Digital is all about an organization’s ability to respond to the needs of their customers as those needs happen – or even be smart enough to anticipate those needs before they happen. This is all enabled by interactive technologies to create those touchless interfaces with the customers. Smart analytics and AI enable organizations to anticipate these needs based on the ability to recognize patterns and inferences over time, but nothing can really substitute for human intelligence to bring customers, suppliers and employees closer together, unimpeded by frustrating silos and legacy processes.

Remember, every broken process chain, or poorly converged dataset, slows down an organization’s ability to do business in real-time and stay ahead of its market. Traditional barriers between front, middle and back offices hinder the true ability of companies to operate in this real-time, responsive and anticipatory digital fashion, which is why we coined the term “OneOffice”, where the unification of digital business models, intelligent automation, analytics and creative talent is happening before our very eyes.

The HfS Digital OneOffice Framework (see below) describes how organizations must integrate their digital customer interfaces with their operations in order to fulfill and anticipate their customers’ needs. It is the organizational end-state to survive and succeed in a world where digitized processes dictate how responsive, agile, cost-effective, predictive and intelligent firms have to be to stay competitive.

To this end, we have delved deep into all the four dimensions of the Digital OneOffice, and conducted deep analyst discussion to aggregate service provider performance at delivering the sum of the Digital OneOffice parts:

- Digitally driven front office

- Digital underbelly

- Intelligent digital support functions

- Predictive digital insights

So how did the Winner’s Circle service providers fair?

Accenture

Strengths

- Well-rounded portfolio across OneOffice: Accenture has the best performance overall across the OneOffice portfolio, and a breadth of industry expertise to complement it. Accenture placed in the Winners’ Circle for each of the Blueprint studies used to compile this OneOffice assessment.

- Strong marketing operations capabilities to support integrated digital OneOffice offerings. Accenture has 16,000 business-focused staff dedicated to delivering digital marketing assignments – a considerable asset that goes well beyond the firm’s IT delivery.

- Strong intelligent automation capabilities. Acquisition of GenFour and exciting partnerships, with significant investments, with the likes of Automation Anywhere, Blue Prism and IPSoft.

- Winning with thought leadership: Accenture is well-known as a thought leader across many of the change agents as well as within individual industries.

- C-Suite relationships beyond IT. Digital business and intelligent automation decisions are largely being driven by both IT and business C-Suite executives in the Global 2000. Accenture has the combination of strategic relationships outside of IT, in addition to the managed services execution.

- Leveraging creative assets for CX and UX design: Accenture has developed an industry-leading focus on becoming a customer experience expert, as evidenced by its 30+ design agency assets, by the broadest portfolio of digital design assets in the services industry (click here for a full list of digital M&A in services.)

Challenges

- Size can work in its disfavor: Its size and success have given Accenture a reputation as a premium, high cost, and less responsive organization. In particular, for smaller companies, just this perception in the market can steer buyers instead toward more niche specialized agencies and the attention, flexibility, and experience they receive from a smaller provider.

- Finding the right culture balance: Accenture is well known for its results-driven, traditional consultancy culture, which will need to be balanced out or effectively blended with the more left-brain focused acquisitions in order to retain creative talent and remain generally effective.

- Proving to the industry it can deliver the end-to-end Digital OneOffice portfolio: There is no doubt that Accenture can pick up strategic work and execute for clients, but being able to demonstrate to the industry it can deliver both the strategic design integrated with complex operational delivery – at scale – is still in its infancy. Many of its competitors will fight hard for execution work where Accenture is delivering the high-end design and consulting. It needs to demonstrate the “one-stop OneOffice shop” is where it wins.

IBM

Strengths

- Strong intelligent OneOffice offering: Market leading capabilities to drive the OneOffice underbelly (automation, security, cloudification) and neural networks (AI, smart analytics, blockchain, and IoT). Impressive development of credible global automation capability and several notable early wins.

- Portfolio breadth: End-to-end and scaled IT and business process services across front, middle, and back-office.

- Horizon 4 investments: Very strong investments and IP in horizon 4 (and beyond) technologies that will shape the future (e.g., Quantum Computing).

- Design Thinking: Has made some considerable investments in recent years, but needs to align more aggressively with OneOffice approach

- Watson: The analytics/cognitive powerhouse has a significant role to play as a cognitive virtual agent, an analytics resource that has huge scalabiity and a long-term investment area for firms with deep interests in their cognitive capabilities.

Challenges

- Size can be a disadvantage: IBM is a large and complex organization, which makes it hard to seamlessly deliver all that it has to offer.

- Translating tech to business outcomes: IBM is often perceived as a technology powerhouse, but one lacking the business translation and context to successfully apply emerging technologies.

- Agility: Lacks the nimbleness and flexibility of smaller players.

- Focus on cognitive may impede its ability to compete for design-focused end-to-end deals: IBM has substantial credibility to drive analytics-driven, cognitive/automation projects, but its lesser focus (over the last couple of years) on true digital design may see it lose out to firms such as Accenture and Cognizant, where digital is firmly established at their core.

Cognizant

Strengths

- Digital marketing is leading front office services: Cognizant performed well in our digital marketing services Blueprint, primarily based on its targeted acquisitions and proprietary IP and frameworks.

- Solid portfolio for the digital underbelly: Cognizant landed in the Winners’ Circle for each digital underbelly-focused Blueprint.

- Strong thought leadership: Cognizant has a very compelling and polished messaging around customer experience focus and automation with forward-thinking leadership, bolstered by design-oriented acquisitions.

- Simple, focused strategy: Unlike several of its Indian-heritage counterparts, Cognizant has always kept its focus simple and business focused. It’s “SMAC stack” approach was the perfect prerequisite to digital.

Challenges

- Integration of key acquisitions will be key to success: Cognizant has made targeted acquisitions such as Cadient, whose capabilities the service provider is still working to integrate in order to bring value to clients.

- Expansion of Design Thinking across services capabilities: Cognizant needs to develop its Design Thinking capabilities to other elements of services outside the front office in order to help its clients on the journey to realize the OneOffice endgame.

- Keeping the momentum going: Cognizant has grown faster than any of the major service providers over the last decade. Keeping its scale aligned with its growth is going to be a challenge to the firm, with greedy investors still expecting 10%+ annual growth in a slowing market.

Infosys

Strengths

- Portfolio across OneOffice capabilities: Strong capabilities across all dimensions of the Digital OneOffice—digitally enabled front office, digital underbelly, intelligent support functions and the nervous system. Recent re-focus on digital expansion is a plus.

- Focused go-to-market approach: Digital platforms, automation, and AI have emerged as key pillars of the go-to-market strategy.

- Digital OneOffice transformation services: All-rounded and scaled IT-BPM capabilities required for Digital OneOffice transformation.

- Data DNA: Infosys has already been very strong with its data capabilities and provided it stays focused on this new course (see the recent interview with its new CEO), the future should be bright as a OneOffice heavyweight.

- Strengthening BPM capabilities: InfosysBPM has demonstrated some of the strongest growth in the industry with some impressive BPM wins over the last 18 months. With deep competencies in middle/back office, in addition to marketing and analytics, the firm can make a strong run at the likes of Accenture, IBM and Cognizant, provided it keeps investing in its digital capabilities.

- US onshore investments: Infosys has targeted 10,000 new staff to locations such as Indianapolis and Dallas. This is being well received by politicians and clients alike and helping align the firm with clients needing more onsite/onshore support.

Challenges

- Relatively conservative M&A outlook: Despite recent acquisitions, overall outlook to M&A continues to be conservative.

- Leadership turnover: Frequent changes to top leadership impact market positioning and consistent messaging. The new regime has to keep this ship firmly focused.

- Market perception as a tech player: Infosys continues to be perceived as a technology player and needs to double down on driving business context in its solutions.

- Needs to spend some of its war-chest: Infosys needs more depth in front-end digital delivery than Brilliant Basics and WONGDOODY. Salil needs to go shopping and spend some of his massive war-chest.

Wipro

Strengths

- Key acquisitions bolster digital transformation capabilities: Wipro’s acquisitions of Designit and Topcoder (Appirio) give Wipro some significant assets for strategic design and UX, and also strong talent in the realm of data science, design, and development.

- Services delivery excellence: Wipro has a strong execution approach to BPO and RPA with its Enterprise Operations Framework and is known as a solid delivery partner across a broad portfolio of services. Strong global presence and competitive aggression to win strategic deals.

- Partner ecosystem: Wipro Ventures’ investment highlights its partner-focused approach. it’s reputation for being easy to work with has helped the firm develop exciting alliances with emerging firms in the fintech, startup space.

- Much improved thought leadership: In previous years this was a major weakness for the firm, but a successful rebrand and a consistent delivery of market positioning and client experiences has change the percpetion of Wipro significantly with clients and market influencers alike.

- Reputation for execution: Wipro has done a lot to up its game in recent years to deliver a multitude of touch, complex global deals. Many of its clients have a strong level of trust in the firm to move further up the value chain.

Challenges

- Integrating acquisitions for a more consultative capability: Clients are looking for stronger thought leadership from Wipro and could use a stronger business- outcomes approach to its messaging. Further integration of acquisitions like Designit can help Wipro be a better innovative thought leader for clients on the journey to OneOffice.

- Development of marketing of HOLMES platform: Wipro should invest in messaging for its HOLMES platform, one of the first broad automation frameworks on the market, to highlight its deep capability and assets in the bot library.

- Needs more front-end digital acquisitions: Not dissimilar to Infosys and TCS, Wipro needs to keep focused on further front-end acquisitions to boost its digital presence with the design areas of the market.

TCS

Strengths

- Client relationships: Appreciated for its engagement with clients, proactive focus on process improvements, and flexibility. Good account management skills. Clients mention factors such as understanding their business and unique operating models and being flexible to work with.

- Embedded analytics: TCS is one of the top service providers with analytics reported as embedded in contracts. Has positioned much of its talent in its data analytics areas as a front-end strategy.

- Intelligent Automation: Major focus on internal capabilities, including ignio platform. Impressive record with clients and a willingness to cannibalize revenues to grow emerging areas.

- Partner ecosystem: TCS has a strong partnership ecosystem for emerging technologies. Its work with academia and startups has been most impressive, with significant funds being invested to create strong talent programs and joint business ventures with innovators.

Challenges

- Thought leadership needs a lot more focus: TCS needs to be more proactive and vocal about ideas around innovation and best practices. It is often challenging to pinpoint the core focus of the firm beyond being a competent technology firm.

- Behind on M&A: While most of the big service providers are scaling up their portfolio through acquisitions, TCS has made a few acquisitions, but is relying primarily on organic growth. While this is clearly a desire from leadership to grow organically, it could significantly stunt TCS’s ability to evolve into more creative design areas where the firm is currently lagging. A reversal of strategy is probably likely in the future as the market shakes out.

- IT services and middle office focused: Aside from a strong digital marketing offering, TCS is more back and middle office, with more of an IT services presence in the middle office. BPM was a core focus, but seems to have faded somewhat in the last couple of years.

- Heavy India delivery: TCS could increase recruitment in specific geographies for more diversification.

Other notable service providers

Outside of the winner’s circle, Capgemini was one of the most notable exclusion, despite a well-rounded OneOffice portfolio across front and back office. The firm still struggles with its North American portfolio, despite its IGATE acquisition and its co-CEO structure and lack of thought leadership has held back progress. Genpact has impressed clients with its LEAN Digital approach, its depth in processes and recent acquisitions in AI, but its lack of scale in IT has kept the firm of the Winner’s Circle. HCL has performed well its strong breadth of services, strength in automation and notable flexibility with clients, but lags the leaders in terms of digital design, change management analytics and innovative messaging. DXC is still trying to find its feet since the HP/CSC merger but has very strong IT delivery capability. The firms does need a strong injection of market positioning and expansion beyond its infrastructure capabilities. Tech Mahindra has quietly emerged as a high performer, boasting a series of impressive digital front-end platforms, a real appetite for innovation and strong client partnerships. We expect the firm to keep improving its market position, providing it can diversity effectively beyond telco, make some astute analytics investments and leverage its M&A for effectively (its Pininfarina acquisition has largely been considered to be misaligned).

Bottom-line: Winning at OneOffice services is about delivering the four dimensions as a true client partner with co-defined outcomes and investments on both sides

The traditional services model was all about delivering incremental productivity and efficiency for clients. There was rarely much purpose behind the client/service provider relationship beyond attaining a series of predefined cost/delivery metrics and KPIs. And once the first set of metrics were met, the next set was normally more of the same, but with added pressure on margins, which ultimately led to a degrading of quality and talent. “They sold us the A team and we ended up with the B and C team” is probably the most worn services catchphrase of the last two decades in the services industry. However, if clients wanted the cheap and cheerful model, that’s ultimately what they ended up with: getting exactly what they were paying for. All you have to do is look at the depressing number of legacy services relationships littering the Global 2000, where most the value has been squeezed out, and both client and service provider are stuck on a depressing treadmill where both often want out, as they just don’t get much business value from the relationship.

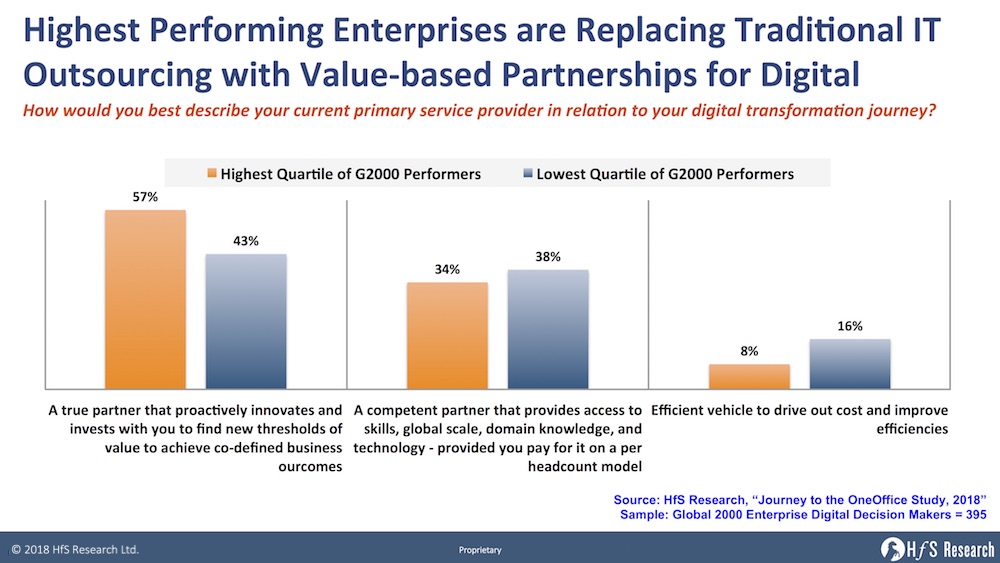

Fortunately, the business imperatives have been changed forever with the evolution of digital business models, which is having the impact of driving much smarter, value-driven partnerships for ambitious clients and service providers. Sure, there will always be the laggards who will persist on cranking out the same old business models until they fade into insignificance, but 57% of digital decision markets among the highest performers (based on revenue and profitability) in the Global 2000 now view their primary service partner as a co-creator of innovation and value, as opposed to a provider of prepaid services that merely provides efficient services as our recent study looking at digital transformation to the OneOffice reveals.

This data speaks volumes – enterprises digital leaders need providers which can work with them to achieve outcomes that are increasingly challenging, with only a third viewing their service providers solely as a resource to provision skills and scale via a headcount model.

A true digital business cannot succeed without unifying front, middle, and back offices – it’s no longer about being great at one component, it’s about weaving together the disparate parts to bring customers and employees as closely together as possible to create the best possible customer experience that wins out in cut-throat markets. Sure, there will always be niche opportunities to support certain needs for enterprises, but the ultimate winners will be those which can partner with their clients to help define and deliver their business outcomes over the long-term. This means providing the business intelligence, market understanding, and technical abilities to help their clients be as competitive as possible. The stakes are higher than ever, and the smart providers are those placing their investments in clients with whom they can thrive over the long-haul.

Posted in : Digital Transformation, OneOffice

Excellent analysis. Very compeling methodology and lays out the future of services in a clear, value-driven way,

James

Very strong analysis, Phil. Good to see the Indian majors pushing up the digital value chain.