Why we think SAP acquiring Signavio is a non-event and actually frees Celonis from its SAP shackles to inspire its loyal following

The initial buzz from SAP leaders with its Signavio acquisition all points to helping its clients migrate from legacy systems onto cloud-based S4/HANA applications. While that is a worthy goal, SAP needs to embrace how to support both non-IT and IT clients with rapid process redesign, if it is to stand any chance of reclaiming former glories that are long-distant memories in today’s high-octane environment. The German software giant has an IT-centric view of the world, where instead we need technology and business to come together to become fluent in understanding the data they need to be effective in their markets. To create this data, processes need to be designed to deliver data at speed, and these need to be automated in the cloud to keep their enterprises functioning. Once processes are flowing beautifully in the cloud, you can deploy all sorts of ML and AI tools to gather increasing amounts of intelligence to anticipate your own needs – and your customers – ahead of time.

Until a decade ago, SAP was, perhaps, the most significant brand and voice in enterprise technology. The German software supremo was the enterprise backbone, the system of record, the “way of doing things” for the majority of the FORTUNE 1000. Back then, Microsoft was already entering rigormortis as a decrepit office suite, SFDC wasn’t much more than a fancy way of managing your contacts, while Workday was confusing everyone with “thin memory”, and Oracle was just a weird collection of tired con-fused software firms run by a guy who resembled a tech billionaire version of Donald Trump.

Since then, the SaaSy likes of Salesforce, Workday, and Coupa have long-driven a narrative that you had to run your processes in the cloud, while SAP labored to catch-up as a “Cloud player”. Then came the digital juggernauts of Microsoft, Amazon, and Google to ratchet the world of enterprise technology into a very different place, where data is king and it doesn’t matter how unstructured it is.

SAP has long-lost its enterprise appeal as the process connoisseur’s tech suite of choice

SAP is a symbol of a long-forgotten time when people’s careers were tied to it, when enterprises thought being locked-into an on-premise software suite was considered a strategically smart thing to do. Hell, any IT bigwig worth their salt needed SAP plastered all over their resume. But those days faded away after 2010 as the cloud took over the core processes in smart enterprises.

SAP made its long-rumored acquisition of workflow and process intelligence vendor Signavio official last week. The move has implications not only for the two merging tech companies, but also the market leader in process intelligence, Celonis, that until now, enjoyed a close and successful partnership with SAP. In addition, Celonis has cultivated many strong partnerships with the likes of Accenture, Cognizant, Genpact and IBM. Will they gravitate towards as SAP-owned Signavio? And will SAP’s army of customers really take this seriously enough to fight their CFOs for yet more cash to pump-prime the Waldorf machine? The depressing answer for both SAP and Singavio is simply: no one really cares.

Why SAP needs all the help it can get to earn credibility as a process orchestration and intelligence player

Every enterprise leader has taken a hard look at their business processes over the last year, seeking ways to streamline and automate tasks and get data on what is working and what broke in the move to remote working. What started as an exercise in somehow keeping the lights on in the pandemic economy, has started to turn into wider initiatives that will have a long-lasting impact. Many enterprises in our research have expressed that ‘there is no going back’, and post-pandemic, they will need a far smarter operating model, technology stack, and data-driven business processes. At the heart of this stack, for most companies, is a hodgepodge of various versions of aging business systems, fragmented over regions and markets, that are responsible for the majority of transactions that keep the business running.

Business leaders seeking their own glory on “digital transformation” and process efficiencies have implemented a plethora of bolt-on tools around core applications over the years, including business process modeling, workflow management, document and content management engines, and of course, robotic process automation. Process intelligence tools have been the latest addition to this mix. In particular, process mining technologies that use transactional system-log data (such as from SAP) to power their analytics and machine learning models.

Why Celonis was so good for SAP customers – and will still be for some time to come

The two principal uses of process mining tools that significantly help enterprises with their SAP estates include:

1) Helping operations leaders make the most of their current ERP and other source systems, find process bottlenecks and inefficiencies, and redesign processes such as order-to-cash and procurement

2) Helping IT teams with systems migration, such as a move to S4/HANA, where the mining technology can be used to map and monitor as-is and to-be processes, and user adoption over time.

Just with those two points, we can see why SAP’s partnerships in this space have gotten deeper in the last few years and got to a point where SAP felt the need to directly invest in a solution of its own. Hence its acquisition of Signavio.

SAP needed to partner with the likes of process intelligence leader Celonis and UiPath (which acquired ProcessGold) to keep its technology ticking, and provide its customers more process visibility and automation. Now it has the ability to define how a fully integrated BPM, workflow, process mining, and automation capability can augment its core technology, beyond what third-party platforms and a host of SAP-specific products have been able to achieve.

Weaning any client with years of experience off of their beloved Celonis to switch to an inferior product owned by SAP is not going to happen… so good luck with that folks!

When it comes to process augmentation, SAP is lightyears behind the market. In 2018, It made a low-budget attempt to enter the Robotic Process Automation (RPA) market with Contextor, a small little-known France-based RPA product to augment SAP Leonardo’s intelligent technologies portfolio. Nothing has been heard of them since, with no examples of SAP playing in the process automation space. It’s been a bust. So if SAP can’t make head nor tail of the most base form of process automation (RPA), why does it think it can take the market by storm acquiring a product which is ranked 13th in process intelligence software:

Simply-put, all the hard years the Celonis founders spent driving around Germany selling the software to SAP customers in a VW Camper (yes, I actually know this!), ensured that Celonis has firmly established itself as the process mining solution of choice, necessitating several years of investment, training and change management from its loyal clients. So why on earth would these process-obsessed customers flock to use the industry’s thirteenth best solution?

Why Signavio? Its collaboration hub and process simulation capabilities couldn’t be more timely for operating in the pandemic economy

As our recent evaluation, the HFS Process Intelligence Products Top 10, showed, Signavio has multiple bright spots and differentiation making it a formidable vendor in the rapidly growing process intelligence market. Its collaborative hub is a great place for business users to share results of their process analysis, comment and present, and collectively iterate on improving business processes – invaluable at a time when most organizations are still working remotely, and need more avenues for collaboration. Furthermore, Signavio’s process mining technology, in particular its simulation engine, is considered top of the line by its customers and partners. As we’re still operating in volatile markets, being able to model out changes in business processes and simulate their execution to find potential blockages can prove valuable by de-risking or accelerating needed changes. Lastly, Signavio’s bolster’s SAP with its BPM and workflow technologies, which customers value, especially its ability to port and overlay structured process models into the process mining module for comparison.

Despite the positives, Signavio customers we have spoken to indicate that it needs to invest to keep up with innovations in process intelligence. Many disruptive startups are continually keeping up the pressure – introducing new ML and data handling techniques, and standards in data visualization and UI/UX. Additionally, process intelligence isn’t the full focus for Signavio, which until a few years ago was only a BPM/workflow vendor. SAP may have inherited some challenges in investing in the process intelligence piece of the suite.

Where does the new alliance leave old beau Celonis? In our view, stronger, and on to bigger and better things

It would seem (on the surface) that Celonis has been thrown in a lurch by SAP’s acquisition of one of its competitors. However, there is a longer story of product and company evolution unfolding here, and SAP’s move only further cements the shift:

Life outside of SAP (Bigger): While SAP was the most common source system for its customers’ transactional data, it was never the sole one. Celonis has been steadily building on its partnerships, as well as technology extensibility into Oracle, Salesforce, and ServiceNow. We expect it to show these partners more love in coming days, which will ultimately only help it serve its customers better. This will allow Celonis to break free from I being perceived as an SAP-only process mining tool and diversifying its range here is a win-win for all stakeholders.

Moving onto EMS (Better): Celonis has already started expanding out from process intelligence into a Triple-A Trifecta solution approach by blending analytics, automation, and AI with the launch of its EMS last fall. As we observed, with EMS Celonis has created a system-of-engagement layer that sits on top of business processes and systems, drawing process insights, and creating execution strategies – either alerting and recommending actions to business users, or setting configurable rules to trigger automation for certain tasks. With this approach, Celonis is on a path toward not only helping you identify and rectify process bottlenecks, but also helping you execute the process itself, with smart insights and recommendations, and automation capabilities.

Building an international company(Stronger): Celonis has been expanding out of Germany as it gets global in all respects – its operations, management, and customer base. Early on, it struggled to fully present an integrated international front to the market. De-prioritizing SAP will give the non-German factions a chance to catch up and shine as well.

Celonis and SAP have worked together on more than 250 implementations in over 30 countries, with clients including 3M, Airbus, Bosch, Coca Cola, ExxonMobil, Novartis, SABIC, and Zalando. Celonis is SAP’s #1 Cloud Solution Extension Partner, and the vendor has developed tons of data connectors, applications, and content to support SAP’s ERP landscape. In fact, SAP is using Celonis to optimize its own internal business processes. The two firms enjoy a shared German tech culture, and as a co-innovation partner, SAP has thus far undeniably influenced Celonis’ product direction thus far.

In conversation with HFS, Celonis leaders mentioned that this move by SAP serves to validate its investments into EMS. The start-up now considers SAP + Signavio to be a competitor to Celonis in its self-anointed EMS category.

The Bottom Line: SAP needs to prove this isn’t yet another tick-in-the box acquisition, and actively put its new process intelligence toolbox to work for enterprises, beyond S4/HANA systems migration

As we discussed earlier, there is massive potential for SAP to embed native process intelligence into its transactional processes to help clients uncover issues and improve business performance. Celonis refers to this as the EMS category. Whether or not that category name will stick, it signals a potential opportunity that is SAP’s to lose.

However, while this all sounds great in principle for SAP, we believe Celonis customers will stay put and many will benefit from innovations that are not created with SAP in mind. Celonis will reinforce its spot as number one in this market.

Having introduced RPA to the world in 2012 I have (sometimes grimly) clung to the belief that RPA will eventually find its path to be a vital cog in the enterprise technology potpourri. Blue Prism opted for the comfort of floating on the London stock exchange less than four years later in 2016, where its founders and key stakeholders opted for a modest payday, rather than make the really bold play of floating in the Big Apple and making themselves known as the pioneer of automation software. The other two major robotic software candidates, Automation Anywhere and UiPath then proceeded to demonstrate their beauty to the big iron software giants, which all opted to seek out cheap acquisitions to scratch their RPA itch, with SAP, Appian, Microsoft, and IBM all settling for small-scale tech additions, rather than making the multi-billion dollar investments AA (Automation Anywhere) and UiPath were demanding.

So with only $450m actually being invested in RPA acquisitions from the tech sector, the $1 billion+ UiPath has been burning through (and a not-dissimilar amount with AA) clearly indicates IPO is the only realistic path forward

It’s easy to blame Covid on many things, such as the negative impact it has had on my performance in cleaning the kitchen, but one thing has been clear: Covid amplified situations where enterprises were struggling or doing well. In UiPath’s case, pre-Covid they tried to force a market situation before their market was ready… all they needed was the patience to wait for their market to open up for them and keep the robotic love story emerging among its starry-eyed clients. However, during 2020 UiPath far outstripped all its competitors because it has an employee base to upsell, and it made its solutions the easiest for services firms and consultants to implement. The efforts made to push their platform into as many clients as possible pre-Covid has paid real dividends with sales cycles severely restricted to those clients who already use your software.

Step up UiPath, your time is now

UiPath’s potential IPO has been whispered about for a couple of years now, but pre-Covid, AA was widely expected to be the first to IPO. With UIPath’s stellar sales performance in 2020, the race to IPO has clearly swung towards UiPath as it has considerably outpaced both AA and Blue Prism in terms of license sales, and you just can’t IPO when your sales performance is flagging.

To this end, in mid-December Bloomberg reported and UiPath eventually confirmed that it filed a draft registration statement on a confidential basis with the SEC for a proposed public offering of its Class A common stock. While the filing may be confidential, UiPath is making sure the buzz about it is anything but. If the likes of Microsoft, Oracle, and Salesforce are failing to see the value of acquiring the firm with a very, very effective services partnership strategy and rampant installed base, then it”s time to open up to the public where there is well over $1 trillion of funds just primed for a tasty investment in a tech firm that has captured the excitement of the Global 2000.

Ultimately, IPO is the only path forward for UiPath. It has received more than a $1B in funding and its investors would like some return. And when valuation makes you a “deca-corn” it’s tough to find a buyer. Public markets to the rescue. While we’ve been VERY vocal about our view that RPA is in no way transformative, there is a ton of “now” value to be reaped from helping enterprises prop up legacy for another couple of years. Their investors have always been very clear that the “now” value of RPA is what makes it investment-worthy. And in a pandemic, clearly more so.

All the ingredients are there for UIPath to IPO and change its mindset

Meanwhile, UiPath continues to invest in its product functionality both organically and via M&A, driving capabilities beyond core rules-only RPA to help it better grapple with unstructured data and support process intelligence. However, HFS sees zero chance of UiPath ever realizing its vision of a robot for every human (which we affectionately refer to as a thinly veiled plan for a license for every client employee) or at least not in its current incarnation which is still predominantly unattended. Microsoft, which just completed the native integration of Winautomation from its acquisition of Softomotive is tracking much more in this direction (Clippy2 anyone?) and has a massive base of desktop users to convert. Nor is UiPath poised to become the “new ERP” as suggested in their recent 2021 predictions – largely because RPA alone, despite the upgrades, does not possess enough functionality to be the epicenter of process and workflow orchestration that sits atop existing enterprise apps.

As for the IPO path, UiPath has been adding customers hand-over-fist, generating massive growth figures. UiPath would be successful by every measure if they could crack the customer scale code. But that’s the challenge – they won’t. RPA has an expiration date that kicks in with legacy modernization. It doesn’t scale not because it can’t but because enterprises don’t need it to. Enterprises can keep using the same 50 bot license and get what they need year on year.

Bottom-line: @UiPath holds the attention of the RPA industry vying to become the first public multi-billion-dollar robotics platform to float on the #NASDAQ. Now its leadership must show maturity and embrace reality. Their time is now .

While it’s easy to criticize anyone in a market that is still flying by the seat of its pants, we have to give UiPath credit for outpacing all its competitors over 2020 and finding itself in pole position to IPO as early as next month. When you consider the only other recent tech IPO was the long-established Cloud firm Rackspace, the market will welcome the market leader in robotics software and make its investors very happy after a frustrating three years of confusing marketing, fantastical narratives, and an incredibly poor ability to win the hearts of many influential analysts. But you know HFS, we can dish it out, and we can also take a punch or two. But we always err on the side of reality, and the reality here is that UiPath will succeed in being the first robotics platform to IPO. It has become the automation platform for many of the leading service providers, and while scaling has been a real challenge, UiPath is winning that battle. The company actually refuses to talk to me or my brilliant colleague Elena Christopher these days because its leadership couldn’t stomach some hard truths we dished out to them pre-Covid (and refused to spend a few minutes digesting data on 372 enterprises). But that’s OK – if you want to control all the narrative and cannot find the humility to take a few punches when you need to take them, you only need to look at other leadership disasters to see where that attitude takes you. Huge egos and inability to listen will see anyone fail. Creating a narrative everyone can believe in, embracing your critics and designing a strategy we call all learn to love are the keys to success beyond IPO.

So this is a time to embrace the hard-won success of Daniel Dines and his team to see RPA finally establish itself in the “work from anywhere” enterprise tech stack. Now let’s hope they can control their egos a bit better to embrace the much more lucrative industry that awaits them.

The IT services market has arrived at its most critical infection point in 20 years, where the role of service providers that survive the Covid era will be those that have made the shift from support firm (Phase 1) to a business partner (Phase 2). We’ve talked about this services shift ever since Tom Reuner and I were young analysts. And we’re not very young anymore. Especially Dr. Reuner.

So why on earth is Atos bidding to make some wild takeover of DXC? Let’s understand the burning platform driving this

When the first major tranche of IT support deals evolved to a heavy dependence on India as a delivery location to exploit lower-cost labor at scale, made possible by the original Internet revolution. In the early days of the offshore era, the more ambitious traditional IT services firms, at the time, developed their own global delivery models with the goal of staying relevant, in the face of emerging competition from the “Indian Pure Plays” (as they were known in those days). This included the likes of Accenture, Capgemini, HP, and IBM – all of whom invested in India to attempt their own flavor of global service delivery with “added value” that the IPPs – at the time – could not (yet) deliver. The traditional IT service firms which failed to invest effectively in the global delivery model, once-great brands such as ACS, CSC and EDS, all got acquired by traditional western outfits. And the IPPs which failed to break into the Indian Top Tier eventually got rolled up into the second tier of traditional IT services shops, desperate to keep competitive, such as Patni, IGATE, and Syntel.

Covid has forced the services industry to make the rapid pivot from bread-and-butter to business-transformation services

Getting to the point of this little history lesson, we need to understand the motivations behind these acquisitive moves. Phase 1 was all about cost, scale, growth, and profitability as IT services firms could save the Global 2000 billions of dollars by exploiting cheaper talent at scale. If you weren’t in the game of pulling the cost lever – and adding above-average value somewhere to justify yourself to your clients – you either made a graceful exit to a willing suitor adding you to their own scale game – or chose to tread water and watch yourself get progressively smaller and desperate, until you got to a point where nones wanted to buy you anymore. I’ll share these firms’ identities over a drink if you can’t guess who there are already.

This new era of services (Phase 2) is seeing a clear bifurcation between the bread-and-butter services of the years pre-Covid – namely standard IT infra, app development and support, and BPO – and the present-day transformative services that run your borderless, work-from-anywhere business operations in the cloud, dependent on deep skills in data science, process design, automation, and most importantly, business logic and training people to become digitally-fluent. You can read our HFS 2025 Services Vision here.

The drawn-out Pandemic Era has forced the route into the cloud; it has forced processes to be re-designed and automated (or re-automated); it has forced enterprises to embrace rapid change, and it has forced the leading service providers to put their money where their mouths are or face a painful drain-circling experience as the bottom falls out of the traditional services model.

The new leaders in Phase 2 of IT services are rapidly emerging – and these do not include Atos and DXC.

IBM is spinning out its legacy infrastructure business while Hyperscalers like Google are starting to win comprehensive cloud deals as in the case of Deutsche Bank. Furthermore, accelerated by the pandemic service providers are reorganizing their business around the cloud. In addition, we are seeing a spate of mega-outsourcing deals in the billions as the word’s fourth-largest economy, Germany, finally warms up to outsourcing by doing “big-bang” deals to the likes of Infosys, TCS, and Wipro, keen to exploit this market and strengthen for the expected recovery later this year, where we forecast growth of 5%+ across services markets. Atos also got its piece of the action successfully extending its partnership with Siemens for another five years (see below), so this does beg the question why it needs DXC, as it clearly need to focus on making that shift from Phase 1 to Phase 2, and its very difficult to understand how a gargantuan merger is what it needs right now. Simply put, this is probably the most complex services merger ever contemplated by two firms which do not have a great track record of large, complex mergers:

Against this background, the announcements that Atos and DXC are publicly reporting a potential takeover of DXC by Atos – in the region of $10 billion – are very surprising, as both firms have been struggling to keep pace with the market leaders for years, and Covid has not provided any respite for either, although DXC has shown some signs of arresting its decline under the leadership of Mike Salvino now in his second year at the helm. Having providers officially confirming takeover discussions is highly unusual, which indicates a merger could well be inevitable if the numbers add up to the stakeholders that matter. Yet, the central strategic question is whether there is an opportunity to consolidate and scale lower margin legacy businesses rather than focusing on investing in innovation.

Rather than getting bigger, these services firms need to spin off their legacy businesses. This proposed merger is illogical.

Currently, HFS sees little value in merging these two firms together, as the only potential value is more in scale and geography, as opposed to deep areas of innovation where both firms are struggling in this tough market. The muted reactions from Wall St tell enough of a story already – this whole merger proposal smells like a consolidation exercise that could be even less effective than the carnage caused when HP and CSC merged to form DXC in 2016. What’s more, Atos has struggled to derive much value from its major offshore-centric investment Syntel, so the chances of an Atos-led juggernaut of mainly legacy services business-lines being effective are highly questionable.

While we laud the value of OneOffice at HFS, this could be the antithesis version, with a hundred-plus ‘offices’ all grimly clinging to survival. We believe the IBM model of spinning out legacy business lines from growth business lines is the smart way forward. That is not to say a merged DXC and Atos could not pursue a smart strategy, but the simple fact that neither has done this to date gives us little confidence that they will.

So let’s take a look under the covers…

Atos and DXC are caught between a rock and a hard place: Losing out on recent large deals while having limited levers for margin improvement

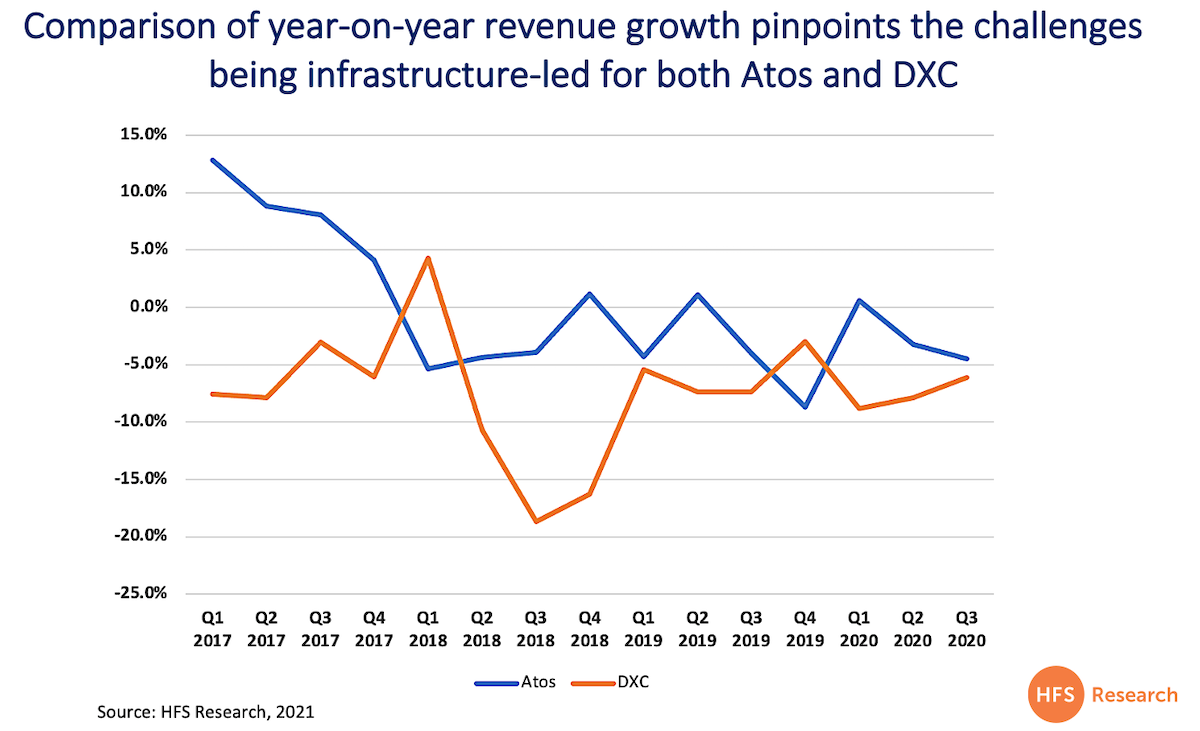

The recent major contract wins of TCS at Walgreens, Infosys’ double swoop at Vanguard and Daimler, and Wipro at Metro paints a bleak picture. It is too simplistic to point out that some of these were asset-heavy deals as an explanation for the lack of success. In particular, in the context of Daimler, there is a strong cloud element and the synergies across the automotive ecosystem are immense in areas like supply chain, cloud agility and creating of data value. While in the Walgreens extension contract, a strong emphasis was placed on digital innovation. The key question for both providers is where revenue growth should come from as the anemic growth as Exhibit 1 highlights:

If topline growth is not the priority then margins have to be improved by either extreme efficiency of operations and/or deep investments in innovation. As our Triple Trifecta Services Top 10 has demonstrated, neither organization made it to the overall Top 10. Atos has strong investments in innovation and a solid vision but struggles around execution. DXC has not even made the Top 10 in any of the various categories. As such deeper investments in innovation but more importantly, the execution of it should be top of mind to Atos.

The deal logic appears to hinge on three pillars:

Finally, Giving Atos scale in the US market

Cross-selling between accounts

Aggressive cost take-out

Atos has a solid track record in M&A. While Syntel might have been fluffed, it managed to extract value out of stagnated businesses like Siemens, Xerox, and Bull. But we see the deal at best as a defensive move that would be buying Atos management time for other strategic moves. While Mike Salvino has stabilized DXC, he has taken over an organization that was demoralized and exhausted after continuous excessive cost-cutting and management change. . His task ahead is perhaps best illustrated by a comparison of operating margins. In Q3 2020, DXC was at 6.2% while Infosys achieved top-in-class with 25.4% and bellwether Accenture came in at 14.3%. Thus, the reported price of $10billion would represent a significant premium on a market capitalization of ca. $7.4bn that is likely to tempt shareholders to accept the offer.

Atos needs to reinvigorate around innovation – not legacy

M&A is in Atos’ DNA. The company is built on perpetual acquisition activity. The extension of the Siemens outsourcing contract in September 2020 is testimony that it can extract value even from highly challenging acquisition targets. Yet, DXC both in terms of scale as well as the culture would be its biggest challenge to date. The acquisition would also come at a time where the company is going through an organizational restructuring dubbed SPRING. With that Atos is moving from a largely horizontal go-to-market to one that is focused on verticals. OneCloud will be the first practice for this new organizational setup. Atos is late with a move toward verticalization and DXC is more advanced. But the key strategic issue goes beyond culture and integration. With the deal, Atos would become a consolidator of legacy businesses. Yet as Accenture and the Indian heritage provider demonstrate, value stems from moving aggressively toward innovation.

DXC is still suffering from its own ill-timed M&A

With a certain irony, DXC is still suffering from its ill-timed acquisition of EDS in 2008 at a time when the outsourcing market was shifting toward more discrete deals with a strong digital flavor. The margin erosion in ITO and infrastructure projects is still haunting DXC. However, in sharp contrast for instance to IBM, there is no RedHat in sight which could act as a catalyst for change. Rather Mike Salvino has evaluated “Strategic Alternatives” for three business units: the U.S., state, and local health and human services business; its horizontal BPS business; and its workplace and mobility business. The public sector business has meanwhile being sold while the other two units will be retained. But this process makes clear that the whole business model is under constant review. Despite more targeted moves like for Luxoft, it appears unlikely that DXC could turn into a consolidator. Therefore, its strategic options are limited.

Bottom-line: The consolidation of legacy businesses will make bankers and executive management happy, but it won’t transform Atos

While Atos might finally get to get to scale in the US, the proposed deal lacks imagination as neither firm adds much of the new world to the traditional world. The offshore component of both firms is not compelling when compared to any of the leaders. For example, their capabilities across the emerging market areas of the OneOffice platform, such as ServiceNow, Salesforce, Pega, SAP S4 Hana and Workday are not leading edge, and business process services investments across both firms have long been neglected. Yes, Atos management might be buying time for a more incisive transformation, but the strategic headwinds are already immense. Clients are looking for trusted partners to accelerate the Phase 2 services journey toward the OneOffice. Doubling-down on legacy-at-scale is hardly a compelling pitch to move up the value chain.

OneOffice is all about putting the customer front and center by having end-to-end processes automated in the cloud enabling great AI to help you make winning decisions…

Joel Martin heads for the Cloud with HFS to lead the Cloud strategies practice

It’s funny when you meet these people across all corners of the globe during your career and you get that feeling that you’ll cross paths again in the future.

I first met Joel in 2002 when I was a Bio-IT analyst (yeah, I actually did that) in Australia working for IDC and Joel was running the PC tracker for the ANZ region.

Fast forward 19 years and Joel, and after his 10-year IDC stint, a couple of cyber-security and research startups; and a product marketing stint at Microsoft, got in touch about something that had nothing to do with the role for leading our new Cloud Practice was being advertised… I even asked him if he knew anyone when I thought “Hang on Joel, what are you doing these says…”.

To cut a long story short, Joel is now our first permanent Canadian employee, based in tropical Ottowa, with 2 daughters, (tries to) play guitar, and has mastered Bar B Qing at -20C. He has lived and worked all over the world and somehow still ended up in Ottowa. But that’s OK because we now officially have HFS Canada! He is also leading HFS’ new Cloud Practice to help the big pivot into the virtual work-anywhere world.

Phil Fersht, HFS: Before we get to all the work stuff, Joel, can you share a little bit about yourself….your background, what gets you up in the morning?

Joel Martin, Vice President Cloud Strategies, HFS: Great question Phil, thanks for asking.

About me, well, I like to think that I am a classic overachiever. I have built a career from a humble beginning to one that has allowed me to live, work, and experience cultures and peers in Europe, Asia, Australia, and North America. I love immersing myself in a new culture, have been fortunate to lead operations, sales, and research teams across the world, and thoroughly enjoy the customers I have engaged in finding new revenue opportunities.

I grew up in a small town in the United States, proud son of a Red Cross executive. As such, I got involved in community service from an early age, which continues to be important to me. Travel is something that I also grew up with, as early in my life, we lived in Germany and then across the U.S.

While at university, I built a partnership between the University in Leipzig and Houston, leading to my joining an international student-led program based out of New York City. This allowed me to travel extensively in Eastern Europe in the early and mid-90s, and honestly, I haven’t looked back. I started my technology career in Prague, Czech Republic, with IDC in 1997 and moved to Australia in 1999 and Toronto in 2004. Building a career in research, consulting, and practice leadership. Then I moved to Microsoft, where I was product marketing lead for the ERP business for Canada. In fact, I was part of the initial plans to move that product to the Cloud. After that, I was recruited by TechInsights, an Ottawa based Intellectual Property firm, to lead global marketing and product management. During this stint, I was part of the executive team that sold the business to a Private Equity firm and was retained to build exit strategies for different business lines.

During this time, both the company and the business I led went through significant digital transformation, taking our products and systems to the Cloud. This was a major undertaking as we fundamentally changed our financial, operations, HR, and customer-facing tools and experiences. That was 2015-2016, hard to believe nearly 5 years have passed.

Over the most recent 3 years, I ran workshops, managed client engagements, and wrote blueprints on building better supply chain relationships. I also supported a new program that focused on the impact of emotional connections between users that the software tools they use. Our hypothesis was that it is essential to look beyond the capabilities and features and understand what emotions drive satisfaction—a crucial component for marketing, sales, and buyer synergies.

Now I am excited to join HfS! As you and I worked together in the early 2000s in Sydney, while our paths diverged, we’ve found ourselves working together again.

As for what gets me up in the morning, I am an early riser, so after that first coffee cup, I like to explore problems with a fresh perspective. You know, before the in-box and to-do list from your boss dulls your creativity.

You’ve had a very global analyst career spanning several countries and continents… can you share some of your experiences over the years… what would you do all over again, and what would you definitely avoid?

When I look back at the crazy times of hitchhiking between meetings in Eastern Europe in the 90s to negotiating with a crooked cabbie in the middle of the night on a highway in China about the fare, there are undoubtedly many memories. And many things I would AND WOULD NOT do again!

The most important thing I always found while working abroad was being willing to listen. Not just to the customer or executive in the meeting, but to the colleagues, cabbies, and folks you meet while spending time in their country. Understanding another’s views based on their experiences, society, and culture has allowed me to apply my experiences in ways that have built more successful outcomes. In my experience, we often rush into conversations with our opinions and should take more time to listen.

So I do my best to avoid talking until asked. Instead, encourage the sharing of experiences, challenges, and opportunities. By making this investment, together, we can then build a prosperous relationship. Without doing so, it can be hard to establish the trust needed to collaborate equally and fruitfully.

How did you end up back in research after spending time with Microsoft?

My career’s second decade was on the supply side of the market. At Microsoft and TechInsights, I succeeded in developing products, managed partner programs, and delivering on go-to-market strategies. Something I’d advised on in my first decade at IDC, but with little real experience.

So, after developing skills as a business leader responsible for multi-million dollar P&Ls and a global workforce and taking some time off after leading the efforts to sell a line of business, research just came naturally to me. I found myself interested in a more holistic view of strategy, from product design and development to competitive go-to-market to contracting and negotiations.

Contracts, I have found, are often overlooked by business and tech leaders. While they can be boring, having read 1,000s of them, I have a good sense of what to look for in terms of fairness and remediation. Understanding the legal aspect of the relationship must be a big part of any cloud strategy. Technology and business leaders should be investing time to study the impact their supplier agreements may have on success!

You’ve chosen to focus heavily on the Cloud at HFS… can you share your passion here? What are your goals?

Technology has been seen as a game-changer to business models and service delivery for the past 2 decades. In fact, being a fan of Star Trek continue to be amazed at how much of today’s technologies were dreamed up by the series in the 60s. However, one thing Star Trek missed was the importance and power of the Network.

It is the Network, not called the Cloud, that is changing the game. This goes beyond computing power and ease of delivery/access; it means this nearly ubiquitous platform can power the workforce and business process needs of organizations, governments, and supply chains. At HFS, I’ll be working to link the One Office, Triple-A-Trifecta, and native automation efforts into a context that both the technology leader and business leader can execute upon.

Exciting stuff! And very meaningful as we toss “digital transformation” out the window and focus on a real evolution of the business, powered by process excellence and underpinned with Cloud technologies.

What role do you see analysts playing as we emerge from this pandemic? Same old game, or is something new brewing?

Obviously, my perspective is biased based on my experiences and how I have been successful. I believe companies will benefit the most from analysts with backgrounds as business leaders themselves. I also believe the Cloud is fundamentally a state-less technology; as such, possessing global experience is essential to adding context to those selling, buying, deploying, and supporting these strategies.

I like to think of myself less as an analyst and more as a part of a strategic team of advisors. Articulating the “what next” in terms of workforce, process, and technology is what an executive should value over just getting another opinion about how they address today’s problems in isolation.

This is what attracted me to HFS. I look at my peers and their experiences across industries, professional backgrounds, and geographic locations. We are well-positioned to offer wisdom over just intelligence. And this is what I feel an organization should be seeking these days when it seeks to augment its data and insights with an outside 3rd party.

What do you think we’ll be talking about when we gradually revert to a world beyond our screens? Will we get a resurgence of energy and excitement, or will we crawl out of our caves blinded by the sunlight?

The fundamental change is that the business knows that the Cloud is no longer a digital service delivery tool. Instead, it is essential to service, workflow, employee and customer experience, and success. Customers and employees are intertwined in a cloud-based supply chain. They do not need in-person experiences as often, nor will they seek them out. Gone are trips to solve tactical problems, glad-hand a business opportunity, or pitch an early-stage project.

Our screens are part of the business now. When travel returns, it will be for strategic reasons, such as fostering trusted relationships, motivating our teams, and gaining experiences by listening, not selling, to the other person.

Well, it’s great having you onboard Joel – looking forward to some intense research in 2021!

In today’s world of constant fake news it was refreshing to get some real news that literally made me choke on my 57th microwaved frozen chicken jalfrezi of the year. The fact that this real newsemanated from the Daily Mail (the UK equivalent of the New York Post or Air India’s in-flight magazine) was an indicator of how bad today’s media has become. Also, the fact that my head of marketing actually reads the Daily Mail gives me serious concerns for our 2021 marketing strategy…

Anyway, let’s get to the point. Our Chancellor of the Exchequer (CFO for you corporate types), “Dishy” Rishi Sunak is married to the daughter one of India’s IT industry’s founding godfathers, none other than Akshata Murthy, daughter of Narayana Murthy, the man who created Infosys. Like that happened and no one’s noticed until someone at the Daily Mail discovered this… and they wed in 2009.

The UK is in a mess so bloody big we need to redefine “mess”

If a depression-driven Covid catastrophe wasn’t bad enough, the mother country is going into a catatonic depression so bad, it may lead to an economic fossilization (that is my term for something worse than a depression) when we throw a no-deal Brexit into the mix… due end of 2020.

Anyone observing the thrilling performance of the Indian-heritage service providers this year will observe how the leaders have somehow kept the IT outsourcing industry actually growing a little bit, despite a predicted 8-10% nosedive that analysts many predicted. And this owes a huge amount to its standout performer of 2020, Infosys, which has chugged along signing megadeals and reinforcing its commitment to the cloud at a time when enterprises are desperate for a partner to help them pivot at breakneck speed into the cloud model.

Anyway, as a disillusioned British born analyst (and global citizen) I suddenly see hope…

I have a lot more faith in these entrepreneurs from Bangalore than the current old-boys network running Her Majesty’s economy into the ground. I always knew Rishi was the only smart one in there, and now we have the evidence.

So… now good old Infosys has no choice butto bail us out as they married into… the UK!

I am sure they will appreciate some free advice on the governance team that can drag us quickly out of our current predicament, so here’s an initial strawman architecture:

UK Prime Minister: Ravi Kumar S. No one spins it better than old Ravi… all he has to do is bulldoze our media with pics of his new baby girl all over twitter and have us guessing forever on the mysterious “S”…

Chancellor: Pravin “UB” Rao… this man can keep a ship sailing through any storm. This current crisis stuff is child’s play compared to rogue CEO’s in private jets and dodgy Israeli automation purchases..

Head of the UK Coronavirus Task Force: Vishal Sikka… time to dust off the former CEO to convince the UK public that we needn’t worry about Covid as “AI will provide the answer” (after showing up 30 minutes late to every briefing).

Brexit Secretary: Salil Parekh… who better to carve us out of the EU than the king of the carve-out deal himself? He’ll even do the deal on the golfcourse showing the rest of Europe how it’s done.

Head of Cybercrime: Mohit Joshi... who better to arm our cyber-defenses than the man who can iron-wall any bank still running on Cobol mainframes? Easy, just move all our sensitive data onto Finacle and the Russians and Chinese will go crazy trying to figure out what the hell we just did…

Vaccine Distribution Czar: Radhakrishnan “Radha” Anantha… who better to command the British vaccination process than InfosysBPM kingpin Radha himself, who will ensure everyone needs to “calm down and just focus on the outcomes”. If things get a bit dicey, he will take questions from his kitchen where we’ll be far more interested in what on earth his kids are sneaking out of the fridge while he’s too busy talking to us…

But what about Rishi himself?

Oh, he’s far too smart for us. Can’t you get him to take over from that Modi guy? Rishi makes money appear from magic, you know?

Today’s environment is based on rapid decisions to move processes and apps into the cloud as fast as possible to keep companies functioning in a remote-working economy. That means it’s all-hands-on-deck to use all available resources to make this happen as cost-effectively as possible. The principles of agile development have never been as important.

Cloud computing is basically the Internet being used as the system for delivering processes, software, data, and other services. Being ‘agile’ means being able to use all resources as and when required. It also means not having to use them when not being used, and not pay for them. So how can we expect today’s service providers adopt agile development to help our enterprises make the leap to the cloud as effectively and rapidly as they can? Let’s ask HFS analyst Martin Gabriel who led the recent Top 10 report in Agile Development Services:

Martin – why has agile become so talked about in the recent past? Hasn’t this been around for ages?

Yes, that is very much true. In a nutshell, due to the following reasons, it took center stage – a) Because of the agile success rate in software development space, and b) the traction in organizational agility. It has proved that agile methodology enhances productivity and alpha, and if adopted appropriately, it reduces overall cost over a period of time. The agile concept has come a long way, it has evolved all the way through software development, but now has branched beyond IT and other departments like marketing, legal, HR, and much more. As the concept is getting increasingly popular across business areas, companies have started to witness higher returns because of this. However, this was only feasible because of the embracement it garnered from C-suite members in recent times. That being said, not all big firms embraced it, companies like IBM and GE witnessed a drop in their revenues as per a report on “Market capitalization of big firms.” On the contrary, firms like Amazon and Microsoft, who adopted agile practices at the top level, have delivered significant results over a period of five years. Companies like Netflix and Spotify were born agile, and they were far from being bureaucratic and hierarchical and are one of the fastest-growing. I believe these are some of the key reasons in recent times it’s been discussed a lot in my perspective.

And has anything changed significantly with the pandemic, or is agile now even more relevant in the current environment?

As we know, agile software development is all about being iterative and collaborative at work. During the pandemic, few agile teams struggled but bounced back faster. But few of them were not doing that well before COVID as well, and the pandemic triggered its downfall too. On the other side, teams that performed well before COVID have developed trust due to the work from home coming in to the play and also plugged mental health management models in the team that shaped them to perform better during the crisis.

While we see this in the organizational perspective, certainly, the pandemic has pushed the organizations to play with an unfamiliar swiftness, and that is how organizational agility became inevitable in today’s environment. Many non-agile organizations adopted agile operating model out of necessity, and it has significantly helped them to cope with the crisis regardless of industries.

With agile operating model adopted completely or partially, companies led with a smooth transition, efficient work management, and met customer needs within set timelines. In fact, within an organization, agile business units performed significantly well than the non-agile business units. We cannot deny the fact that non-agile organizations struggled to manage the remote work environment and resource prioritization.

The Challenge of performing well in crisis with agile models does not end here. The real test will begin when the same organizations who adopted the agile way of working out of emergency might have to figure out the most sustainable model that suits them after things settle down. The current operating model was only developed out of emergency and was not a well-planned one in the long run.

So, what impressed you – and disappointed you – the most when you conducted the briefings and enterprise reference calls during the recent T10 report? Did you feel the industry has been making a lot of progress with agile or is it more “lip service”, Martin?

What impressed me – Well, I have lot to discuss on this, starting from enterprise adoption rate of the Agile methodology to success rate, client relationship, providers’ willingness to go overboard, and to my surprise, commitment and impressive client relations. This is where some of the mid-tier players were able to demonstrate and deliver better than the tier 1 players – this does not mean that tier 1 players were less impressive or have not wooed their clients. Sometimes the complex management structure takes away the perk and makes it intricate and challenging to achieve desired results faster.

Flexibility, when I say flexibility, here I am talking about the willingness to flex resources if needed, flexible pricing, free hands-on choosing resources for their projects, open environment where developers from providers’ side were able to push back if that’s not the right approach and the willingness to go out of the box rather than sticking only with the contract.

These are some of the positive angles that few providers were able to pull off.

What disappointed me the numbers they gave for their agile resources. While conversing on providers’ strength in their agile practice, it was observed that the numbers of trained agile associates were a little unrealistic. Few providers mentioned more than 80% of their application development work in agile, whereas few of its peers only mentioned around 35%. These numbers lie in two ends and difficult to analyze.

Large organizations are still focusing on pleasing clients instead of being true to the name of agile engagement. Few agile team members were unable to have difficult conversations with their clients, instead, they agreed to every task thrown at them without explaining the challenges behind. In fact, they did not create room to push things back if they were unrealistic.

In my humble opinion, clients are very mature compared to many service providers. They have vast know-how and understand the ground-level challenges and common market problems better and on top of that, they have a willingness to cooperate.

Sometimes, client references given by the providers refuse to participate as there were no prior intimations given. These instances reflect that providers sometimes assume clients are happy and ready to share happy testimonials.

Across providers’ offerings, frameworks, partnership ecosystems, and capabilities are the same. End of the day it’s about customer satisfaction, overall experience, and pricing.

Answering the last part of your question, the Agile model indeed progressed over the years. It has almost replaced the traditional waterfall methodology. The agile failure rate is only 8%. Yes, it has its challenges too. Initial costs, unclear objectives that lead to constant changes, scaling across different teams and locations, resistance to change, and lack of executive support are some of the challenges.

And which providers, Martin – in your view – distinguished themselves the most? And why?

Infosys, HCL, and Accenture bagged the top 3 ranks in our top 10 studies. Sometimes simple things make a huge difference, and in our agile study, that’s exactly what happened. I reiterate that customer feedback, pricing, and flexibility differentiates providers. Methodology, approach, partnership ecosystem, scale and breadth, IP, and accelerators are very close calls among the top players. It is tough to differentiate for buyers and even me as an analyst. Little you can make difference wherein the thought leadership, investment roadmap, and willingness to go that extra mile is the one that differentiates among the top players. Matter of fact, fourth, fifth, and sixth rank holders were very close to each other. They were equally good in most of the assessed parameters.

As we evolve rapidly into this new hyper-digital environment, how would you like to see agile evolve and a practice? What is your advice to young professionals in this space?

Well, agile is not limited to individual teams (say product development team) anymore; embracing the agile practice organization as a whole is the way.

Advice to young professionals – Coders who are developing agile competency will differentiate themselves and have a better advantage over others. Also, we are embracing organizational agility; therefore, an agile foundation or awareness is going to be inevitable.

Furthermore, some of the skills are often taken casually or being ignored. Agile team members must equally focus on developing soft skills like managing difficult conversations, the ability to present your work to a wider audience if needed. Being a good developer or coder isn’t sufficient anymore. Agile is about constant change and iteration and for that these skills are ideal.

And how would you describe the similarities between agile development and the rapid scaling up investments? How can we use agile to get to our “North Stars” faster these days?

In short, the Agile concept took years to reach where it is today. Even today, some of the top IT service providers agreed that only ~36% of their application development work is in agile. Similarly, scaling up agile has its own challenges. In the past, sr. leaders were very stringent in approving the budget. Last four-five years with proven agile results and an agile mindset, C-Suite members are open to scaling, and the COVID crisis further pushed the process.

Answering your second part of the question. We witnessed results in organizational agility over a period and it’s one of the big fuss in the industry right now. Also, in the recent pandemic, agile organizations were the ones who were able to swiftly move/adapt to the remote workspace than others. Leaving challenges aside, the benefits of organizational agility is faster adoption of changes, capitalization on new trends, and incline towards an innovative firm. I believe, in short, organizational agility is the best way to reach our North Stars, faster. There are a lot of steps and approaches to be followed, that is another discussion altogether.