One platform which has scaled new heights over the past year, geared to orchestrating processes in the cloud, is ServiceNow. One area that is becoming increasingly critical for these platforms is driving up the excitement of the leading – and emerging – services providers to train their staff to deploy, develop and help manage the solutions. Hence, it is no coincidence that we’re seeing SNOW rise in prominence with the service providers with ex-SAP chief Bill McDermott at the helm.

HFS’ IT services leader, Dr Tom Reuner, supported by analyst Martin Gabriel, have spent the past few months talking with an exhaustive quota of end-customers of ServiceNow, in addition to drilling into HFS’ customer perception surveys, to draw up the definitive Top Ten guide to ServiceNow Services in 2021. Premium HFS subscribers can access their copy of the report here.

So let’s hear a bit more from Tom about this evolving market…

Phil Fersht, CEO HFS: Tom – why has ServiceNow become the orchestration platform of choice for so many enterprises in recent times? What has changed to drive such a level of interest?

Dr Tom Reuner, SVP IT Services Research, HFS: Suffice it to say, Phil, the attraction of ServiceNow is in the eye of the beholder. For me, it is one of the key enablers for operationalizing the OneOffice. Let me peel back the HFS nomenclature for a moment. ServiceNow is the operational layer that helps organizations to deliver digital customer and employee experiences. In a nutshell, it is achieving this by offering workflows in the cloud that are underpinned by a single data model. But crucially, these workflows are cross-functional and organizations are looking to obtain that single pane of glass with all the operational data.

So what does cross-functional really mean? Many organizations started their journey with ServiceNow with IT workflows as they got fed up with the lack of agility of their often highly customized ITSM solutions such as Remedy that are still on-prem. But many organizations are expanding ServiceNow beyond ITSM toward IT Business Management or SecOps within IT, while others are literally taking the platform and leveraging it in business functions such as customer service, HR, and procurement. Thus, ServiceNow is a conduit for overcoming the organizational silos that we at HFS keep talking about. As one service provider put it, you have to earn your right in IT workflows to expand the platform to other business units.

Another strong alignment with the OneOffice mindset is that ServiceNow is delivering digital customer and employee experiences that delight folks rather than frustrate them. Those experiences could come from portals but increasingly are coming also from mobile devices. A good example is returning to work projects and even vaccination management as we are hopefully getting toward the tail end of the pandemic. You only get to high levels of customer and employee satisfaction if your operations are underpinned by consistent data sets and actions can be adapted easily.

How is the service ecosystem evolving around the NOW platform, Tom? What are you seeing from the major providers and the emerging niche firms?

There is an immense dynamism in the broader ServiceNow ecosystem. I would point to three major trends. First, clients are starting to scale the cross-functional journey with ServiceNow. We are seeing organizations managing GBS operations with ServiceNow end-to-end. They are taking the platform across HR, F&A, procure, and beyond. This is a far cry from the beginnings of ITSM. Second, ServiceNow is pushing an industry-led go-to-market. Thus, service providers have built out deeply verticalized offerings. Compelling examples are Operational Resilience in the financial services space and on the telco side, Network Performance Management offerings that get deeply integrated with the OSS/BSS landscape. And you can see those two trends clearly in ServiceNow’s financial performance. In Q4 2020 only 62% of new contracts were around IT workflows. And many of the leading service providers have an even lower percentage of contracts around IT workflows.

The third trend is the war for talent and with that, the unavoidable acceleration of M&A activity. Given the scarcity of talent, ServiceNow pure plays are being acquired by the GSIs. The most recent examples are NTT DATA acquiring Acorio and Cognizant gobbling up Linium. Both pure-plays had a strong focus on the US market. But we have also seen private equity (PE) firm Sunstone Partners acquire three ServiceNow pure-plays (Evergreen Systems, Cerna Solutions, and Novo/Scale) to create a new pure play challenger with global ambitions. It will be intriguing to see how this new company called Thirdera will fare.

So against the background of those trends and developments how are service providers reacting to this and who is standing out from the crowd?

Pivoting to broader transformational programs where the platform is being taken beyond IT workflows into what ServiceNow calls ESM ( i.e. customer and employee workflows) and more recently even into industry-led solutions is where the wheat is being separated from the chaff. It is here where the leaders like Accenture, Infosys, KPMG, EY, and DXC Technology are standing out. Many clients are looking for more than just implementation services that are commoditizing fast and that are often driven out of offshore factories. Put in other words we are seeing the OneOffice mindset come through. Organizations are progressing toward a more holistic data model and are looking to drive workflows across organizational boundaries. Beyond the leaders Atos stands out as the leader in the “Voice of the Customer”, IBM has made significant progress and is building out deep industry solutions while LTI gets strong client references for highly scaled IT workflow projects.

However, outside of the usual suspects, the unsung heroes of the ServiceNow ecosystem are often the leading pureplays or boutiques. For example, Enable Professional Services is the champion in Australia and Asia with strong ESM credentials while Plat4formation is at the cusp of innovation in manufacturing and beyond. Cask excels with a transformation focus in the US market while GlideFast has a strong sales momentum in the same market as well as a high CSAT score. As an analyst engaging with these organizations is immensely rewarding as you glean so much more information about the market.

Has Bill McDermott made a big difference, in your view?

There many ways of looking at it, Phil. For starters, he is a brilliant sales guy. I remember him from my days at Gartner donkey’s years back when he was heading up sales there. Looking at it from the ServiceNow angle, Bill’s tenure marks a new phase in their corporate development. His predecessors built the core functionality and established the brand. The next phase is strongly accelerated growth. You can compare this to the evolution of Salesforce. Therefore, the next logical step is verticalization. Bill hasn’t devised the strategy but he is excellent at communicating it. He keeps talking about ServiceNow being the platform of platforms. Which is a clever way of emphasizing cross-functional workflows. Yet, those workflows only happen through integration with all the applications and toolsets.

Having said that, there is a bit of a cult cropping up. Almost all the service providers we talk to point to “having discussions with Bill” and quite frankly just drinking the Kool-aid. But as the platform is being expanded into completely new use cases, having this communication “magnet” is immensely helpful. And we should keep in mind that ServiceNow has always avoided being pigeonholed. It was never the ITSM company. If anything, not too long ago it positioned itself as the “cloud company”. Now the positioning crystalizes around “Workflows for the Modern Enterprise” and as mentioned, the notion of the platform of platforms. Given the heterogeneity of the capabilities, having a highly visible figurehead is immensely helpful.

We recently saw ServiceNow acquire one of the small RPA providers, IntelliBot. What was that all about Tom? Why did they opt for a small firm in this space and not go for one of the larger RPA firms?

What appears to get lost in much of the ‘excited’ commentary of the Intellibot acquisition is that we have to move beyond a siloed mindset. This is not about RPA or AIOPs. This should be about moving toward cross-functional workflows. Put another way, ServiceNow is not entering the RPA market. As with all its acquisitions, it is looking to re-platform the capabilities of Intellibot. Or put yet another way, it will not offer Intellibot as a stand-alone offer. The aim is to expand the workflow experience toward the automation of legacy systems. Intellibot’s low code credentials have the additional bonus of allowing users to create automation. Therefore, comparisons to the leading RPA provider are misguided. This is a tuck-in acquisition that allows the integration of legacy applications and data sources. As such, this is more akin to SAP acquiring Contextor. For SAP the direction of travel is opposite to ServiceNow. Rather than allaying concerns of clients to migrate to the new world of HANA, ServiceNow is the cloud-based innovation that is aiming to integrate with the plethora of legacy systems. They aim to offer a connector to all leading applications and tools etc. Deeper process intelligence capabilities are the next logical steps, but again only focused around ServiceNow data, not as a competitor to the likes of Celonis.

You invented the “Intelligent Automation Continuum” during your earlier days with HFS. Is that still relevant, or have you changed your thinking? Are enterprises starting with basic RPA before graduating to more sophisticated technologies or is something else happening?

As a failed historian, it is always a tad indulgent for me to go down memory lane. To some degree, I am amazed that the Intelligent Automation Continuum is still being talked about and that clients still find value in it. While the market has moved on, the thought-process behind the Continuum remains valid, I would argue. But as with many things, automation really is in the eye of the beholder. For me, Intelligent Automation was always about end-to-end process automation and the need to integrate and orchestrate both legacy technologies as well as innovative offerings such as the cloud. But I was expecting a convergence of IT and business scenarios. So much so that I declared “RPA is dead” back in 2016 just to make a point.

Looking at some of the more detailed discussions on the Continuum, the idea was never that you have to start with basic RPA to progress to more sophisticated technologies as you put it, Phil, but rather two other fundamental points. First, that all the approaches and technologies plotted across that Continuum are both overlapping and interdependent. Therefore, clients have to find ways of orchestrating those. Second, the direction of travel is toward unstructured data and probably less obvious toward less well-defined processes. Cognitive and artificial intelligence is meant to overcome the limitations of these two dimensions.

And with that, we are back to ServiceNow. The cross-functional workflows and the integration capabilities of ServiceNow’s Integration Hub are taking us back to those discussions to progress toward end-to-end automation and decouple routine service delivery from labor arbitrage. We have to re-focus on those outcomes rather than getting side-tracked by the task automation pushed by the RPA incumbents. It is here where the ever-expanding capabilities of ServiceNow are coming in. But to be frank, I don’t think the RPA camp has taken too much notice of how much ServiceNow has changed.

So finally, Tom, what will be we talking about in the next couple of years as we see AIOps matures and other data-centric technologies become more prominent? How are operational process solutions going to take shape?

For me, it is really building on the points that I was just trying to make. The focus should be on the convergence of IT and business and enabling this cross-functional mindset to overcome organizational silos that we keep discussing in the context of the OneOffice. But to get there, we need enterprise-wide service management and monitoring. Yet, we are still miles away from getting even close to that. There are many missing pieces on that journey. But I expect deep investments around operationalizing Data Science, be it around process intelligence or AIOPs. The focus must be on integrating disparate inputs including metadata from logs or data that is adjacent to the actual process. However, the ability to ingest disparate sets of information has to be matched by the ability to execute and ultimately automate actions. Over time we have to progress to the non-deterministic application of dynamic scripts. Thus, this is also more about the platforms such as ServiceNow and Celonis, rather than about all those points solutions. I am tempted to close out with the thought process behind the Continuum: the focus on end-to-end automation and the need for integration and orchestration. But then again, markets rarely evolve rationally.

HFS Premium subscribers can click here to access their full copy of the 2021 ServiceNow Services Top 10 Report

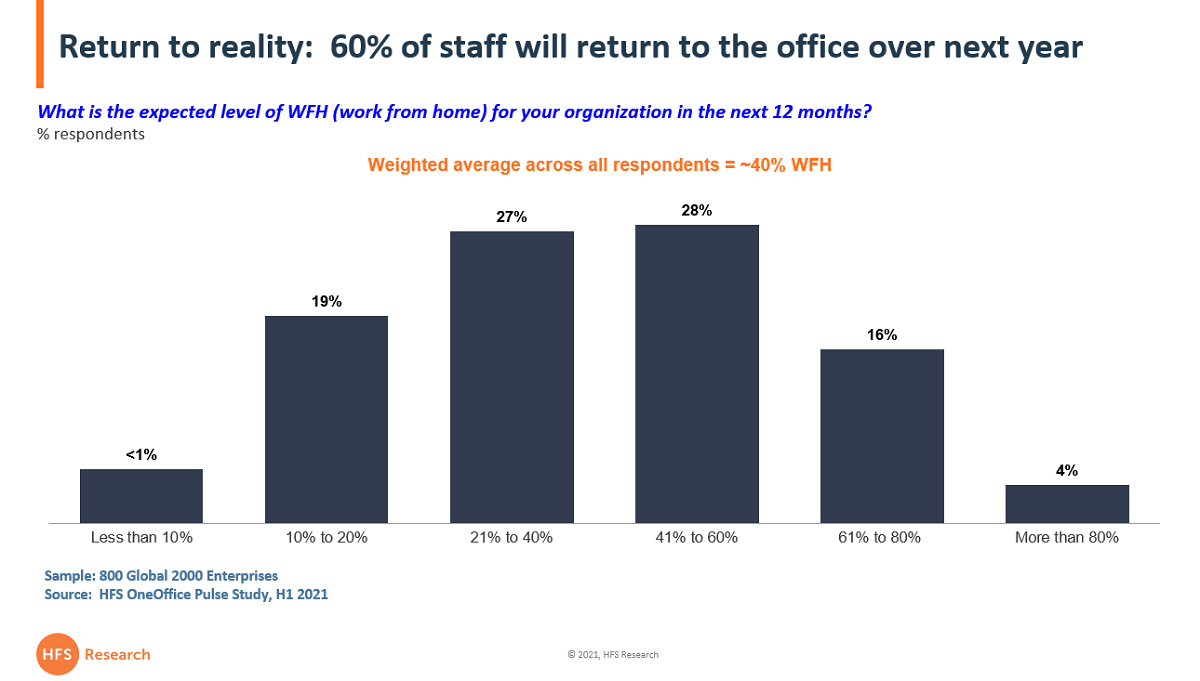

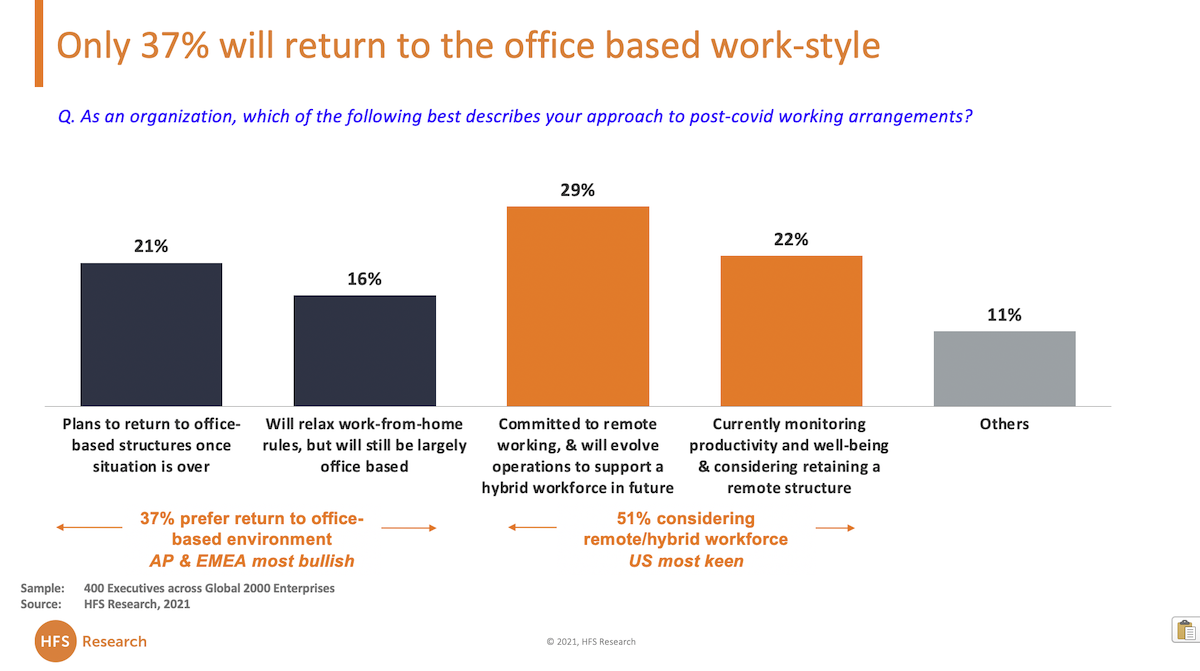

What a difference six more months of staring into the digital abyss has made

When we interviewed leadership from 400 Global 2000 enterprises at the end of last year only 37% saw them returning to an in-office environment. Our very latest HFS Pulse study, covering 800 Global 2000 enterprises, clearly shows a marked shift towards sending staff back to the office, with a 60% ratio of staff expected to be office-based over the next year:

We’re entering a hybrid reality, where digital and physical work cultures are blended

The digital exuberance of 2020, where declarations from many leading enterprises – the likes of Unilever, Hitachi, Mastercard, Google and Amazon – that they had become “work-from-anywhere enterprises” is clearly losing steam as so many enterprises have struggled to maintain a motivating, dynamic culture. Employees – from leadership down to interns – are burned out with the sheer monotony of a 100% digital environment and the inability to whiteboard ideas, share ideas, collaborate on process design and embrace emerging tech. This is especially the case with Gen-Z and Millennial staff who are desperate to get back to an office environment. In fact, many are choosing to work for firms that are embracing an in-office culture – something we have already seen happening aggressively in the call center environment (download POV here).

Bottom-line: We’re seeing a significant “digital-flip” towards an in-office model

We can’t deny the experience of the last year has driven a genuine need to configure business operating models to function in a remote virtual environment, as most businesses simply can no longer limp along with on-premise systems, fragmented processes, and an inability to operate in the cloud. However, as we evolve towards a new reality where we can really visualize a physical future for businesses, it’s also become clear that businesses are struggling to function entirely in the cloud and depend more than ever on a people-driven culture. Why is this?

Businesses thrive on people and technology empowers us, not dictates how we work. While many businesses struggled – or failed completely – during the pandemic, many have thrived as costs have been decimated and a return to growth has created so many new markets to exploit and customer demand to satisfy. This has also created a highly fluid job market, where people can get hired rapidly over Zoom and staff can dictate where they want to work. Companies with strong, dynamic leaders who inspire staff to learn new things, collaborate together, and focus on purposes beyond mere profit and efficiency are fast becoming venues where ambitious staff want to apply themselves. While much can be achieved in a pure remote model, it’s simply not sustainable for a healthy, energizing work environment in the medium-long term. Running data and processes in the cloud is critical to keep companies operating effectively, but those are merely the baseline table-stakes to survive in this new hybrid reality. Technology is critical to provide the infrastructure to exist, but it doesn’t dictate the business model… people do.

There is only so much you can achieve remotely. We’ve talked to hundreds of executives over the past year, and they all complain about the same thing – they are managing an almost-unmanageable amount of internal meetings over video calls, simply to keep the wheels on basic task management and accountability. Simply put, it’s becoming increasingly complex and awkward to run business operations in a remote model where training is a huge challenge, where motivating people is almost impossible, where getting beyond the basics of keeping activities functioning is a huge challenge. Communicating, collaborating, idea-sharing, white-boarding etc are critical for taking businesses forwards and driving real innovation. They are also critical for helping employees become comfortable with change, to be comfortable with automating mundane elements of their jobs, and to become adept at embracing ways of accessing the data needed to exploit market opportunities. With industry lines blurring, supply chains fragmenting and new opportunities and challenges springing up at a breathtaking pace, the time to bring people back together is fast-arriving, and so many enterprise leaders are now seeing this in spades.

Rajan Kohli is quite possibly one of the coolest and calmest global leaders in today’s services industry, at a time when the speed and the pace of change bounce between hot and scalding. Are things moving as fast as clients want? And what about the internal pace of change? Wipro has recently completed both a major restructuring under new CEO Thierry Delaporte and the eye-catching acquisition of Capco in the past few weeks, so how are they really pulling it together to deliver the value clients so urgently seek?

Rajan now leads Wipro iDEAS (Integrated Digital, Engineering and Application Services), one of the firm’s two new global business lines, so I spent some time with him to wade into those waters…. after his daily run through Central Park. Here’s a peek into the conversation…

Phil Fersht, CEO and Chief Analyst, HFS Research: It is great to have you back on here again Rajan. I think we last spoke on HFS about three or four years ago, so quite a lot has happened since then with you, your career, and with Wipro. For the benefit of everyone here, maybe you could just give us a rundown on yourself again, and where you have evolved from, to the position that you are in today. Then we can talk a bit more about how you are hoping to take things forward in the new setup at Wipro.

Rajan Kohli, President and Managing Partner, Wipro iDEAS (Integrated Digital, Engineering, and Application Services Business Line): Absolutely. The pleasure is all mine, Phil. I think, when we last spoke, I had just taken over as the leader of Wipro Digital, and Wipro was making a big bet on digital in that space. Prior to that role, I was head of banking and financial services, and before that, I had been the Chief Marketing Officer at Wipro. But most of my time had been in leadership roles in our financial services business. We set up Wipro Digital in 2014, and I’d been leading Wipro Digital until a quarter back.

If you remember, Phil, our initial hypothesis was that in Wipro Digital we’ll develop capabilities that are differentiating, capabilities that don’t currently sit in any part of Wipro, and then, over a period, we’ll move other parts of Wipro under Wipro Digital so that we can do an end-to-end digital proposition for our clients. And that is the journey we were on.

“Through the massive restructure that Wipro had… we added the digital experience parts of Wipro’s business into Wipro Digital, then we added application modernization. With this latest reorganization, Wipro has now added all of engineering, all of applications, all of data also under this new group called iDEAS.”

Earlier this year, through the massive restructure that Wipro had, we have continued that journey forward. Initially, we added the digital experience parts of Wipro’s business into Wipro Digital, then we added application modernization. With this latest reorganization, Wipro has now added all of engineering, all of applications, all of data also under this new group called iDEAS.

The new global business line of iDEAS consists of Wipro Digital, Apps and Data, and the Engineering and R&D business of Wipro. We have also brought Industry Domain and Consulting under the iDEAS business line.

This is now the new construct, where we have two global business lines, iDEAS, and the second one is called iCORE, which is infrastructure, operations, and cybersecurity.

Phil: So it has obviously been quite the year now. We have been operating in a work-from-anywhere scenario quite literally, and I think a lot of the theory and desires that we spoke about over the last decade, some of that is now coming into practice for many enterprises, for many of our own companies, and into our own lives.

What do you see is the real speed between the desire for change and the actuality of the pace of change in the market? Are things moving as fast as clients want, or are you seeing a mismatch between what people want to get to versus where they are heading?

Rajan: That is a very good question. I think all our clients, enterprises, post-COVID, want to move much faster. They want to do more digital, but the gap between their desire and ability is what I will call digital fitness. It is comparable to having a desire to run 100 meters in 10 seconds, but not having the capability to do that. The gap really is fitness.

“All our clients, enterprises, post-COVID, want to move much faster. They want to do more digital, but the gap between their desire and ability is what I will call digital fitness. It is comparable to having a desire to run 100 meters in 10 seconds, but not having the capability to do that. The gap really is fitness. …Those who had modernized their IT application and infrastructure were able to achieve much more.”

I think the realization is there, among our clients now, that they need to modernize the core to really become a digital enterprise. That came to the fore during COVID because, if you talk to most of the CEOs and CIOs, the biggest issue was the IT, the application, the legacy nature of the landscape, and just the sheer amount of effort and time it took to do simple things. Those who had modernized their IT application and infrastructure were able to achieve much more.

There are good examples of enterprises that were able to pivot very fast. Best Buy was able to offer curbside pick-up very quickly, and Target could do a lot of omnichannel business. Chipotle – their stock did really well because they were able to order on their app and offer pick-up from the stores. A lot of enterprises took advantage of the scenario to gain share. There were many others who suffered, and that is the difference that I call digital fitness.

Phil: I think you have had your own shift in strategy, Rajan, where you have moved much more in a geolocation strategy model than maybe what you were doing before. How do you think that is going to go as you work through a lot of change with your clients as well?

Rajan: I think the current model of geo-based structure is a good one. I will tell you two or three reasons why I believe it is a really good one.

“The industry definitions of the past no longer really hold true. … For us to be able to serve our clients the best, it is better to organize against a particular account and bring all of the Wipro value proposition into the account, irrespective of the industry boundaries of the past.”

Number one, if you really see, the industry definitions of the past no longer really hold true. If you look at Amazon, of course, it is a favorite example of all. Is it a tech company? Is it a retail company? Is it a delivery & logistics company? It is all, right? Similarly, if you look at Zillow, they want to compete on the buyer journey, so why would they not want to offer mortgage loans, if possible? Do they now become a financial services company? Look at Walmart, they want to get into banking and financial services. For us to be able to serve our clients the best, it is better to organize against a particular account and bring all of the Wipro value proposition into the account, irrespective of the industry boundaries of the past.

Secondly, through this reorganization, Phil, we have brought our accounts and account management team closer to the customer. Client relationships were reporting level four or level five below our CEO. Now, they are on level three, and some on level four, and so we have brought ourselves closer to the client.

While we have become regional, we also need to stay global, because we do not want our capabilities to get siloed. So, the global business lines are truly global. iCORE and iDEAS are two global business lines that give us the ability to learn something, to deliver something in one client, in one region, and then replicate it in another client, in another region. That is why I like this construct a lot.

Phil: In terms of internal transformation, as a OneOffice type of organization, I know there is a lot of work going on internally to really pull that together, as well. Can you talk a bit more about what you are doing internally to, sort of, reformat the whole way Wipro is operating in this economy?

Rajan: I would say two things, Phil. First, in the past, there were a lot of operations that were sitting outside of the service lines and were being centrally managed. Now all of that operational capability has been brought into the service lines. Service lines now can decide how much they want to hire, where they want to hire, at what price they want to hire, and equally how they build talent in-house. A lot of that decision-making has been given to them.

Second, for us to now operate this model, we need a much better fabric that connects our accounts and our business lines. [We] really have a very strong order-to-cash system which, by the way, also can be flexible as we integrate many of the acquired companies into our system. So, if company A has a particular rhythm, which is different from company B, we should be able to offer that through the flexibility in our system.

We have a program called Quantum, Phil, which is being led from the top of the company, and that is the fabric that will now connect us in this new organization.

Phil: Excellent, Rajan. So, what about the conversations we are having now? I mean, there was so much focus on digital before the pandemic hit, in terms of a lot of focus around design, interface, and almost advertising-type businesses, as we were taking enterprises through that journey. But has that conversation shifted, in the last year, in terms of what the top priority is now? Is it maybe not quite as important as it was?

Rajan: Well, there are things that probably have become more important now that were not as important in the past. Modernization is one of them.

In the past, modernization was seen as IT’s requirement. It was not seen as a business requirement, because the functionality did not change. Business always worried about paying for modernization, because they paid for features and benefits, and modernization is more speed. They did not see the importance of it. Post-COVID, I think they have realized the need for speed, and hence the modernization, so that has changed.

“What has changed is Cloud. Pre-COVID, cloud was still important, but people were looking at cloud as more of an infrastructure-as-a-service play, a cost reduction play, or a flexibility play. Post-COVID, it is a play for speed as well.”

Second, what has changed is Cloud. Pre-COVID, cloud was still important, but people were looking at cloud as more of an infrastructure-as-a-service play, a cost reduction play, or a flexibility play. Post-COVID, it is a play for speed as well. We see clients realizing that a cloud-based environment offers them the ability to go live faster and better with their new features to market. I think that cloud has become a lot more application and domain-centric, compared to just pure infrastructure-centric, and we are seeing that shift, post-COVID.

And last but not least, in the immediate aftermath of COVID, everything was about access, “I need to reach my employees; I need to reach my customers; how do I do that?” A lot of spend went in that direction, but now it is about a sustained performance. I think that journey obviously was always going to be a little short-lived, because people have achieved what they needed to achieve in the first six months, and now they are looking for more sustainable differentiation, post-COVID.

Phil: As we look at this great return-to-work that is going to hopefully unfold in the next few months, maybe six to nine months, how do you see that taking shape? Are you seeing us going back to similar office-based scenarios as before, or something very different happening? We have seen Unilever, we have seen Amazon, and Microsoft,… a lot of companies come out and declare that they are now work-from-anywhere/work-from-home businesses and that they are relying less on real estate and things like that. Do you see a different scenario unfolding as we watch a return-to-work happening?

Rajan: Yes, I do not expect us to go back completely to the pre-COVID scenario. I believe this is one of the positive effects of COVID, and a lot of that will stay. Just think about it today. You know, over the last nine months, almost 90% of our workforce has been working from home, yet we are delivering on our SLAs, clients are happy with us, and they are giving us more business. You saw our results over the last quarter – we are growing. I believe a lot of this will stay.

But we are in a services business, which means that a lot of our ability to work from home is also dependent on our clients’ decision-making, so to that extent, we will be dependent on what decisions they make. I have absolutely seen many of our clients that have made long-term announcements around not doing more than 50% from the office, so we will stay connected to that.

On our shared staff, or back-office staff, who are either not directly managed by the client or not directly delivering work for our clients, we expect a vast majority of them to continue to work from home partially. So, they will work a week from home, come to the office a couple of days, then work a week from home, etc. I think it will evolve, but it will not come back to where it was in the past.

Phil: Yes, I think our data is telling us something similar. I think only a third are looking at a complete return, and most are looking at, as you said, a different, more phased, hybrid model as we evolve. Does that change how you look for talent, the types of people that you are looking for, in your own organization, your own areas, and maybe your client areas as well? Are your needs shifting now? Are you looking for a different profile of people than you were?

Rajan: Yes, we are looking for a different profile of people. It is not just to do with post-COVID work from home, but over a period, this shift has been happening. Hence, we are looking for people who have greater learnability. Very clearly, we cannot define where technology will go two, three, four years down the line. People need to be responsible for their own destiny, so they also need to have learnability; they need to be able to pick up new skills.

The second is collaboration, and that part is now even more important. Because we are working from home, remotely, via video conferencing, the skills that you require to engage with people and collaborate are a little bit different, and even more relevant than in the past. Collaboration is thus important.

“Diversity has always been important, but one thing that both COVID and the movement in the US have brought forward, particularly over the last six to nine months, is the fact that diverse teams are necessary. Within Wipro, we have doubled down on diversity with very, very specific initiatives to drive diversity at the leadership level.”

Third, diversity. Diversity has always been important, but one thing that both COVID and the social justice movement in the US have brought forward, particularly over the last six to nine months, is the fact that diverse teams are necessary. Within Wipro, we have doubled down on diversity with very, very specific initiatives to drive diversity at the leadership level. Even if you see some of the recent hires we have made at level one, which is CEO minus one, and level two, CEO minus two, they come from all walks, and bringing more women into leadership is very important.

Phil: Yes. And you see this return to work evolving, and maybe the removal of borders in businesses now. They are far more globalized.

You made an acquisition recently of Capco, Rajan, which is the largest acquisition I think Wipro has made. There seems to be a lot of focus around building out more client-side onshore competency now in the system, as well. Is that part of the thinking, globalizing the model?

Rajan: Yes, globalization of the model was a journey we were on over the last couple of years, especially as you move upstream. As you move more into the consulting and the design phase, we needed more globalization.

“Capco, which is the largest acquisition Wipro has ever made, helps us… fill the continuum of think it, design it, build it, done it – that end-to-end continuum. We will continue to move and localize, and not just in these countries but also other delivery locations globally, outside of India.”

Capco, which is the largest acquisition Wipro has ever made, helps us do that, and helps us fill the continuum of think it, design it, build it, done it – that end-to-end continuum. We will continue to move and localize, and not just in these countries but also other delivery locations globally, outside of India. Eastern Europe, for example, is of interest to us, and other [areas]. Mexico has been growing for us. We will continue to do that.

Phil: Right. So at a personal level, who have been the big influences in your life and career, as you have evolved? You have had a successful rise, Rajan, particularly in the last few years. Who would you credit for that, in terms of influencing your motivation or your viewpoints? Or, just in general, who helps drive your thinking?

Rajan:Yes, I would say two people. One, of course, my mother. My mother was a teacher. She really focused on imparting the right values in me, and I saw that in how she operated day-to-day.

“I have had the great privilege of working very closely with Mr. Azim H. Premji, Wipro’s founder, and seeing him in action. Anybody who has worked with him, even for a very short duration, would tell you that there is so much to learn from the great person he is,… and how willing he is to ask any question if he believes that can make him better and make the company perform better.”

And the second [influence], having spent 25 years in Wipro, I have had the great privilege of working very closely with Mr. Azim H. Premji, Wipro’s founder and seeing him in action. Anybody who has worked with him, even for a very short duration, would tell you that there is so much to learn from the great person he is, from how he carries himself, how humble he is, how he challenges himself, and how willing he is to ask any question if he believes that can make him better and make the company perform better.

Phil: Absolutely. And I was absolutely amazed at the level of personal investment he has made in India, its infrastructure, and also even in COVID relief. He has donated more money than many of the richest people in the world like Jack Dorsey at Twitter. They have not actually sacrificed as much investment in this as Azim Premji has.

I was quite amazed at how he runs a tight ship, both as a business and personally. He is an incredibly generous man, and I think a lot of that has gone unnoticed for a long time. He has done a lot to be very proud of, and his contributions to India, so I am not surprised to hear you say that he has been one of your influences there.

This has been really nice to catch up and see your personal successes, as well as Wipro finding itself with some good energy and direction coming out of this pandemic economy. I look forward to catching up with you in the not-too-distant future to see how the new acquisition, and maybe more acquisitions, are embedding, and how this global model is treating the company.

Rohan Kulkarni is Research Vice President, Healthcare, at HFS

We’re firmly on our path to view the world through industry lenses at HFS research, as we see value chains across sectors merge, and the needs to be hyper-connected changing before our eyes – with suppliers, customers, partners, governments, etc grouping into new value ecosystems as the world finds its feet post-pandemic.

Who could have predicted the reinvention and emergence of food services as a whole new industry, such as the complete digitization of banking and retail, the shift in insurance to becoming a sales/marketing-driven industry, and the reemergence of the travel industry in this pandemic and post-pandemic eta? But perhaps there have been no more fundamental changes to an industry value chain than what has transpired – and continues to evolve – in healthcare. The need for rapid, quality patient data, economic data, cloud migration, and supply-chain reinvention has never been so critical to driving government, enterprise, and individual decision-making in the world of health, life sciences, and pharmaceutical production.

Without further ado, let’s delve into the views, ideas, and plans being driven by our latest analyst addition, Rohan Kulkarni, fresh from his accolades as a master of perfect pints…

Phil Fersht, Founder, CEO and Chief Analyst, HFS. Before we get to all the work stuff, Rohan, can you share a little bit about yourself….your background, what gets you up in the morning?

Rohan Kulkarni, Research VP Healthcare, HFS. The opportunity to participate in the healthcare ecosystem is personal to me. Recognizing that US healthcare is sub-optimal across the key dimensions of cost, health outcomes, and experiences will impact me and most of us in the most personal ways as we grow older requires us to lean in and help make it better. I want to influence drivers that could make the care construct better in some meaningful manner.

I have been in the industry, getting on a decade and a half, leading strategy at multiple fortune 500 companies, being a product management executive & CIO at 2 different health plans while having consulted across the ecosystem. These opportunities have highlighted that the health & healthcare industry is unique in its ability to only get better in a participatory fashion. It’s not just a doctor and patient equation, but rather needs all of us to do our part to stay healthy, be good patients when sick and when we get better, to stay that way. Its ongoing work for all of us all the time.

Phil – You’ve had a diverse career spanning several roles aligned to the healthcare industry… can you share some of your experiences over the years… what would you do all over again, and what would you definitely avoid?

Rohan – Yes, Phil, I have been lucky to traverse this path through the healthcare ecosystem as a journeyman. I am amazed at the paradoxes in the industry; on one end, the amount of money that is in the system is mind-boggling and sufficient to solve all our healthcare challenges with plenty leftover, yet on the other hand, it represents the only industrialized nation without universal health insurance. This pandemic has exposed the level of empathy the industry has, particularly the nurses and doctors whose altruism knows no bounds, yet our society today is challenged with misinformation and trust impacting care & its delivery. My point is that the healthcare industry is meant to solve a polymathic problem and we are still scratching the surface in so many ways despite all the advances.

As I indicated earlier, I have been privileged to journey through the ecosystem, meeting some wonderful people, accomplishing things that made me proud, contributing to helping reduce costs & optimize resources, and most importantly finding platforms to drive awareness to draw in more people to participate in the improvement of the ecosystem.

Phil – How critical is the role of services and technology in the healthcare industry during this time – has it changed significantly?

Rohan – I think technology and its enablement through services as we know it has been a cornerstone of healthcare’s evolution for the better part of 2 decades. As the population grows, particularly the seniors, and the prevalence of chronic conditions worsens without any evidence to suggest a radical change in behaviors, I would say that the role of technology and services in healthcare is critical, perhaps only next to what clinicians can do.

Yes, I think it has changed significantly from how data is captured and analyzed and used in diagnosis and care protocols, how it can keep patients connected to clinicians for real-time interventions, how fast we can develop vaccines, and much more. The speed from identification to solution to post solution maintenance, in my view, has been the hallmark of the last decades’ extreme technology focus on healthcare.

Phil – What role do you see analysts playing as we emerge from this pandemic? Same old game, or is something new brewing? How do you intend to cover the healthcare sector?

Rohan – Health & healthcare’s success, in my view, is defined by the quality of life attributes, which will require democratization of the ecosystem and the broad participation of everyone. A key focus of that is driving awareness and engagement to help people, communities, enterprises, and governments appreciate different perspectives. To be able to bring various stakeholders together, drive robust debates and influence good sustainable solutions. I think this next chapter for analysts will differentiate between the good ones who will challenge the status quo and raise the bar, collaborate and influence industry solutions and those that will be critics.

My approach is going to include a few dimensions;

coverage expansion to include the entire ecosystem beyond the health plans and life science that we currently cover to healthcare providers;

a focus on digital health through the intersection of Healthcare & Triple-A Trifecta change agents – AI, automation, and smart analytics as well as mobility and virtualization

Healthcare is a polymathic problem and will require a polymathic solution; as such, I will cover healthcare’s intersections with climate change, societal changes, the food we eat, the impact of the way we work (e.g., OneOffice), and more that impact the social determinants of health.

While I do have faith in my fellow humans, I do suspect that at some point here shortly, the pandemic will be history, albeit a painful one for many. It will likely get people to go back to their old habits with perhaps a few non-material changes to their lives. As such, it is critical to driving awareness in more meaningful, personal, and even in your face ways so that together we can chart a better path forward.

Phil – What do you think we’ll be talking about in healthcare when we gradually revert to a world beyond our screens? Will we get a resurgence of energy and excitement, or will we crawl out of our caves blinded by the sunlight?

Rohan – I think that depends on where in the world you are. In the US, we were already down the path of being virtual in healthcare, and the pandemic certainly accelerated it. I suspect that momentum will continue where physical interventions are not necessary, such as primary care, nonsurgical specialist visits, etc. I believe after the initial surge of visits to the dentist, ophthalmologist, gynecologist, etc., human behavior will likely reverse to the mean, to return to most pre-pandemic behaviors. Now given the fact that we are unlikely to be at herd immunity any time soon and will likely need a booster vaccine come fall, I think a true post-pandemic scenario is still evolving.

Phil – Thanks for sharing your plans with us, Rohan. Excited to learn more from you as you get bedded in with us!

How many of you even knew Earth Day was on 22nd April? And even if you did, did you care?

If there is one lesson we will eventually take from Covid, it’s the paranoia that government and business leaders’ now live with: a constant fear of being caught cold by a crisis like this, ever again. This paranoia must spur them to preventative action rather than a reliance on their ability to deliver rapid treatments. Those treatments of the symptoms simply paper over the deepest cracks of the causes – problems that remain unsolved despite all the debt we’ve incurred.

Barring future pandemics and world wars, which seemingly can be treated by throwing extraordinary amounts of money into science and military coffers, the next looming crisis is that of a climate meltdown. This offers the opposite problem – where the only cure is through smart and painful prevention, not quick-fire, after-the-crisis inoculation.

Sustainability must become a native part of businesses, policy, and our day-to-day lives

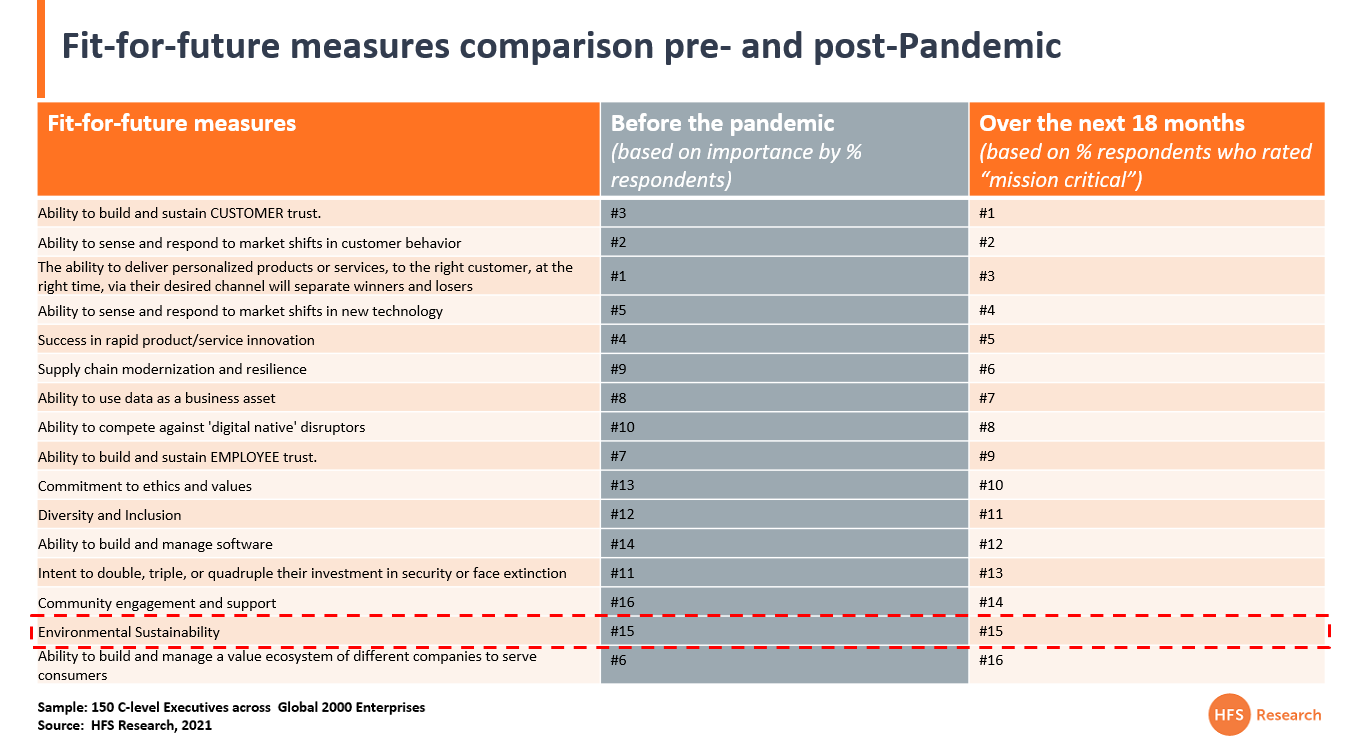

This means people need to be educated, they actually have to listen and then change their behaviors. No-one really took the threat of nuclear war seriously until the horrors of Hiroshima and Nagasaki were experienced. The world was able to recover from the horrors of ‘limited’ nuclear war, the experiences, hopefully, proving to be preventative for many more decades to come. But there is no second chance if we continue to destroy our planet. There can be no “lessons-learned” when the world runs out of water…. Sadly, our recent study of 150 C-suite executives across the global 2000 shows us that sustainability only ranks fifteenth as a “fit-for-purpose” measure – no change at all from pre-Covid times:

In this vein, we had our roaming story-teller Nischala Murthy Kaushik spend time with analyst Josh Matthews, who spends a lot of time thinking through how we tackle sustainability and climate change, in addition to spending his spare time as a counsellor on Cambridge City Council in the UK…

Nischala Murthy Kaushik (CMO, HFS): Let’s start with the basics, Josh… What is the definition of ‘sustainability,’ and why is it important in 2021?

Josh Matthews (Assoc Research Director, HFS): The best place to start by checking out the UN Sustainable Goals. These 17 Goals cover all the ambitions we should have as a planet, whether its tackling climate change, lifting people out of poverty, restoring and protecting biodiversity, or eliminating inequality. These challenges don’t stand alone—they’re heavily interconnected. These are all challenges we still face in 2021. These are all challenges we’re likely to face for decades to come. There’s so much under the sustainability umbrella—but can broadly be split into environmental, social, and governance (with a financial sustainability element) factors; many (businesses especially) refer to “ESG” as a way of indicating that sustainability is about more than just climate change, and how tightly intertwined all 17 Sustainable Development Goals are.

Nischala: The theme for 2021’s Earth Day (22 April) was “Restore our Earth”. How does the theme of sustainability really help in restoring our Earth?

Josh: There’s a scientific and internationally agreed need (The Paris Agreement) to reach net-zero globally by 2050 to have a chance of avoiding further irreversible global warming and climate and ecosystem breakdown. If we don’t reduce our emissions to net-zero by 2050, we’ll have lost any chance of avoiding global warming above 1.5 degrees (since pre-industrial times). This will not only cause extreme and erratic weather and make more of the planet uninhabitable, but it will also continue to break down natural ecosystems: oceans and reefs, polar regions, jungles and forests, and so many more. Biodiversity will disappear as habitats, and food chains will collapse. Restoring our Earth means avoiding this. But it also means actively improving biodiversity (and the planet in general) from where we are now—not just stopping the harm.

Nischala: Do discussions around sustainability come up in your interactions with clients? what are their top-of-the-mind questions and challenges?

Josh: Yes they do, Nischala, Many enterprises across the globe are committed to sustainability in various forms (for example, become net-zero carbon or committing to a target like 2030) and some demonstrate it through company policy or corporate level programs with a dedicated leader to drive this charter. As we emerge from the COVID-19 pandemic – sustainability and achieving more than just shareholder profit are becoming critically important for enterprise leaders (see Exhibit 1). Many, however, are struggling to translate their intent to action and impact. Many know that their customers are looking for sustainability in the products and services they buy—but still manage to stick with the status quo or not go far enough.

Our conversations with service providers do not fill us with a whole lot of confidence that the majority of enterprises are making the changes they need to make—despite marquee use cases and headline enterprises who have seized the sustainability narrative (Unilever is a good example). There is hope, however, as these same service providers hold the keys to making sustainable transformations happen – as they do in digital transformations. They can bring the strategy and design consulting, implementation, managed services, and technology to help businesses move along a pathway to sustainability.

Nischala: Has the election of Joe Biden as President of the U.S. made an impact, Josh?

Josh: Absolutely. And this is apparent in our service provider and enterprise conversations. There has been progressive regulation promised for some time across the world – and a desire for this from service providers and enterprises who are trying to be leaders in tackling climate change and pioneering all forms of sustainability. Investment in green technologies, infrastructure, jobs, and all manner of routes is beyond welcome – and other countries need to see this as a defining moment – where things change – and sustainability is no longer a future problem. Like enterprises, governments need to nail down roadmaps to decarbonize and reach net-zero. They also need to do the same in tackling all forms of sustainability. Technology and strategy, combined with implementation, need to come together.

Nischala: What trends around technology and innovation are you seeing in the world of sustainability?

Josh: Technology and innovation have two sustainability angles:

Firstly, they can both help businesses, governments, and individuals be more sustainable: AI and analytics (including in consumer apps) can improve decision making and optimization (of energy use, for example, which has a cost and carbon emissions benefit) and combinations of the internet of things (IoT) and cloud platforms can help measuring, monitoring, reporting, and optimizing of emissions. There are so many more examples.

Secondly, technology and innovation come with an associated carbon footprint which must be addressed. The electricity that powers computing and data storage must be decarbonized, and its consumption must be reduced. To address this, companies are sourcing more and more renewable energy to power their datacenters (or even producing it themselves) alongside improving their efficiencies. The supply chains which create technology products must also become more environmentally friendly (the mining of metals for batteries, for example), socially responsible (by eradicating modern slavery, to name only one challenge), and transparent (so that customers can have confidence that the first two points have been met, alongside their other requirements).

Nischala: What is it that large organizations can do to support the case and cause of sustainability actively?

Josh: Sustainability must become native to businesses. It must be an integral part of every decision from the shopfloor up to the CEO’s office. If there’s one concrete action to take away from this, it should be building a roadmap to decarbonize their carbon footprints. Measure your current footprint, and then plan how you’ll reach net-zero by 2050 at the ABSOLUTE LATEST (as far in advance as possible!). This includes your own direct and indirect emissions, but also those throughout your supply chains (often ). For example, direct emissions can be reduced via process optimization and redesign, indirect emissions could be decarbonized by sourcing more renewable electricity, and procurement processes can be adapted to ensure suppliers meet the highest sustainability standards to improve scope 3 supply chain emissions.

Nischala: Are there any specific initiatives that you are doing at HFS towards this cause?

Josh: HFS has been talking about sustainability, and importantly the sustainability services ecosystem, for some time. Businesses and governments know they need to become sustainable—but many don’t know where to start or how to put plans into action. Service providers are the ones who’ll make this change happen—as we’ve seen them do through digital transformation work—through consulting and design, implementation, ongoing management of operations, and technology. The sustainability services ecosystem, however, remains fragmented and poorly understood by providers and enterprises (and governments). Keep watching the HFS Research space as we change this throughout 2021. The sustainability ecosystem needs to be mapped, defined, understood, and coordinated. This must happen soon so that service providers can bring their enterprise clients and partners along on their journeys.

Nischala: What is it that we can do as individuals to support this cause, Josh?

Josh: There’s so much, Nischala – and even small changes aren’t wasted. Some of the most important would be: walking, cycling, and using public transport to cut down on car use (and if possible switching to an electric car, or car-sharing); reducing meat consumption and generally shopping for the most sustainable options (locally sourced, low plastic, etc.); reduce, reuse, and recycle as much as possible; retrofitting homes (although expensive) lowers heating/cooling costs as well as carbon emissions.

Nischala: What are some of the best global online resources for anyone to read if they want to understand more?

Josh: We’ve been sharing plenty of our favorite resources and research over the last week or so (and HFS’ own research, of course!), and obviously so much more is out there. But my top 2 picks would be:

United Nations (including the Sustainable Development Goals)

Cambridge Zero (a new policy unit within the University of Cambridge)

Nischala: Thanks for sharing your views and knowledge on this critical topic, Josh! We’re all eager to see our industry taking more action to drive sustainable actions.

Enterprise data businesses Syniti and Data Migration Resources have joined forces in a move they believe makes them the biggest data software platform and services pureplay in this, or any other, town. And we see no reason to doubt their claim. With the thirst for quality data at a pandemic-driven all-time-high to base critical enterprise decisions, this merger is perfectly timed.

Under the Syniti banner – and with Syniti CEO Kevin Campbell remaining at the helm – the new company has the resources and global footprint to answer the ‘Are these guys big enough?’ question when it comes to tackling the most complex data requirements of the top echelons of the global 2000. The Newco claims it offers the largest collection of data specialists and an AI-driven platform converging capabilities across data management, analytics, and governance. With Campbell energized and back in his element, who drove one of the first BPO pureplays Exult, before he inspired the multi-billion dollar BPO and technology growth trajectories in Accenture (see blog), you have to believe the newly re-invented king of data services is taking his new company somewhere very interesting…

Tie up comes after record growth for SAP-certified Syniti

Both parties share a common focus on people and intend that the new scale of the organization will give their prized data specialists the opportunity and desire to stick around to build long careers and the culture to attract more.

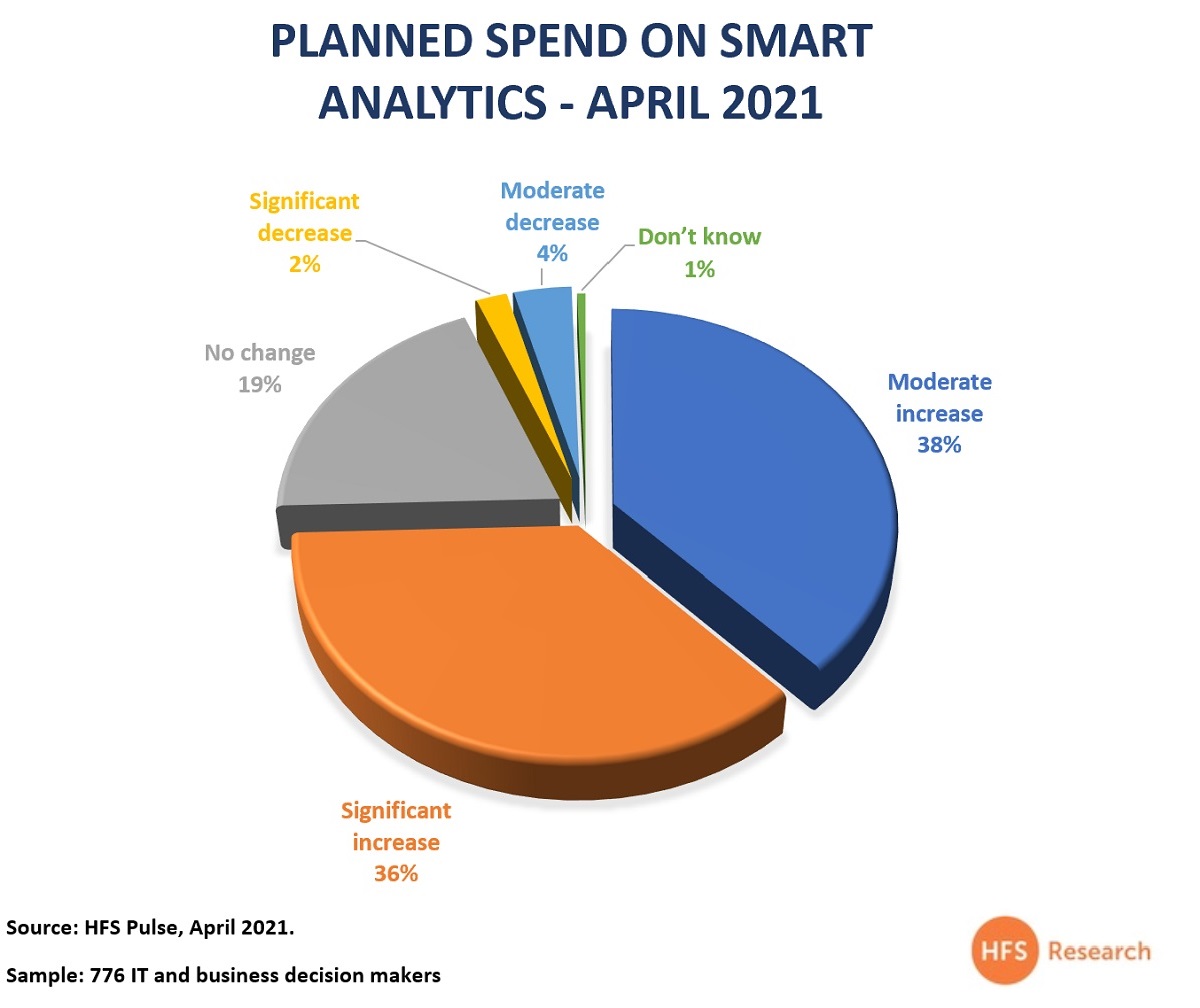

Syniti enjoyed record growth in 2020 (with some regions reporting more than 275% growth YoY). It reported the best Q1 results in its 23-year history at the end of April 2021. It’s riding a wave of rapidly increasing investment in smart analytics (Exhibit 1). Almost three-quarters see investments rising either significantly, or moderately.

Exhibit 1:Do you see investments increasing, decreasing, or staying the same for smart analytics in the next 12 to 18 months?

Syniti has been expanding from its SAP heartland (where it now holds SAP Certified Gold Enterprise Support Integration) to introduce real-time data replication with Amazon Web Services (AWS).

It is also an SAP platinum partner when it comes to helping businesses move to SAP S/4HANA, SAP SuccessFactors, and SAP Ariba. SAP resells data migration software from Syniti as SAP Advanced Data Migration by Syniti. Deloitte, IBM and DXC have been Syniti’s leading SI partners to date.

Joining together offers a global footprint and platform for acceleration

Syniti and DMR have been competitors in the North American market – each with facilities in India. Syniti has expanded to Europe and Asia-Pacific and DMR has gone into Latin America. The plan is to scale up globally, making use of the combined power of their India operations and sharing sales teams and the best of the products, tools, ideas, methods and techniques applied by each business. The aim is to accelerate their individual growth through combination – staking a bigger claim to the rapidly expanding demand for enterprise data management than either could alone.

The combined solution portfolio – comprised of the Syniti Knowledge Platform, DMR CONCENTO, Rapid Data Governance (RDG), and other software solutions, offers customers and partners aggregated, integrated capabilities to address a wide range of data-led business and IT requirements.

DMR products will remain supported into the foreseeable future and the combined might of the organizations will be applied to accelerate the ongoing development of DMR’s CONCENTO RDG – a potentially powerful differentiator if it delivers on its promise of cutting implementation costs by up to 50%.

Bridge Growth Partners are the majority owner of the new enterprise with DMR CEO Ryan Rodenburg joining the executive board with a ‘CEO of the Americas’ remit.

Bottom Line: Effective combination of assets holds the key to long term success

Thousands of hours of teaming ahead of the official merger proved the two parties can work together well. But the long-term success of the deal is likely to reside in how effective the new organization can be in making 1 + 1 = 3 when linking up its assets in a range of client-value-creating combinations. The new organization makes for a more balanced products/services company going forward, something the market is starting to reward. What is critical now is to encourage Syniti’s energized service provider partners, especially Deloitte, IBM, Accenture and DXC to increase their focus and staff training on the bigger, badder Syniti.

In short, we need to understand that data is the strategy to get us ahead of our markets. Here are five steps we must take:

Get The Data to Win In your Market. This is where you must align your data needs to deliver on business strategy. This is where you clarify your vision and purpose.

Re-think processes to get the data, Then you must re-think what should be added, eliminated, simplified across your workflows to source this critical data.

Design your new operational workflows in the cloud. There is simply no option but to have a plan to design processes in the cloud over three-tier web-architected applications. In the Work-from-Anywhere Economy, our global talent has to come together to create our borderless, completely digital business. This is the true environment for real digital transformation in action.

Automate processes and data. Automation is not your strategy. It is the necessary discipline to ensure your processes provide the data – at speed – to achieve your business outcomes. Hence you have to approach all future automation in the cloud if you want your processes to run effectively end-to-end.

Apply AI to data flows to anticipate at speed. Once you have successfully automated processes in the cloud, it is easy to administer AI solutions to deliver at speed in self-improving feedback loops. This is where you apply digital assistants, computer vision, machine learning, and other techniques to refine the efficacy of your data. AI is how we engage with our data to refine ourselves as digital organizations where we only want a single office to operate with agility to do things faster, cheaper, and more streamlined than we ever thought possible. AI helps us predict and anticipate how to beat our competitors and delight our customers, reaching both outside and inside of our organizations to pull the data we need to make critical decisions at speed.

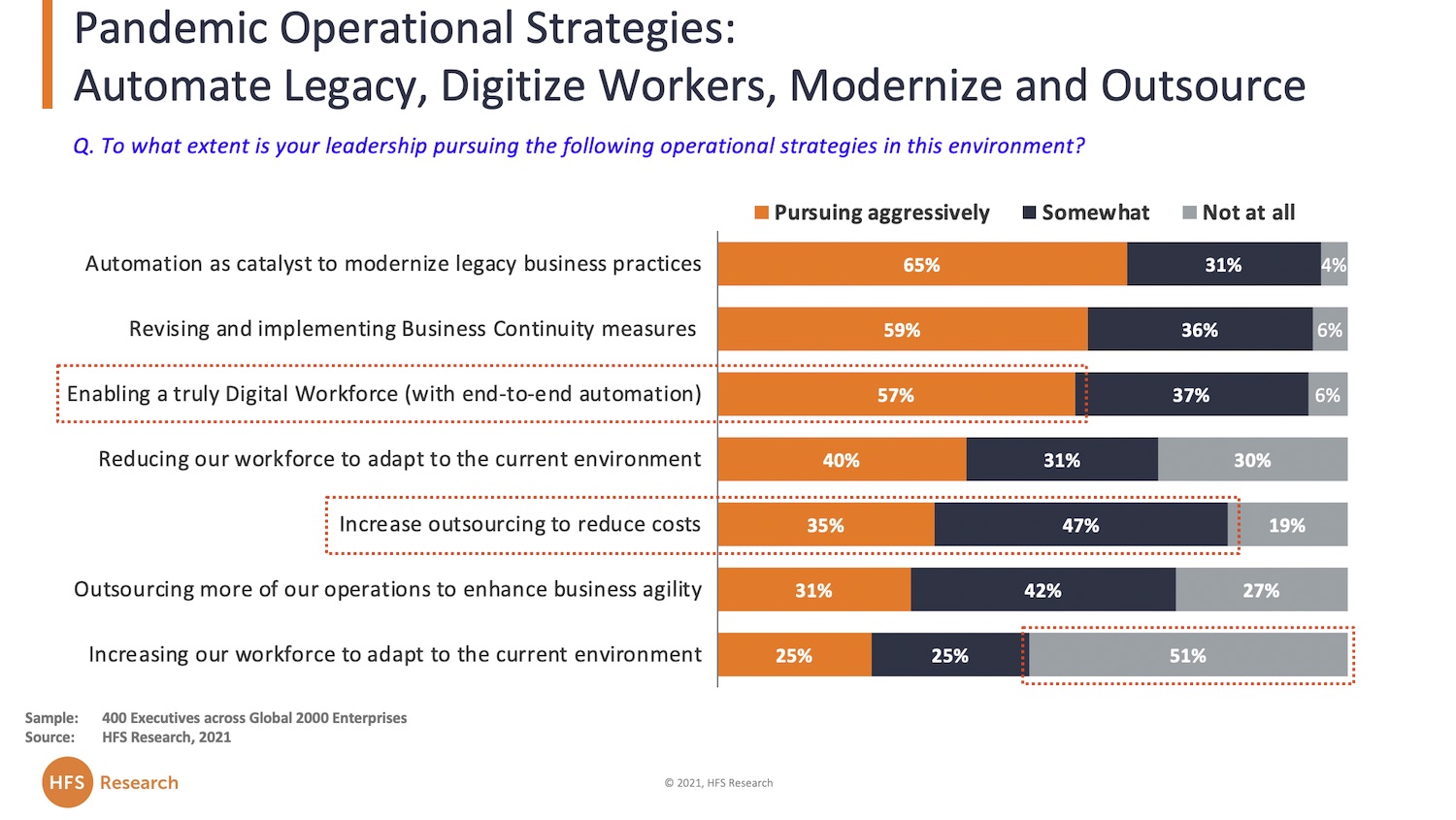

The impact of the pandemic has completely changed the mindset and change imperative of the majority of organizations. Our recent study of 400 operations and IT leaders across the Global 2000 shows how crucial automation has become as the catalyst to modernize business operations. And this means the old-thinking around RPA is rapidly leaving the building, as enterprises are faced with a dual challenge: ring-fencing legacy data centers and processes, while making fresh investments to re-jig critical processes to function effectively in the cloud:

Simply put, if you try to take your existing messy processes and simply move them “as-is” into a cloud environment, it’s going to be one very costly exercise that could be so cumbersome, you may go out of business before you even get them there. We used to talk a lot, in pre-Covid days, about moving your “mess for less” offshore, and even if you did very limited transformation, you would reduce costs simply because you were tasking lower-cost people to run them for you. Essentially, anything you couldn’t shoe-horn into your standard ERP model would be a prime candidate to outsource as it was not likely to be core business activity, but you still needed them processed, and you might as well run your mess for cheaper via a service partner, than do it yourself.

Two thirds of major enterprises have no choice but to head for the Cloud in the new economy

Fast-forward to 2021, and most large enterprises have managed to move their messy stuff to an outsourcer or their offshore captive. That was what legacy outsourcing was all about and over 90% of the Global 2000 did it. Now they are faced with a whole set of nagging new challenges, as they simply have to function in the cloud, if they want to be effective in this work-from-anywhere environment, which we know is going to be the norm for at least two-thirds of enterprises, even after we finally get Covid under control:

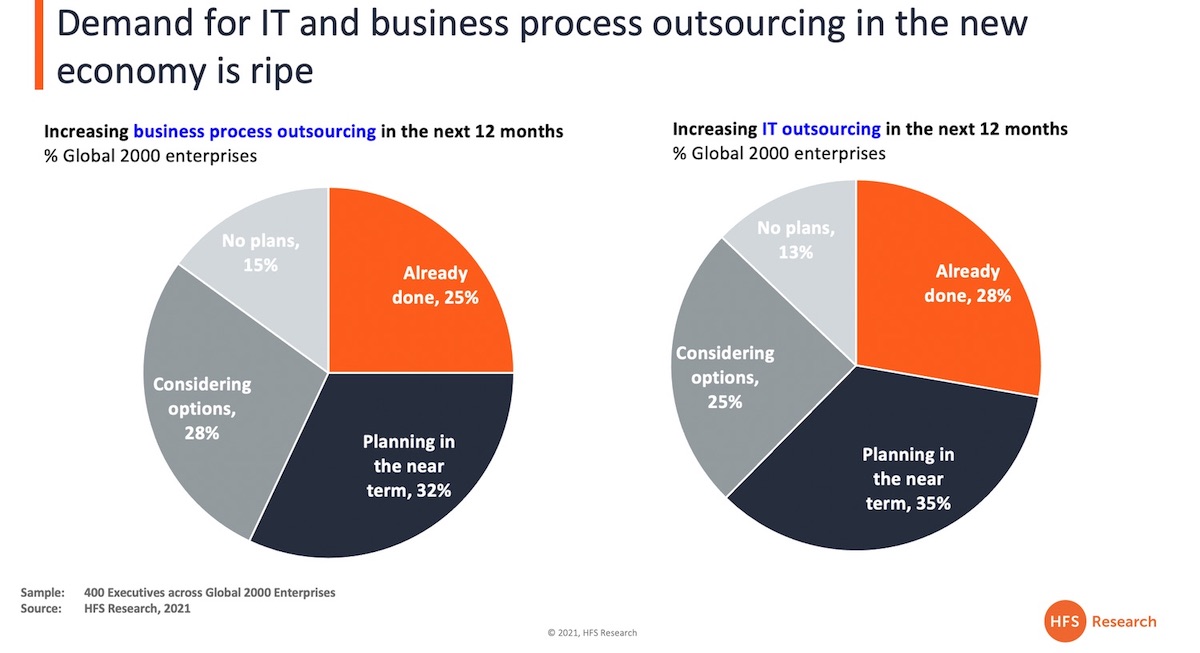

So what does this new wave of outsourcing look like, and why is it poised to increase at close to 10% this year – and likely even more next year?

The desire to centralize large clusters of people is dissipating with enterprise leaders focused on outcomes. After 14 months of operating with armies of shared service staff operating remotely, most have learned how to manage by focusing on the outcomes of getting processes delivered, as opposed to obsessing with governance structures based on effort and control. Many enterprise leaders have told us how they are focused on driving greater internal coordination with increased daily video meetings, where accountability and ownership are determinedly applied, and 51% (see above) do not see the need to add additional headcount to make this happen.

The need to scale-up and scale-down at speed has never been more pronounced. The number one watch-word today is about moving at speed. Enterprise leaders accepting the current status quo simply want to make fast decisions to make their operations and supply chains as nimble as possible. This means freeing themselves from multiple sign-off points to enact policies and strategies is becoming an imperative; lugging around bloated back office functions that strangle the ability to get things done is becoming a tainted memory. Having deeper partnerships with lesser numbers of partners not only cuts out operational costs, but also creates far more flexibility to operate at speed in unpredictable market conditions. This explains why a quarter of enterprises have already increased their outsourcing scope across business and IT processes in this environment, and a further third are planning to accelerate in the near term. Pipelines for new deals are strong – especially in Europe, and early indications from our soon-to-be-finalized Pulse study for H1 2021 indicate expenditure increase in the high single-digits:

The need to add “digitally-fluent capability” is forcing the issue on the interplay between business context and technology capability. With all today’s technology solutions CIOs are evaluating being cloud-based, their roles are shifting away from the provision of custom-app development, support and maintenance etc., and towards understanding the business context of their non-IT executive counterparts. This is more about housing data, ensuring security, scalability, speed and business continuity. They need to make their departmental leaders’ data ubiquitously available, accessible, and mineable – working with them to embed a mindset that inspires business and IT staff to work together to create an organization that can flip its business model to exploit these seismic market changes.

There is a lot more trust to work with partners. The rapid uptick in deeper, broader outsourcing relationships is being driven by enterprise buyers becoming more decisive and experienced, and their service partners becoming much more adept and confidant to strike rapid, cost-friendly deals, knowing they have the expertise and resources to make these deals profitable in the short term and (potentially) lucrative in the medium-longer term, as they get closer to their customers’ customers.

It’s much easier to have a third-party drive automation than forcing it on resistant/inexperienced staff. Today’s service providers are becoming highly adept at automating transactional work – simply because they have had no choice but to get proficient at it if they are to deliver value for their clients profitably. On the flip-side, enterprises have proven particularly useless at scaling automation projects and doing anything more than piecemeal projects within silos. We can delve into all the reasons why this has been a failure for over 80% of them, such as politics, employee resistance and inability to redesign processes (and let’s not forget a year-plus of pandemic), but the benefits of having an external party tasked with driving your automation efficiencies are now crystal clear.

Bottom-line: With the cyclical nature of global recessions, the historical reaction is to outsource without much transformation. However, the response this time is different…

Today’s service providers are much more confidant at delivering the outcomes because they know how to infuse technology to support these new commercial models. Moreover, you can’t get the data you need if your critical data is not in the cloud and you don’t have the people, partners, processes, technology – and desire to change – to make this possible. Service providers now have the experience, desire and risk-appetite to roll their sleeves up and help many enterprises make it through the most unpredictable economic era we have ever lived through.

Let’s cut to the chase folks… chatbots have struggled to gain much of a foothold in the corporate tech innovation stack. However, our analyst Melissa O’Brien has spent the last few years studying how these engagement technologies are evolving deeper into the enterprise where they can truly augment staff and reduce a significant amount of their time, while driving a whole new digital way of engaging for both employees and customers… from the back office right through to the front. So let’s take a look at which services firms are getting good at creating these digital associate workers for enterprises…

Melissa, we’ve been observing the evolution of “conversation AI” for a good decade-plus now, so what’s new? has the pandemic driven more uptake?

The demand for conversational AI has exploded over the last year. The automation tools we call digital associates were one of the digital superheroes of the pandemic, as conversational tools picked up the slack in handling volumes of interactions when human associates were not available due to a lack of work-from-home preparedness. Reduction in staff coupled with spike in volumes of interactions in many industries such as ecommerce created a burning platform. For many companies, this rapid and massive disruption resulted in accelerating digital initiatives already in play and pushing many lingering POCs into production mode. Industries like travel and hospitality, which had a brief period of an incredible uptick in customer interaction volumes a year ago, have now developed conversational tools poised to address inevitable future surges driven by pent-up demand.

Now that acceptance and adoption has increased significantly, the imperative is to move beyond the low-hanging fruit, the really simple and repetitive stuff, to really see what these tools are capable of. The next evolution of DA’s is a lot more about using ML and AI for conversational complexity, having a good design that fits into an overall experience strategy, and integration with enterprise systems in order to deliver greater value. Many companies which hadn’t dipped a toe into this space pre-pandemic are struggling a bit with the learning curve now, where others that had a foundation built already are expanding their use cases. Enterprises are now really looking at digital associates from an employee and customer experience perspective rather than only call deflection, efficiencies, and cost savings. In many cases, we’ve seen them as effective tools for sales conversions and building brand loyalty. So there are a lot more potential outcomes that companies are now looking to conversational AI to help achieve.

Why do you think this space has struggled to attract the feverish hype of RPA and “dumb” back office automation? What needs to happen to get the digital associate value proposition weaved into the whole intelligent automation and AI narrative?

I think part of the trouble is this market landscape is vast, the tools poorly defined and buyers are confused. This is part of the reason we’ve taken to calling the tools “digital associates,” to convey that they are digital workers built to provide a tangible outcome. Digital associates are not distinct segments like AI, automation, and analytics – in fact, they are tools that if designed properly use elements of all three to maximize their power. The face of automation has been largely tied to RPA, a singular tool where a lot of the use cases are straightforward – the quick time to value in many of these tools makes it a fairly fast and easy win for certain processes. With conversational AI, there’s a lot more nuance to think through employee and customer journeys, the complexity that is human language and interaction, and the connections that need to be made in disparate back end systems for them to operate in a meaningful way at the engagement layer.

Digital associates run the gamut of maturity, but often get associated with their simplest cousin, the chatbot. Chatbot fatigue has been a real roadblock; 10+ years ago the fad was to slap an FAQ bot on every website, expecting it to deflect calls and create efficiencies. More often they provided little help outside of website navigation, and created customer frustration and degraded the experience in the process. So people who hearken back to those experiences will have an aversion to trying out conversational tools or be hesitant about their value. This is obviously changing now as the real digital associates are starting to prove their worth.

I think this is where the OneOffice helps people conceptualize the impact digital associates can have on an organization. Firstly, start with an EX or CX focused outcome objective and design the DA backwards from there. As you’ve said yourself Phil, digital associates are augmenters of the human experience. They start to add more value as they become more sophisticated and embedded in our processes. And thinking in terms of the Triple-A Trifecta, the digital associates’ AI-powered brain is complemented by automation arms and legs to retrieve, report, update and transact. Data is the fuel the associate ingests to produce insights (analytics) and achieve optimal performance, including the personalization users are expecting.

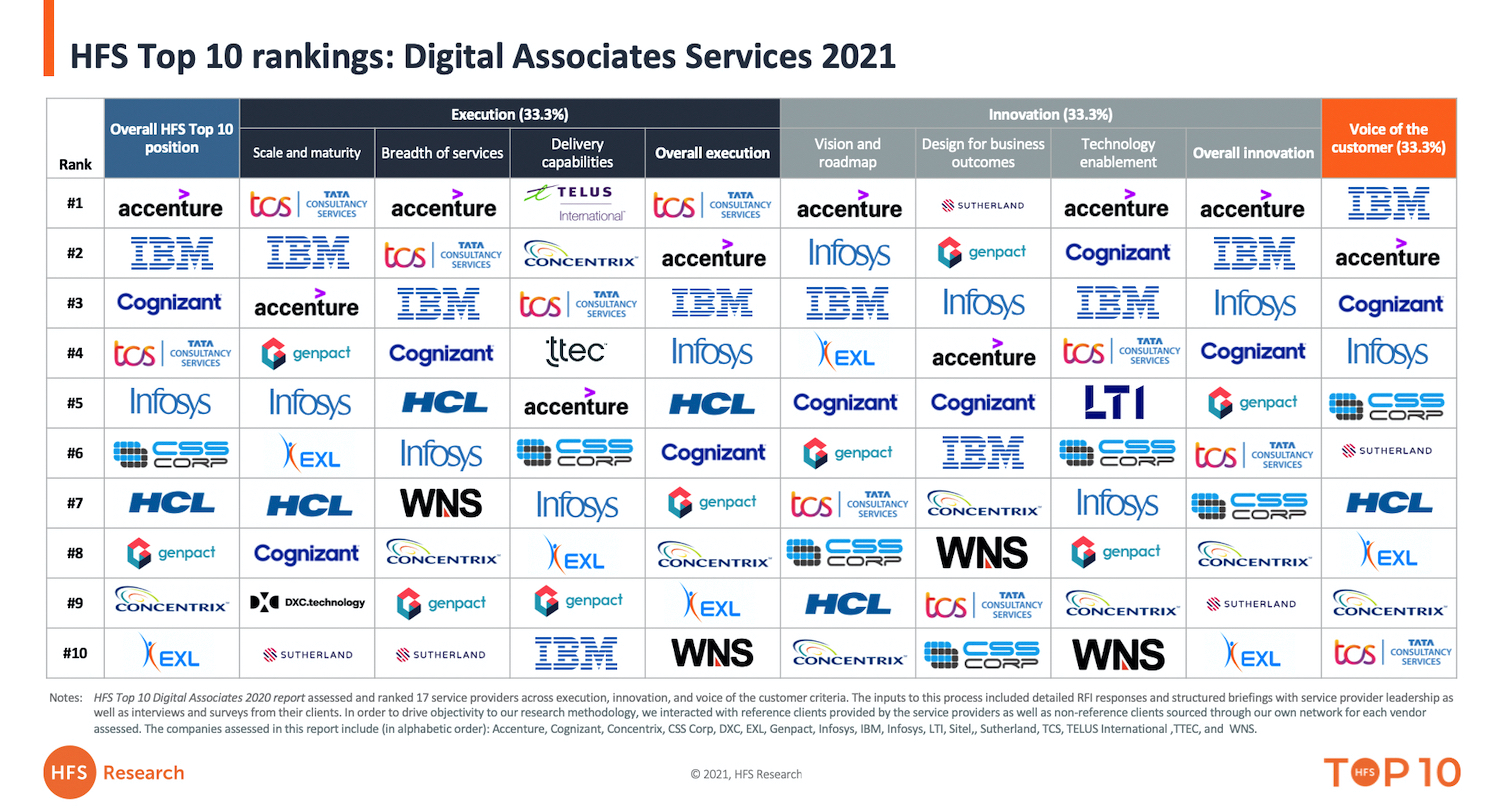

And which suppliers are currently winning in this market, Melissa? Both in terms of services and products?

Accenture, IBM and Cognizant took the top three spots respectively in our recent services Top Ten. These providers demonstrated an impressive breadth of capabilities across industries and enterprise functions, both IT and business, and a depth of design, process and technology prowess. While we didn’t include advisory firms in our assessment, focusing instead on BPO and IT services implementations, firms like KPMG and Deloitte have significant depth of expertise in developing solutions for clients in this area also.

On the products side, the number of vendors having some level of capability in this space is astounding. You’ve got the cloud providers which all have their platforms and developer suites, namely Google Dialog Flow & CCAI, AWS Lex & Connect , Microsoft Luis & Power VA. And then your established OOB software firms like IPsoft and Kore.AI, and including some of the RPA firms such as Pega and NICE dabble in various forms of digital associates. And we’ve been watching some interesting up and comers like last year’s “hottest hot vendor” Techforce.ai, and most recently we’ve been briefed on XpertRule’s Viabl.ai platform which comes in with an interesting value proposition focused on decisioning.

We’re really seeing this as an ecosystem play right now, as most of the successful implementations we’ve seen have required fairly complex customizations and integration from the service providers. While the products players tend to focus on selling licenses, the service providers provide with industry knowledge, deep understanding of clients’ processes and design expertise to help companies think through employee or customer touchpoints and really map out what they want to accomplish. And most of the service providers are completely technology agnostic, so they can come in and leverage an existing vendor relationship or preference or help evaluate vendors and select based on their requirements.

How are the call center firms approaching digital associates – are they reacting to customer demand, or still fighting to protect the legacy “butts-on-seats” model? Which ones are unafraid to disrupt the model and push conversation AI aggressively?

Many legacy contact centers still operate on FTE volumes and they’re safe for now because there’s still plenty of demand for labor-focused services (which is being driven quite a bit by growth in digital native companies whose rapid growth requires help to scale operations.) But most of the contact center leaders have a balanced approach which strategizes with clients on digital-first customer journeys which include a blend of automation and agent support. Concentrix is one of the most aggressive we’ve seen in this market, which landed at #9 in our recent report, the top ranking of any of the contact center pure plays. The challenge that the CX players continue to have is that of brand perception. They know that with the increase in self-service and automation that in many client engagements, if they don’t cannibalize their business another provider or vendor will. So they’ve built solid AI and automation capabilities for those clients with the appetite to work with them in that regard. The trouble is that some enterprise tech leaders won’t consider a contact center to work with on emerging tech, so in order for them to really gain traction in this space, there’s a mindshare gap to bridge, especially with IT decision-makers.

And finally, Melissa, how do you expect digital associates to evolve as we get used to new ways of working? are they going to branch way beyond customer-facing solutions?

Customer service examples are the most ubiquitous, but digital associates have already spread well beyond that realm. In the top ten, we saw a plethora of use cases in procurement, HR, IT helpdesk, finance, accounting, and much more. One of the interesting surprises we found was the prevalence of recruitment and HR bots. We’ve seen conversational AI tools which can help shepherd a candidate through the application and interview process, and also offer employee support once onboarded, helping staff access, understand, and process important information around benefits and compensation, performance, and time reporting. This is really a result of how accustomed we’ve become to automation in our consumer lives, that we expect to interact with digital ‘colleagues’ at work. And while chat solutions are still very commonplace, I do think the future of this market lies in voice. Not phone-based or intelligent IVR’s, but similar to virtual assistants like Alexa and Siri we’ve become so accustomed to in our consumer lives. Voice is opening so many doors right now to create new ways for people to engage either with our work as employees or with companies to buy services and products.