I’ve been spending a lot of time with the BORN leadership team, and we’re incredibly excited to welcome the BORN Group to the TechM family. The Born Group is an iconic global agency with end to end capabilities across creative, content and commerce. In fact, just recently, they won the e-commerce agency of the year in Asia for their industry leading commerce capabilities.

We’ve been building out our Customer Experience capabilities over the past few years. Our strategy is to build an end-to-end CX offer that means we can help our clients design and deliver really innovative customer experiences, underpinned by cutting-edge technologies that both differentiate and strip out cost.

What we have realized is that in the traditional contact center business, bulk of the existing business is dealing with failure demand. Something goes wrong with customer’s business, more customers contact you, more FTEs to deal with that volume, and more revenues. I hate that business model. Because it’s at cross purposes with our customer’s objectives. Running downstream operations limits us in addressing this issue. The only way to help our customers is to get engaged upstream in CX design, and get closer to marketing. When processes are designed for right first time, our customers need less of our services and we are happy with that. BIO, Mad*Pow and now BORN help us with these capabilities across regions and verticals.

The other trend is how contact center and online are virtually coming together. Sales and service journeys often start in one channel and end up in the other. We are industry leaders in the front office today. We are making giant leaps with these acquisitions in the online world. What we now have is a portfolio that addresses the needs of CMOs, CDOs, CIOs and heads of customer experience to help achieve their objectives. In addition to that, it now allows us to offer a whole suite of offerings across the brand experience, behavioral experience and the book of records as an end to end provider.

And how do you see the services industry converging across business process and digital delivery? What sort of conversation will we be having in another couple of years?

Interesting question Phil! We’re definitely seeing convergence. Take the case of a 13 year old kid who is into online gaming. He knows what it takes to succeed there. He needs the lightest gaming controller or mouse. It’s so interesting to observe how he goes about his business. He does an online research. He goes to the store for a hands on experience. Then he checks online, store and contact center offers and pricing and tells me this is where to buy it from. It’s not a choice. Consumer behavior will drive it anyways.

Consumers (and our clients!) want seamless omnichannel experience across their journeys, and that means joining up the business processes and digital assets that deliver CX

Equally, businesses are waking up to that fact that Brand and Marketing investments are secondary relative to CX investments. If your customers aren’t happy, marketing investments won’t bring returns. So we’re also seeing convergence across Marketing and Customer Operations, with CMOs taking on an extended remit on Customer Experience.

I’m personally quite focused on seeing how we can emerge as the catalyst for One Office transformation. I know that’s a topic close to your heart but I do see the digital delivery changing the rules of the game between traditional silos across the front, mid and back office. We have just launched a one office experience framework (OFX) that brings all the IP we have as a firm as well as third party ecosystem that we partner with to bring seamless, frictionless experiences and reimagine the way we do traditional processes. We are taking our role of being the orchestrator or the “stitcher in chief” as I like to call it very seriously to ensure we can bridge the gap between business processes and digital delivery.

You’ve also been very vocal, Ritesh, about the way your BPM team has embraced automation to drive the customer experience – can you share a little about how what is faring? What are the successes and challenges of the services model as you do more of these deals?

To be honest, Phil, we’re only just keeping up with demand on Automation. We have now reinforced our 60,000 strong digital human workforce in the BPS business with over 6,000 Bots, with a transformational impact. Automation doesn’t just mean cutting time and cost; it leads to consistency, improved resolution, better employee experience… and ultimately better customer experience.

In almost every case, our automation journey with clients has quickly accelerated; we now have automation factories on every continent. But that in itself leads to challenges. We had to learn how to maintain and service our army of Bots to ensure they keep functioning as the world around them continually changes. This is a challenge we’ve overcome, but one that we’re keeping an eye on as the Bot workforce increases. We are also actively leveraging AI/ ML where appropriate in our existing operations to eliminate work and improve cycle time.

Perhaps, the biggest thing to address here is the associated change management within the workforce. Traditionally, the BPO industry has seen people use traditional proxies of power – the number of folks you manage or the revenue you control. Automation, AI and analytics are challenging the traditional bastions of power. We had to change the way we measured people by asking them about the transformation they drove and the impact it had. Initially, we had anticipated a challenge from our workforce: we thought our people might see Bots as a threat to their jobs. But we quickly found that our people love them when they see that . Bots eliminate routine and repetitive tasks, and make it easier to find the right information at the right time. This has enabled our staff to spend more time engaging with customers, and the result is more satisfied employees, and better staff retention.

On the other hand, it also means change management at the customer end. Most customers want the right things, but ultimately it comes down to someone who used to do a repetitive simple task, whose job will be done by bots tomorrow. I am encouraging my teams to help customers deal with the change too. A classic example is customers asking for an SDLC for a simple RPA project. I see it as an employment guarantee scheme. We have to get better at influencing that.

At the same time, I would hasten to add that a big focus area for the industry as a whole is going to be the work to be done on crafting the “messy middle” – the new roles that get created on account of the interplay between machines and humans.

And finally, what’s your advice for emerging talent in the services industry… what would you do differently today if you were 23 again?

I would advise young people joining the sector to carefully navigate their career path to ensure they have deep-dive exposure to Technology, Analytics and AI. The 4th industrial revolution is well underway, and to become a leader in our industry you need to be able to stitch together the right capabilities to deliver client outcomes – and practical hands-on experience is invaluable. At the same time, professions are going to evolve over the course of a career. The average youngster entering the industry is probably going to see atleast 2-3 technology-led disruptions so the ability to unlearn and re-learn skills has never been more important than today. Critical thinking and dealing with ambiguity is going to be important so the sooner you seek out experiences that allow you to get out of your comfort zone, the better.

And if I were 23 again? Seriously, I entered the workforce when I was 23 joining a global bank and in hindsight, I would probably have expanded my horizons, travelled across the globe, spent more time on the beach, picked a few new hobbies/ interests … but that’s another story!

Well thanks for reconvening with us… and a terrific lunch too, Ritesh!

Net-net, technology isn’t necessarily the heart of making the connections from front to back – it’s making good choices about what you automate and having the business process in place to back it up.

Net-net, technology isn’t necessarily the heart of making the connections from front to back – it’s making good choices about what you automate and having the business process in place to back it up.